Answered step by step

Verified Expert Solution

Question

1 Approved Answer

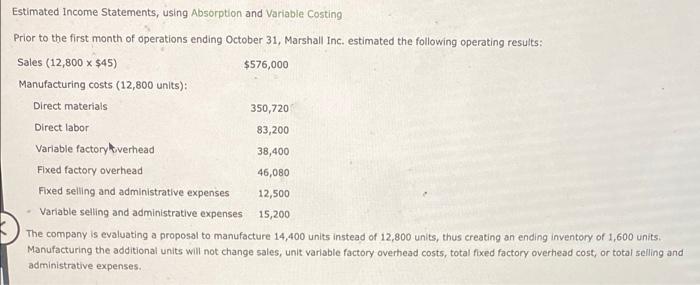

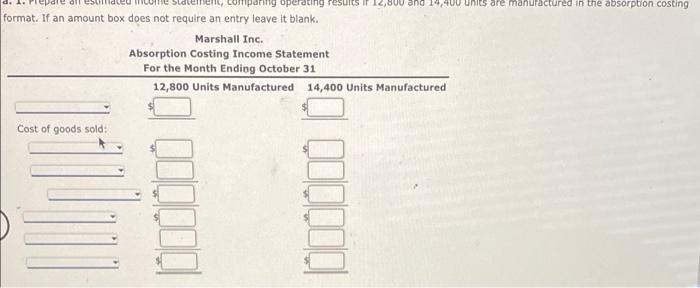

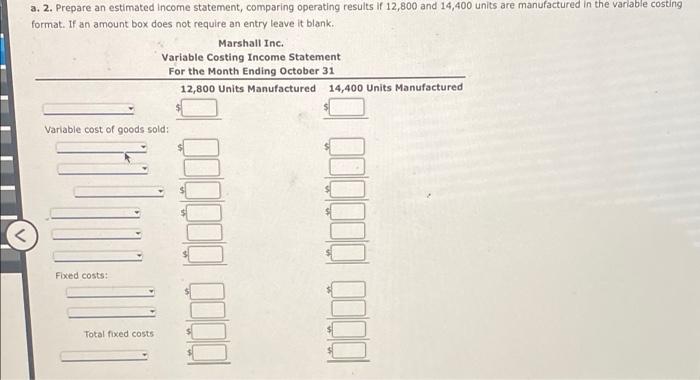

Estimated Income Statements, using Absorption and Variable Costing Prior to the first month of operations ending October 31, Marshall Inc. estimated the following operating results:

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Valuation For Accountants A Short Course Based On IFRS

Authors: Stephen Lynn

1st Edition

9811503567, 9789811503566