Answered step by step

Verified Expert Solution

Question

1 Approved Answer

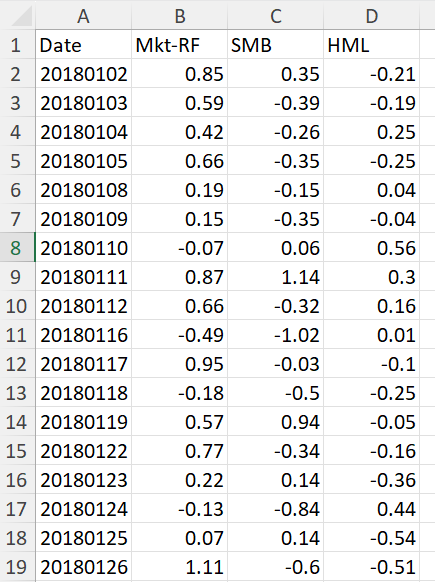

estimate VaR for an equity portfolio using the Model - Building approach using excel functions, show all clear steps with guide. Suppose you have invested

estimate VaR for an equity portfolio using the ModelBuilding

approach using excel functions, show all clear steps with guide. Suppose you have invested in two of the FamaFrench factors, namely MktRF and

HML Assume conditionally the returns of MktRF and HML follow a bivariate normal

distribution. Assume the portfolio return is the sum of the factor returns. Estimate the daily volatilities and the correlation using the EWMA model with lambda

using excel functions, show all clear steps with guide Plot the daily volatilities for MktRF and HML on the same graph. Plot the daily

correlations on a separate graph using excel functions, show all clear steps with guide. Estimate the oneday VaR for the portfolio uing excel functions, show all clear steps with guide

Note: You are not required to use maximum likelihood to estimate lambda we simply

assume lambda You may assume the initial variance for the first rate of return is

equal to the sample variance, and the initial covariance is equal to the sample

covariance.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Process To Profits Strategic Planning For A Growing Business

Authors: William Lasher

1st Edition

0324223870, 9780324223873