Answered step by step

Verified Expert Solution

Question

1 Approved Answer

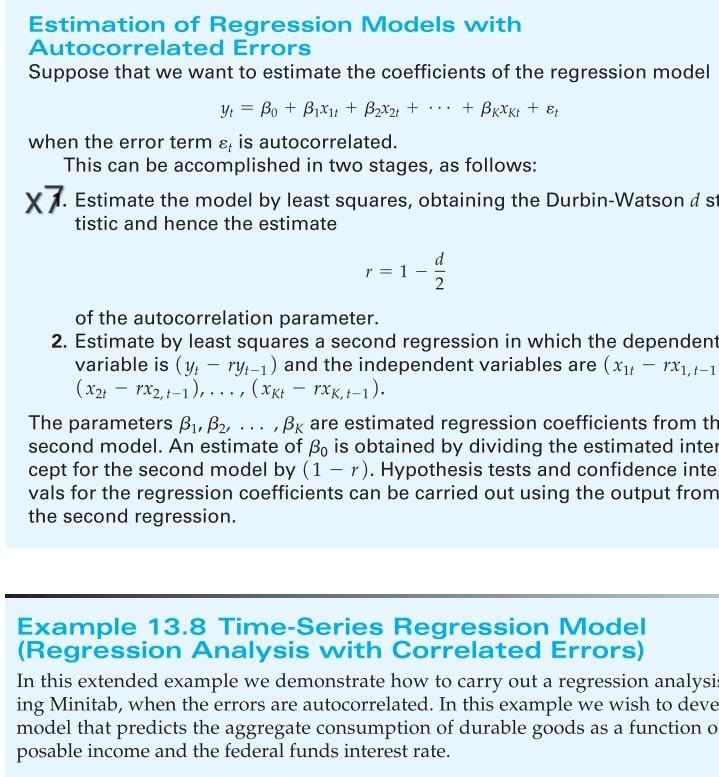

.. Estimation of Regression Models with Autocorrelated Errors Suppose that we want to estimate the coefficients of the regression model y: = Bo + B1X11

.. Estimation of Regression Models with Autocorrelated Errors Suppose that we want to estimate the coefficients of the regression model y: = Bo + B1X11 + B2X2 + + BKXK+ + 8 when the error term er is autocorrelated. This can be accomplished in two stages, as follows: x7. Estimate the model by least squares, obtaining the Durbin-Watson d st tistic and hence the estimate d r = 1 2 of the autocorrelation parameter. 2. Estimate by least squares a second regression in which the dependent variable is (y: - ryt-1) and the independent variables are (X11 1X1,4-1 (x2+ - rx2,-1),..., (XK+ rxk,t-1). The parameters B1, B2, ..., Bk are estimated regression coefficients from th second model. An estimate of Bo is obtained by dividing the estimated inter cept for the second model by (1 r). Hypothesis tests and confidence inte vals for the regression coefficients can be carried out using the output from the second regression. Example 13.8 Time-Series Regression Model (Regression Analysis with Correlated Errors) In this extended example we demonstrate how to carry out a regression analysi ing Minitab, when the errors are autocorrelated. In this example we wish to deve model that predicts the aggregate consumption of durable goods as a function o posable income and the federal funds interest rate

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Analysing The Value Proposition Of The Audit Process In Africa The Case Of Malawi

Authors: Daniel Dunga

1st Edition

3659166286, 978-3659166280