Everything is included What is total surplus? The difference between the maximum amount a buyer will pay for a good and the cost to the

Everything is included

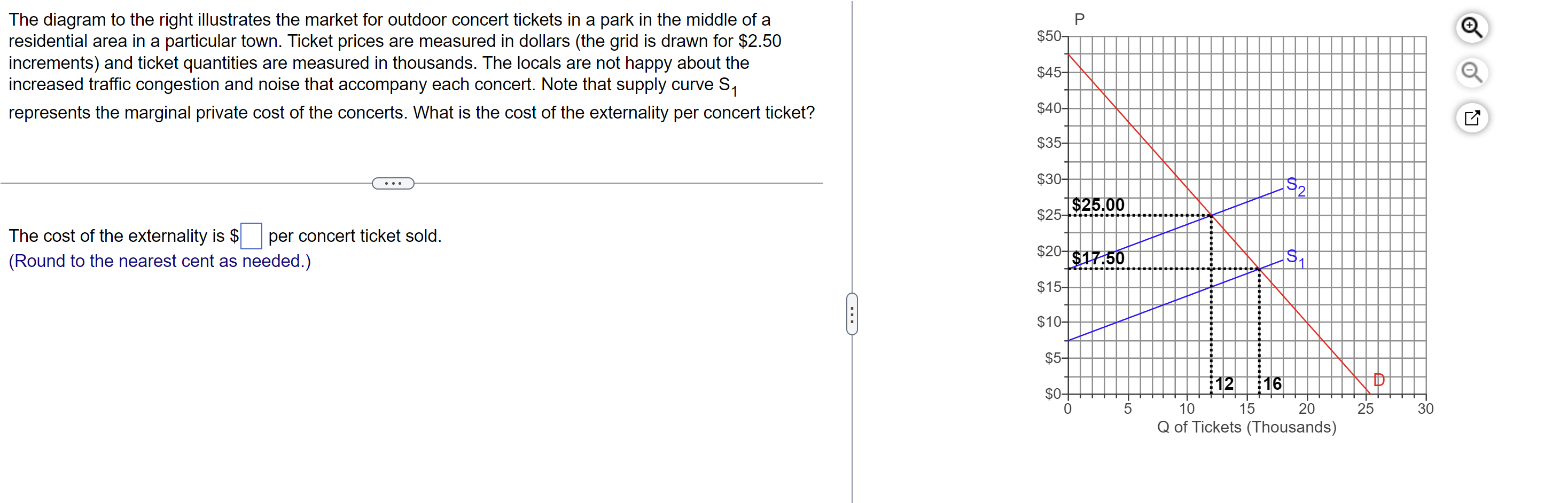

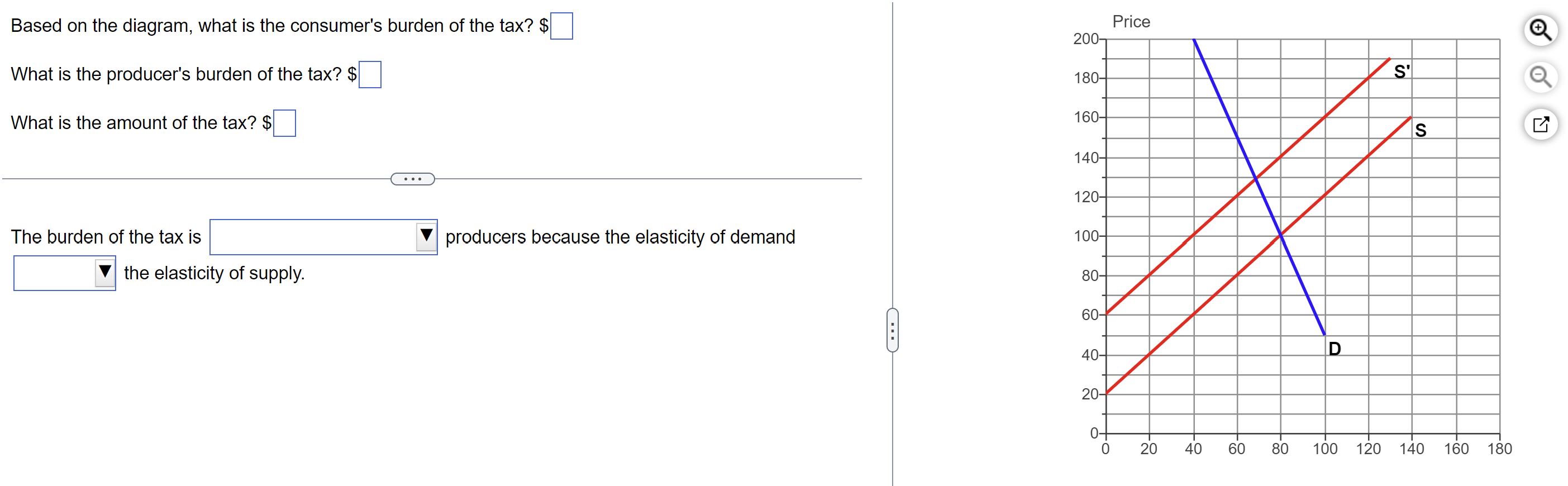

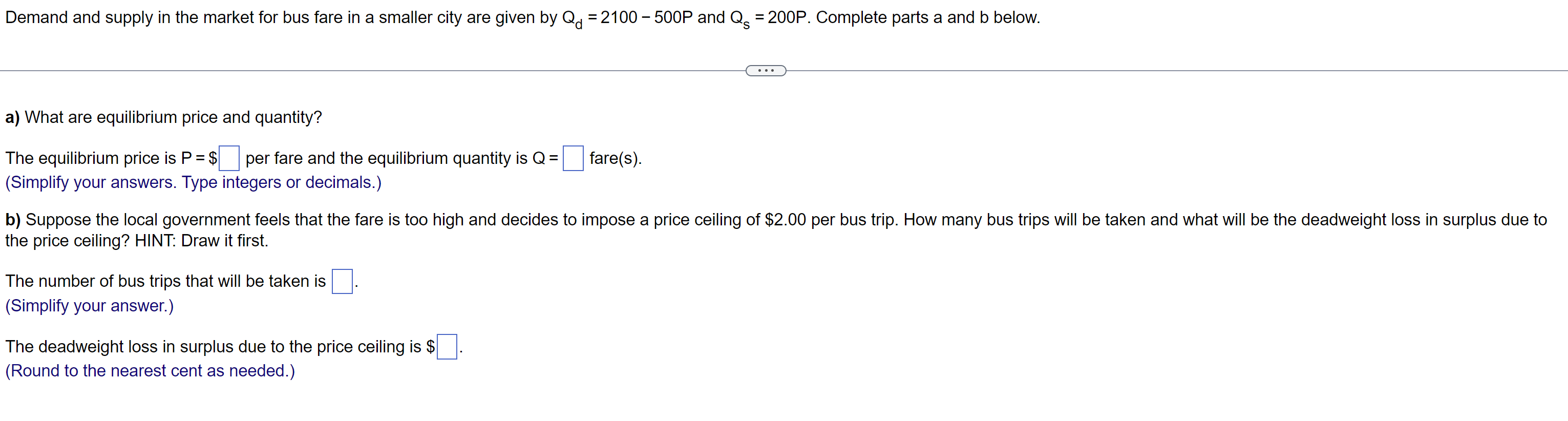

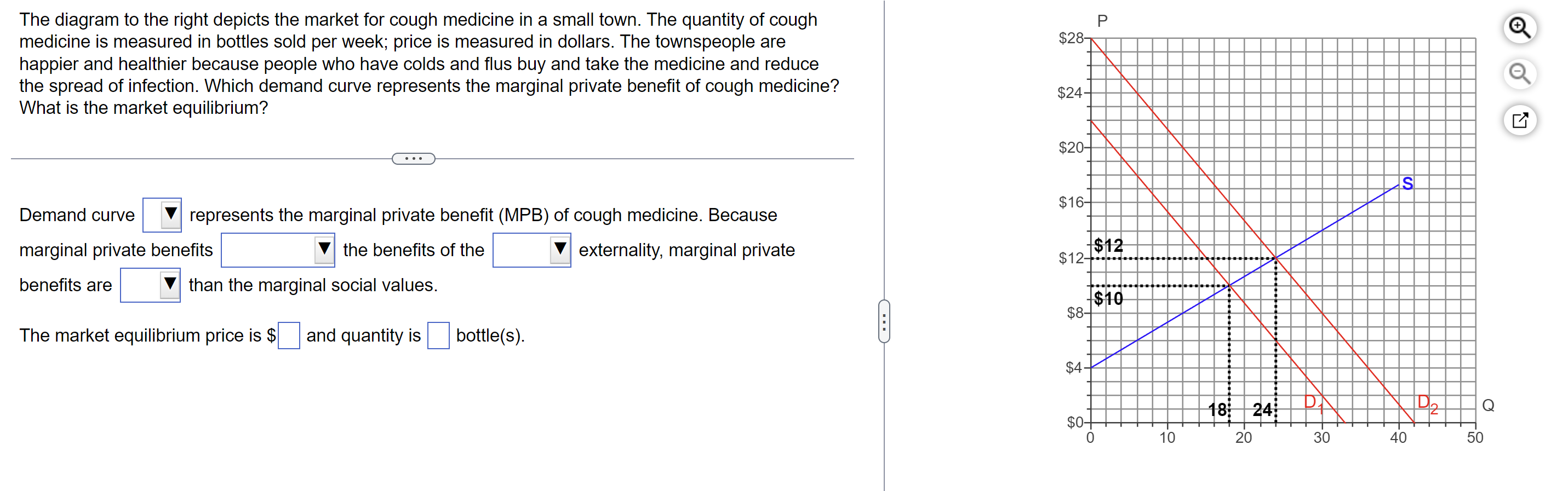

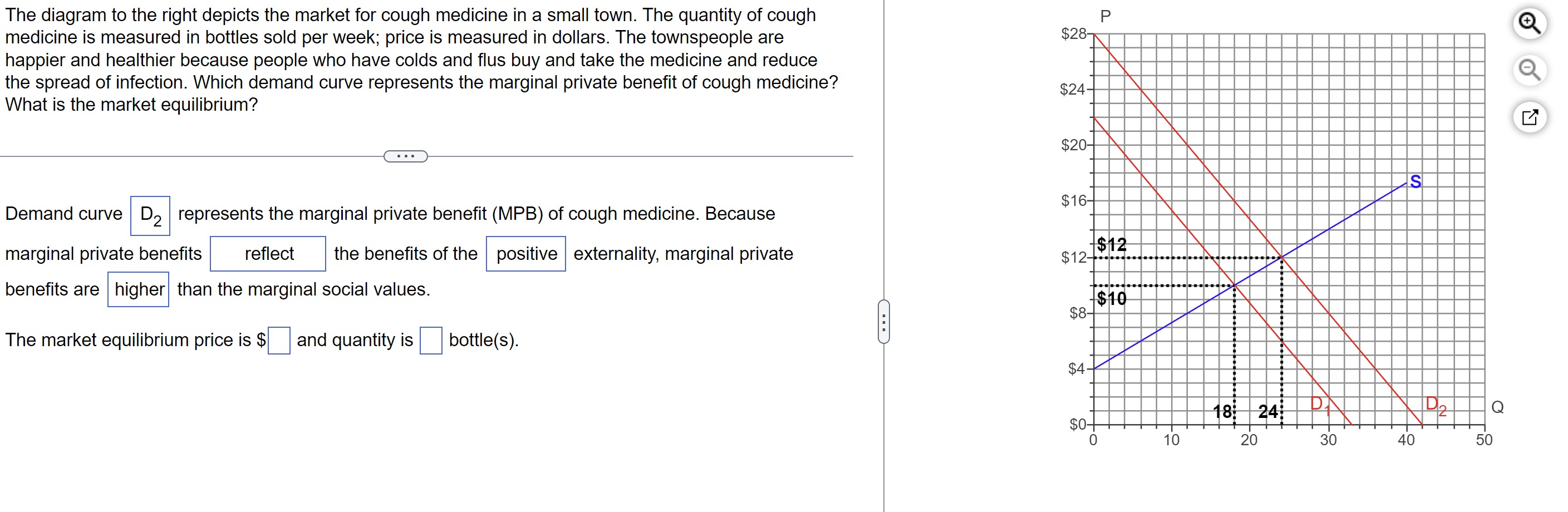

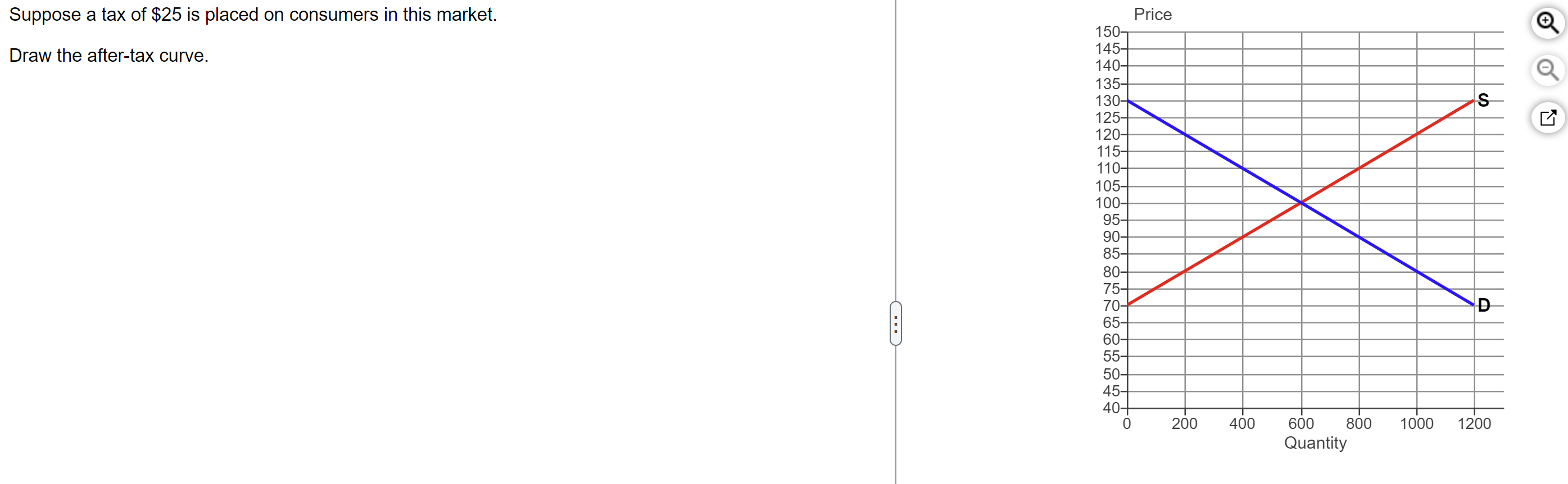

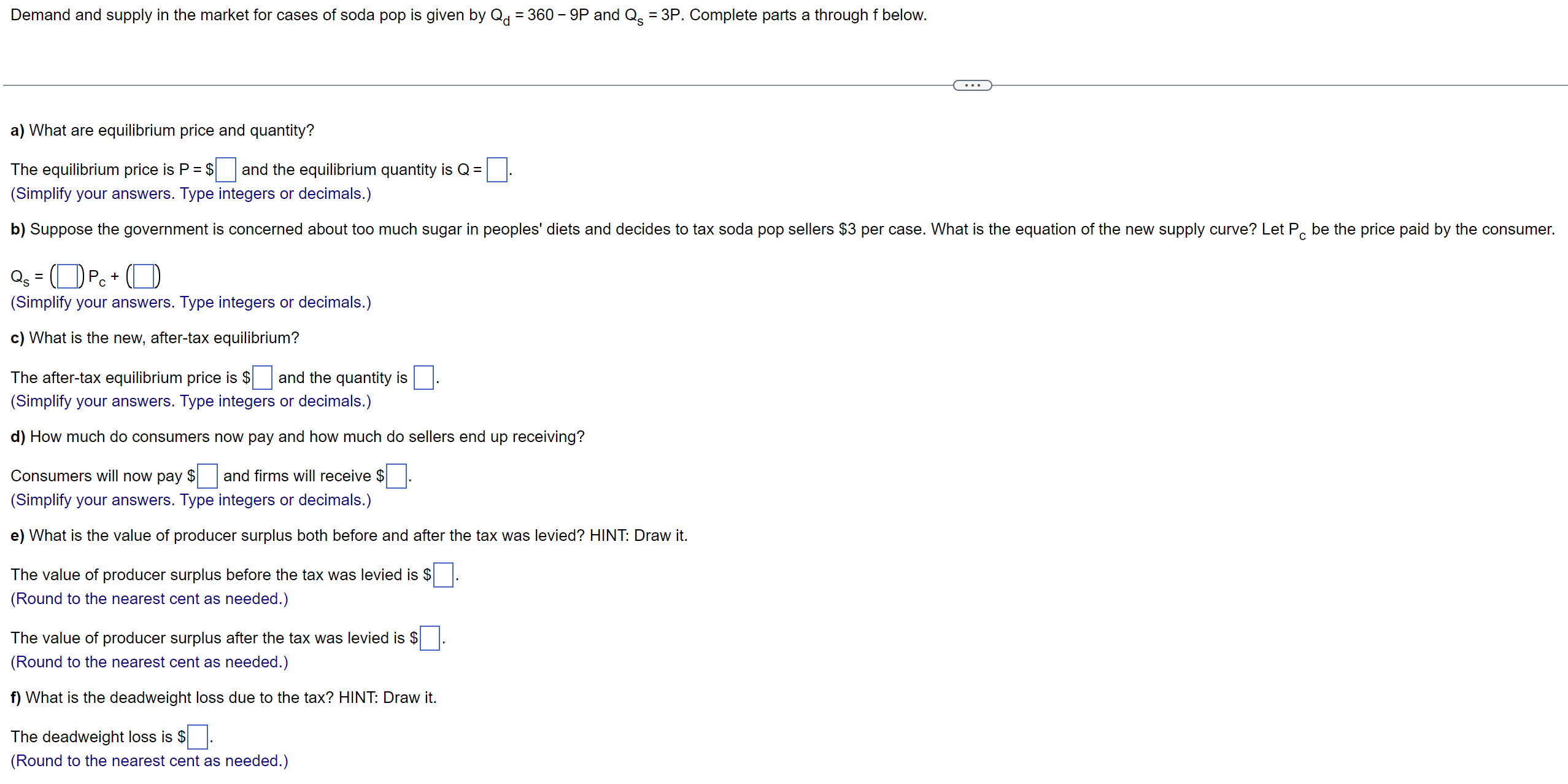

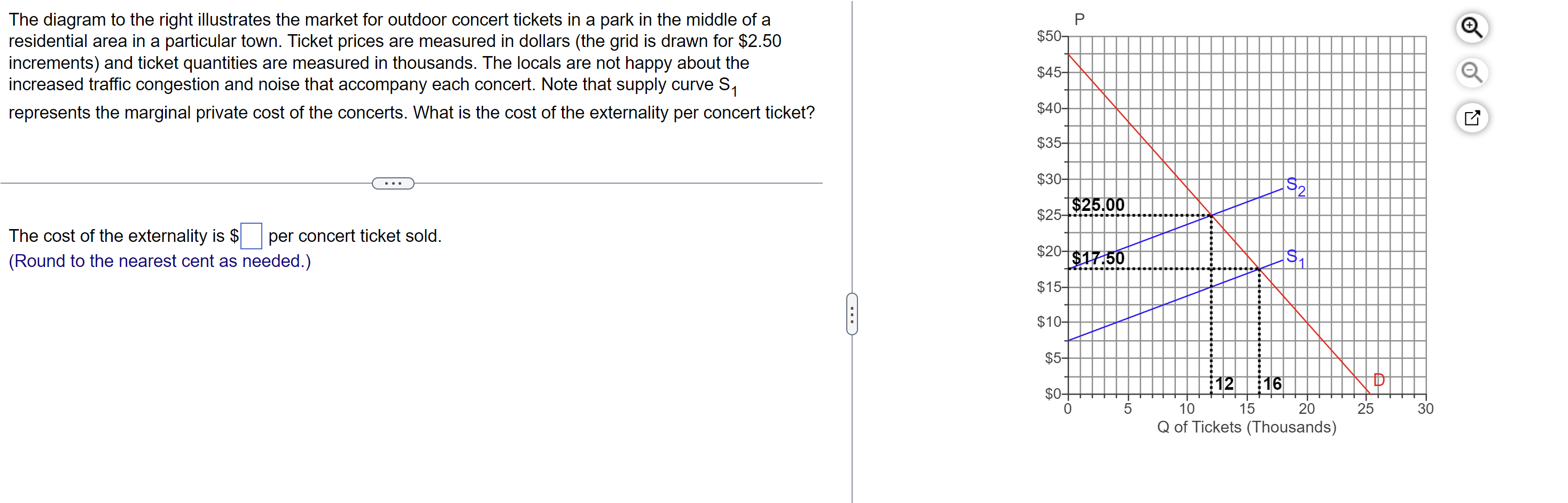

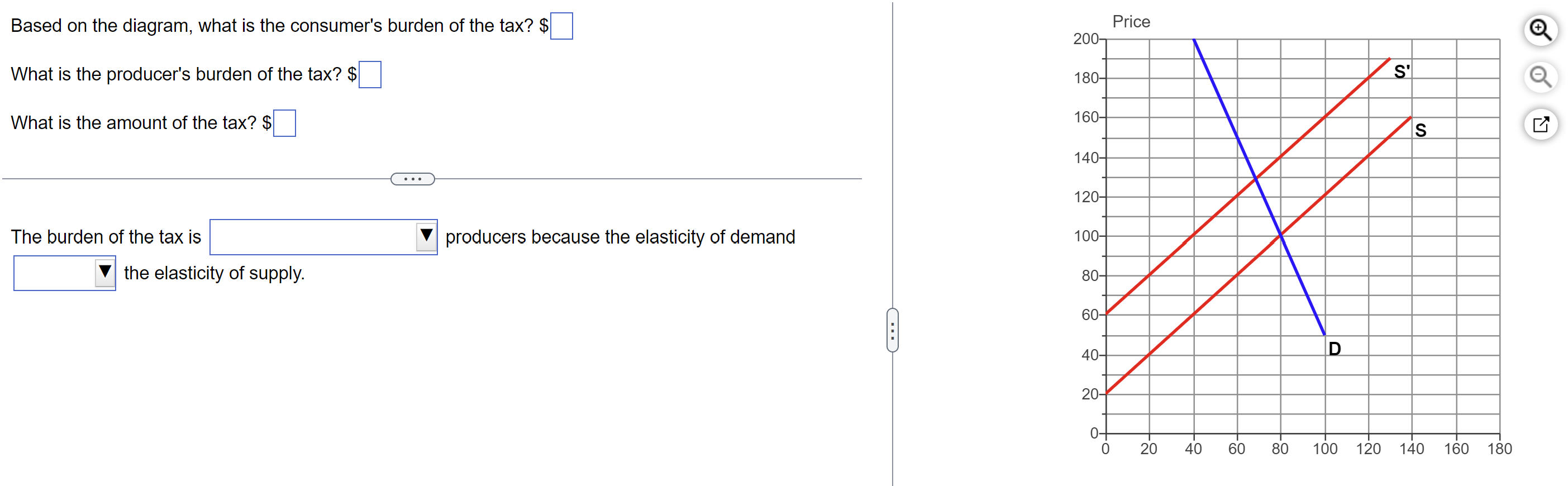

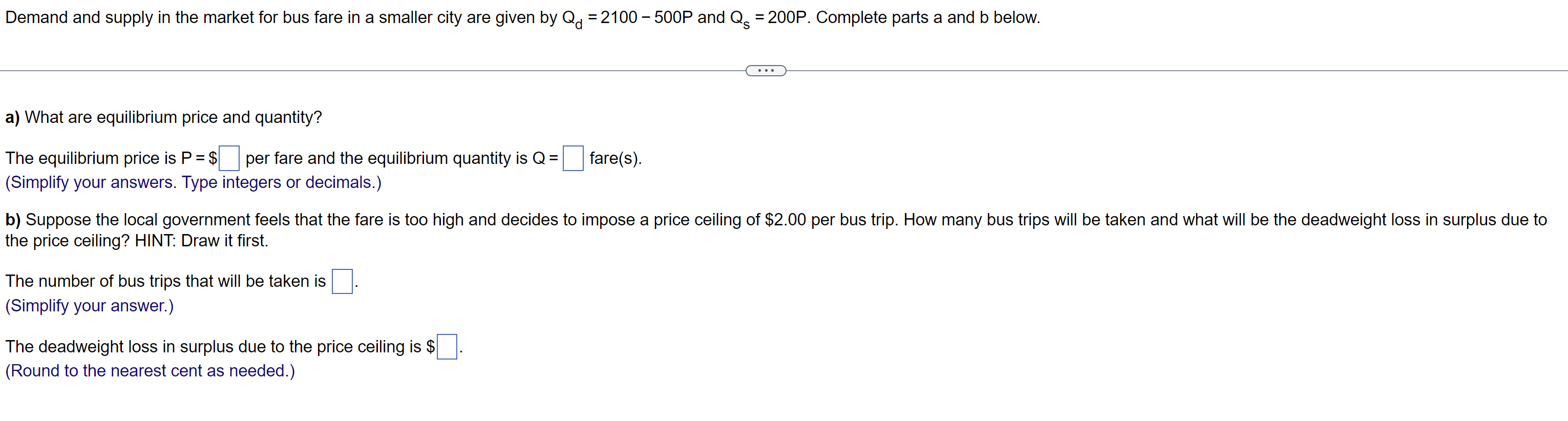

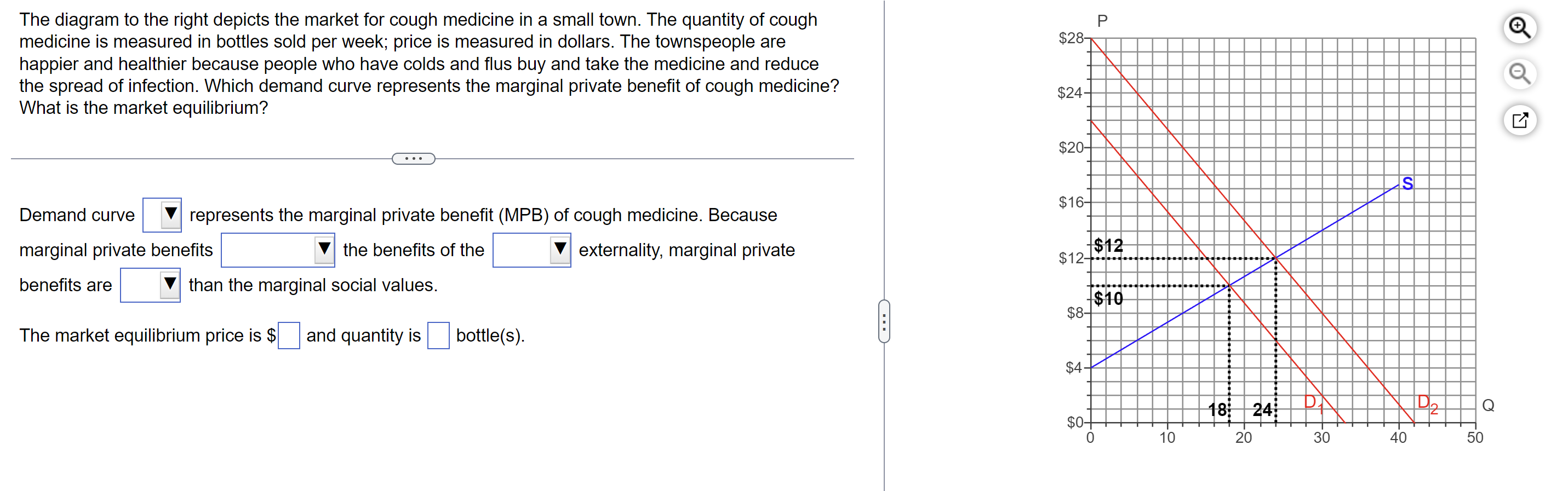

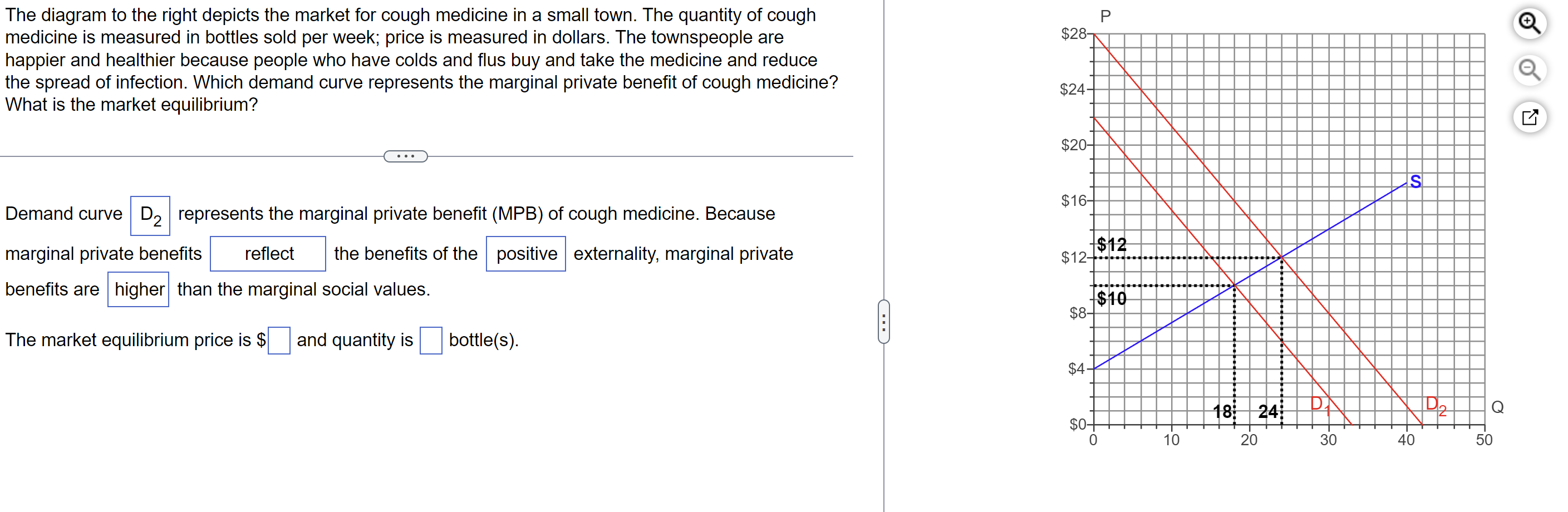

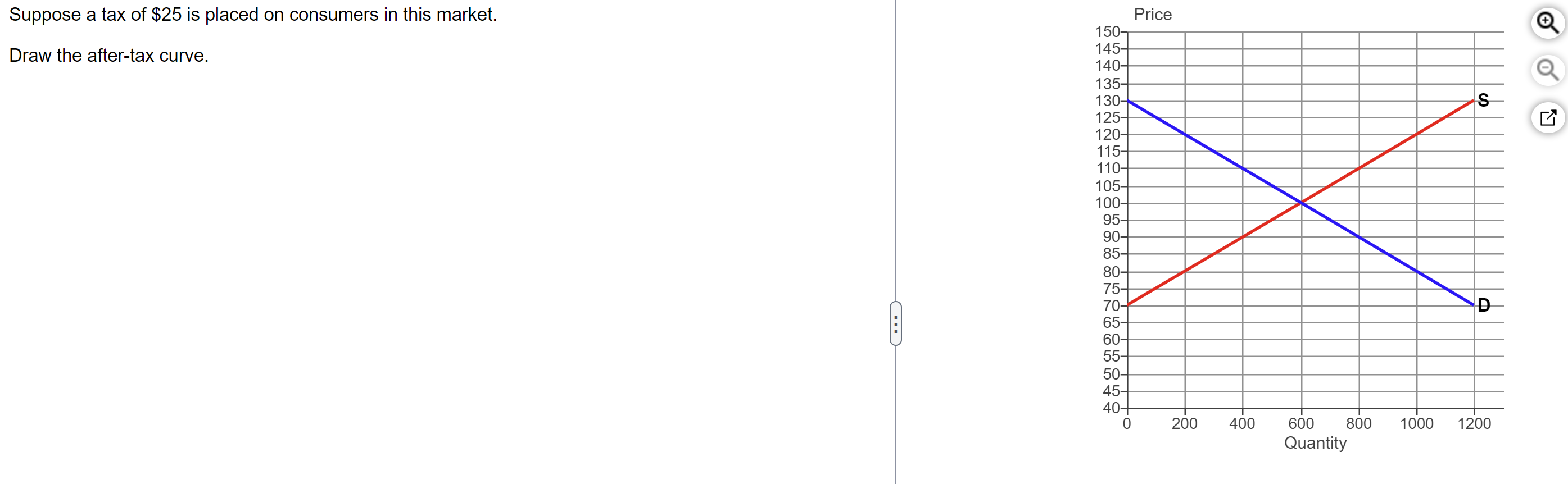

What is total surplus? The difference between the maximum amount a buyer will pay for a good and the cost to the seller. The sum of the consumer's willingness to pay and the cost to the seller. The difference between the maximum amount a buyer will pay for a good and the price they actually have to pay. 9.097? The sum of the consumer's willingness to pay and the price they actually have to pay. Binding price ceilings lead to permanent causing Non-binding price ceilings lead to causing the market price toThe diagram to the right illustrates the market for outdoor concert tickets in a park in the middle of a residential area in a particular town. Ticket prices are measured in dollars (the grid is drawn for $2.50 P $50- increments) and ticket quantities are measured in thousands. The locals are not happy about the increased traffic congestion and noise that accompany each concert. Note that supply curve S, $45- represents the marginal private cost of the concerts. What is the cost of the externality per concert ticket? $40- $35- . . . $30- The cost of the externality is $ per concert ticket sold. $25.00 (Round to the nearest cent as needed.) $20-$17.50 $15- $10- $5 $0- 12 16 D 5 10 15 20 25 30 Q of Tickets (Thousands)Which of the following goods are rival in consumption? . Common resources and club goods A B. Public goods and common resources C. Common resources and private goods D . Club goods and private goods Based on the diagram, what is the consumer's burden of the tax? $ What is the producer's burden of the tax? $ What is the amount of the tax? 35 The burden of the tax is V the elasticity of supply. producers because the elasticity of demand 200 180 160 140 120 100 80 40 20 60 Price 0 20 40 60 80 100 120 140 160 180 Demand and supply in the market for bus fare in a smaller city are given by Qd = 2100 500P and QS =200P. Complete parts a and b below. a) What are equilibrium price and quantity? The equilibrium price is P = $ per fare and the equilibrium quantity is Q = fare(s). (Simplify your answers. Type integers or decimals.) b) Suppose the local government feels that the fare is too high and decides o impose a price ceiling of $2.00 per bus trip. How many bus trips will be taken and what will be the deadweight loss in surplus due to the price ceiling? HINT: Draw it first, The number of bus trips that will be taken is (Simplify your answer.) The deadweight loss in surplus due to the price ceiling is 8% (Round to the nearest cent as needed.) The diagram to the right depicts the market for cough medicine in a small town The quantity of cough medicine is measured in bottles sold per week; price is measured in dollars. The townspeople are happier and healthier because people who have colds and flus buy and take the medicine and reduce the spread of infection. Which demand curve represents the marginal private benet of cough medicine? What is the market equilibrium? Demand curve Y represents the marginal private benet (MP3) of cough medicine Because marginal private benefits V the benets of the V externality, marginal private benefits are V than the marginal social values, The market equilibrium price is $ and quantity is bottle(s). $20 $16 $12M\" O 10 20 30 4O 50 9,0 The diagram to the right depicts the market for cough medicine in a small town. The quantity of cough medicine is measured in bottles sold per week; price is measured in dollars. The townspeople are happier and healthier because people who have colds and flus buy and take the medicine and reduce the spread of infection Which demand curve represents the marginal private benefit of cough medicine? What is the market equilibrium? Demand curve D2 represents the marginal private benefit (MP8) of cough medicine. Because marginal private benets reflect benefits are higher than the marginal social values The market equilibrium price is $ and quantity is the benefits of the positive bottle(s). externality, marginal private $28 $24 $20 $16 $8 $4 $0 gangliaw Elm\" //' ' 20 30 40 50 9,0 E'x. Suppose a tax of $25 is placed on consumers in this market. Draw the after-tax curve. 150 145 140 135 130 125 120 115 110 105 100 95 90 85 80 75 70 65 60 55 50 45 40 Price 200 400 600 800 Quantity 1000 1200 99 Demand and supply in the market for cases of soda pop is given by Qd = 360 9F and Q5 = 3P. Complete parts a through f below. a) What are equilibrium price and quantity? The ecuilibrium price is P = $ and the equilibrium quantity is Q = (Simplify your answers. Type integers or decimals.) b) Suppose the government is concerned about too much sugar in peoples' diets and decides to tax soda pop sellers $3 per case. What is the equation of the new supply curve? Let PC be the price paid by the consumer. QS = PC + ( (Simplify your answers. Type integers or decimals.) c) What is the new, after-tax equilibrium? The after-tax equilibrium price is $ and the quantity is (Simplify your answers. Type integers or decimals.) d) How much do consumers now pay and how much do sellers end up receiving? Consumers will now pay $ and rms will receive 25 (Simplify your answers. Type integers or decimals.) e) What is the value of producer surplus both before an: after the tax was levied? HINT: Draw it. The value of producer surplus before the tax was levied is 85 (Round to the nearest cent as needed.) The value of producer surplus after the tax was levied is $ (Round to the nearest cent as needed.) f) What is the deadweight loss due to the tax? HINT: Draw it. The deadweight loss is $ . (Round to the nearest cent as needed.) What happens to consumer and producer surplus when the price changes? When the price falls, consumer surplus falls and producer surplus falls. When the price rises, consumer surplus rises and producer surplus falls. When the price falls, consumer surplus rises and producer surplus falls. When the price rises, consumer surplus rises and producer surplus rises

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance