Answered step by step

Verified Expert Solution

Question

1 Approved Answer

especially c)!!! 2. Suppose you run a convertibles arbitrage hedge fund. You've noticed a po- tential trading opportunity related to the different securities issued by

especially c)!!!

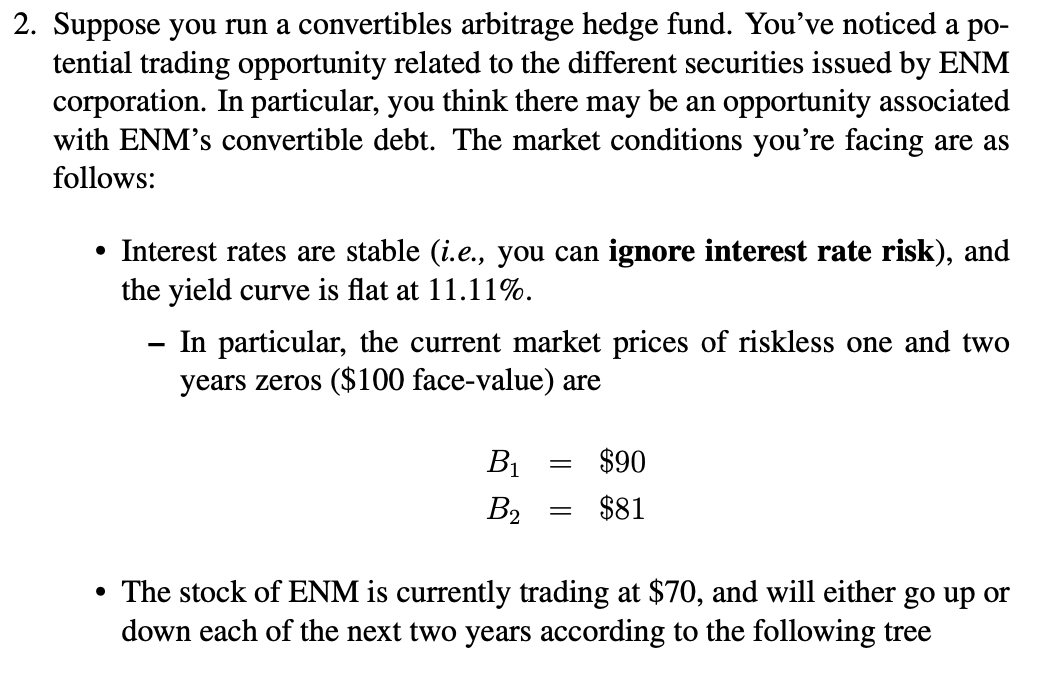

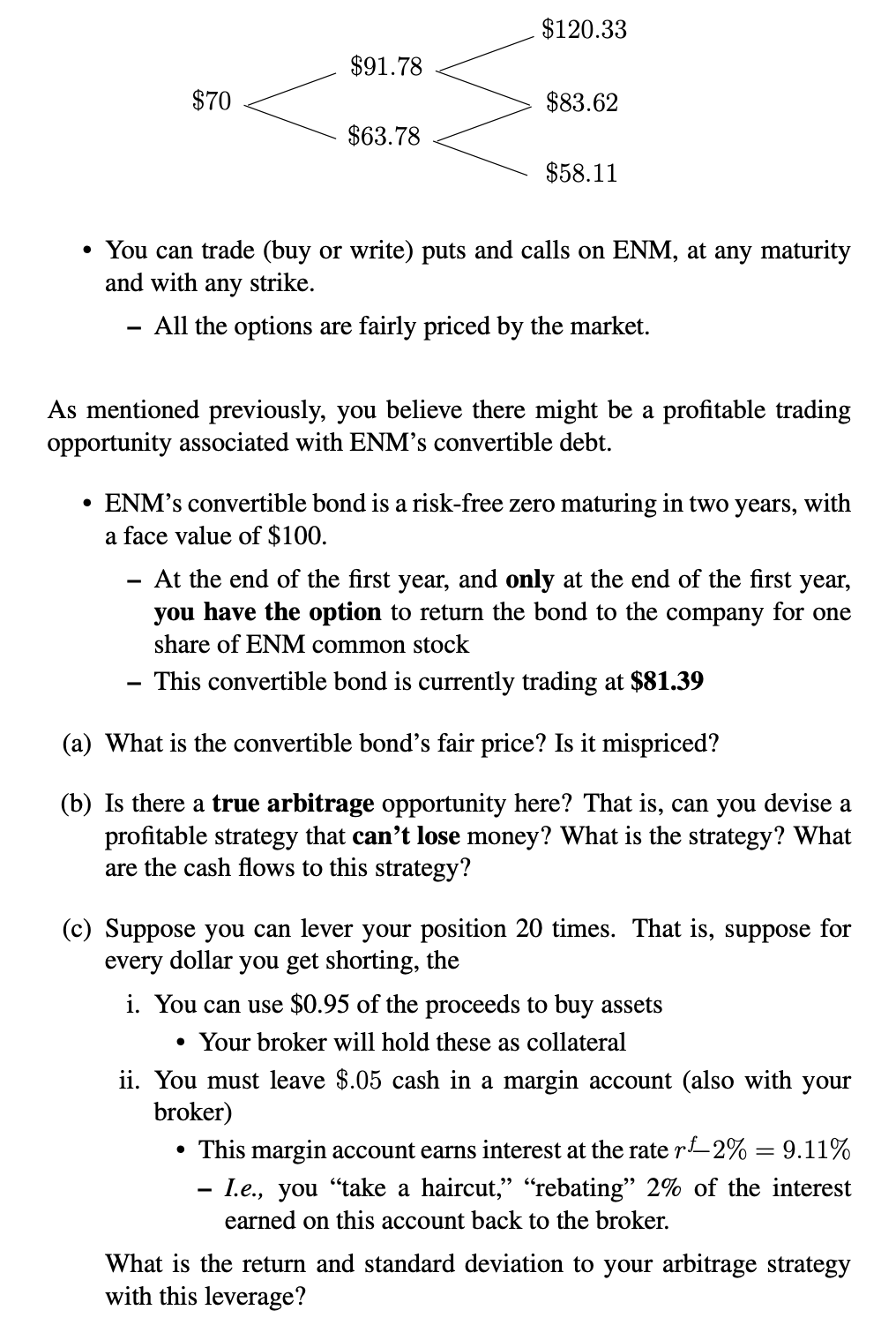

2. Suppose you run a convertibles arbitrage hedge fund. You've noticed a po- tential trading opportunity related to the different securities issued by ENM corporation. In particular, you think there may be an opportunity associated with ENM's convertible debt. The market conditions you're facing are as follows: Interest rates are stable (i.e., you can ignore interest rate risk), and the yield curve is flat at 11.11%. In particular, the current market prices of riskless one and two years zeros ($100 face-value) are Bi $90 $81 B2 = The stock of ENM is currently trading at $70, and will either go up or down each of the next two years according to the following tree $120.33 $91.78 $70 $83.62 $63.78 $58.11 You can trade (buy or write) puts and calls on ENM, at any maturity and with any strike. All the options are fairly priced by the market. As mentioned previously, you believe there might be a profitable trading opportunity associated with ENM's convertible debt. ENM's convertible bond is a risk-free zero maturing in two years, with a face value of $100. At the end of the first year, and only at the end of the first year, you have the option to return the bond to the company for one share of ENM common stock This convertible bond is currently trading at $81.39 (a) What is the convertible bond's fair price? Is it mispriced? (b) Is there a true arbitrage opportunity here? That is, can you devise a profitable strategy that can't lose money? What is the strategy? What are the cash flows to this strategy? (c) Suppose you can lever your position 20 times. That is, suppose for every dollar you get shorting, the i. You can use $0.95 of the proceeds to buy assets Your broker will hold these as collateral ii. You must leave $.05 cash in a margin account (also with your broker) This margin account earns interest at the rate rf_2% = 9.11% I.e., you take a haircut, rebating 2% of the interest earned on this account back to the broker. What is the return and standard deviation to your arbitrage strategy with this leverage? 2. Suppose you run a convertibles arbitrage hedge fund. You've noticed a po- tential trading opportunity related to the different securities issued by ENM corporation. In particular, you think there may be an opportunity associated with ENM's convertible debt. The market conditions you're facing are as follows: Interest rates are stable (i.e., you can ignore interest rate risk), and the yield curve is flat at 11.11%. In particular, the current market prices of riskless one and two years zeros ($100 face-value) are Bi $90 $81 B2 = The stock of ENM is currently trading at $70, and will either go up or down each of the next two years according to the following tree $120.33 $91.78 $70 $83.62 $63.78 $58.11 You can trade (buy or write) puts and calls on ENM, at any maturity and with any strike. All the options are fairly priced by the market. As mentioned previously, you believe there might be a profitable trading opportunity associated with ENM's convertible debt. ENM's convertible bond is a risk-free zero maturing in two years, with a face value of $100. At the end of the first year, and only at the end of the first year, you have the option to return the bond to the company for one share of ENM common stock This convertible bond is currently trading at $81.39 (a) What is the convertible bond's fair price? Is it mispriced? (b) Is there a true arbitrage opportunity here? That is, can you devise a profitable strategy that can't lose money? What is the strategy? What are the cash flows to this strategy? (c) Suppose you can lever your position 20 times. That is, suppose for every dollar you get shorting, the i. You can use $0.95 of the proceeds to buy assets Your broker will hold these as collateral ii. You must leave $.05 cash in a margin account (also with your broker) This margin account earns interest at the rate rf_2% = 9.11% I.e., you take a haircut, rebating 2% of the interest earned on this account back to the broker. What is the return and standard deviation to your arbitrage strategy with this leverageStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Secured Finance Transactions

Authors: Dominic RM Griffiths

2nd Edition

1787425142, 978-1787425149