Question

Evaluate the following questions and answer. The remaining Application Exercises deal with purchasing a house. Assume that you are currently renting an apartment for $1,040

Evaluate the following questions and answer.

The remaining Application Exercises deal with purchasing a house. Assume that you are currently renting an apartment for $1,040 per month and you have been considering buying a house. You have saved $10,000 toward a down payment for the house.

A salesperson informs you that he has a new house for sale, where the house and land were independently appraised at $200, 000, but are being sold by the builder at a discount price of $185, 000. The builder wants to get rid of the property quickly because the house is the last one to be sold in the development and the builder is moving on to construction of a new development.

The salesperson connects you with his in-house lender, to whom you give details about your income and grant permission to review your credit and eligibility for a loan. You inform her that you are prepared to make a down payment of $10,000 toward the house if necessary. She gets back to you with good news that, if you put $8,100 toward the house, then they can give you a 30-year loan for the balance of $176,900 at 6.25% per annum (compounded monthly). Note that lenders require the house to appraise at or above the purchase price; otherwise, they may reject the loan or require more down payment. The lender computes the monthly mortgage payment at $1,089.20. She informs you that the remaining $1,900 of your $10,000 can be used toward costs associated with the final evaluation of the physical property and the closing of the purchase (property inspector fee, termite inspector fee, official survey, attorney fees, etc.). The builder agrees to pay for costs beyond your $1,900 and make necessary repairs you identify during the period you have to inspect the property (the due diligence period).

Hearing the news about your qualification for the loan, the salesperson asks you how much rent you are now paying. When you inform him that you pay $1,040 per month, he quickly points out that it would be a mere extra $50 per month for you to meet the mortgage payments. He emphasizes that it is better to own than to rent, especially if the mortgage is just a bit more than your current rent.

QUESTION 1. In addition to closing fees paid to settle the loan, there are expenses beyond the monthly mortgage payments. First, since your deposit was less than 20% of the purchase price, you are required to take out a private mortgage insurance (PMI) to protect the lender if you default on the loan. The PMI typically lasts until the unpaid principal balance of the mortgage is paid down to 80% of the original value of the house, where the house's original value is the lesser of the purchase price and the official appraised value of the house used in closing the sale. Note that the bank may also require your payment history to be in good standing (e.g., no late payments in the past year or two) before removing PMI. Of course, if the value of the house increases nontrivially, you may be able to remove the PMI earlier. Suppose that the PMI is $141.52 per month.

Second, along with PMI, you have to pay for hazard insurance to cover un- planned damages to the house due to fire, smoke, wind, etc. Assume that the hazard insurance is $36.50 per month.

Third, you have to pay property taxes to the tax district (e.g., county and city) where the house is located. The property (i.e., house and land) will be valued within your tax district, which is a valuation that is separate from the appraisal done when purchasing the house. The resulting tax district's valuation is the taxable value of the house and is the amount to which the property tax rate will be applied. Suppose that the annual property tax rate is 1.3% and the taxable value of the property is $189, 986. For this project, the taxable property value is less than the appraised value (i.e., $200, 000) used for the purchase. Sometimes, however, the taxable value can be higher which was not uncommon in the aftermath of the 2008 mortgage crisis.

The PMI, hazard insurance, and property tax payments are in addition to the monthly loan payment, and all together they form a single payment you make to the lender. The lender or a company hired by the lender manages these payments by taking out the portion for the loan payment (principal plus interest) and depositing the rest into an escrow account, which is used to pay the annual insurance premiums and property taxes on behalf of the borrower.

Finally, assume that the property is in a housing development that comes with a mandatory Homeowners Association (HOA) fee. The HOA fee is used to maintain the grounds, roads, etc. in the development. If you do not pay the fee, the HOA can foreclose on your property. Assume an HOA fee of $100 per month.

a) What is the estimated total monthly PITI, i.e., the minimum monthly payment covering the principal, interest, taxes, and (hazard) insurance?

b) Identify two other mandatory house expenses that are outside of the PITI payment and other basic house costs like utilities and repairs. Do exclude costs like groceries, tuition, medical expenses, etc., which are more associated with running a home. What is the minimum monthly cost of the house during the first year if you now include these two mandatory house expenses and PITI? Which of these housing costs will likely increase in the future?

c) What is your opinion about the salesperson's pitch about the cost of renting versus buying a house?

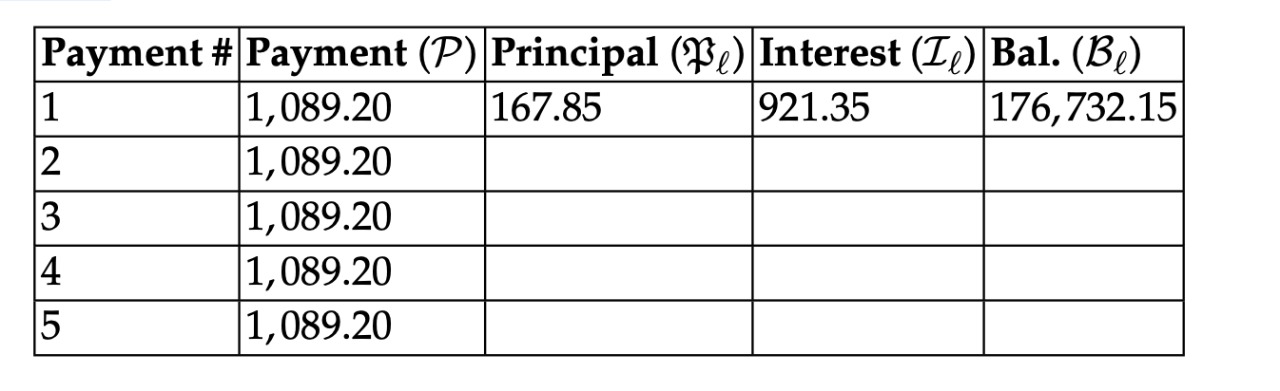

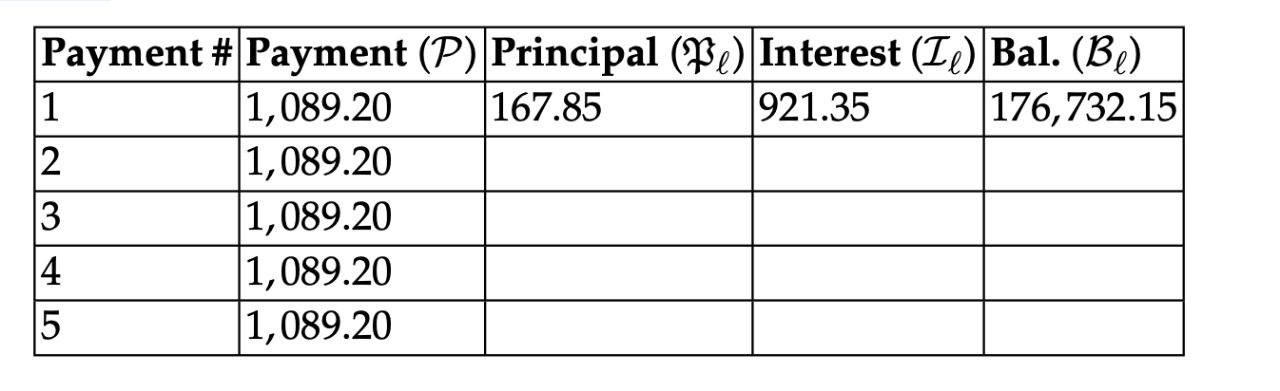

QUESTION 2: Fill out the amortization schedule below, which is for the first 5 months of the loan (see picture)....

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Economics

Authors: Dominick Salvatore

12th edition

9781118955727, 1118955765, 1118955722, 978-1118955765