Answered step by step

Verified Expert Solution

Question

1 Approved Answer

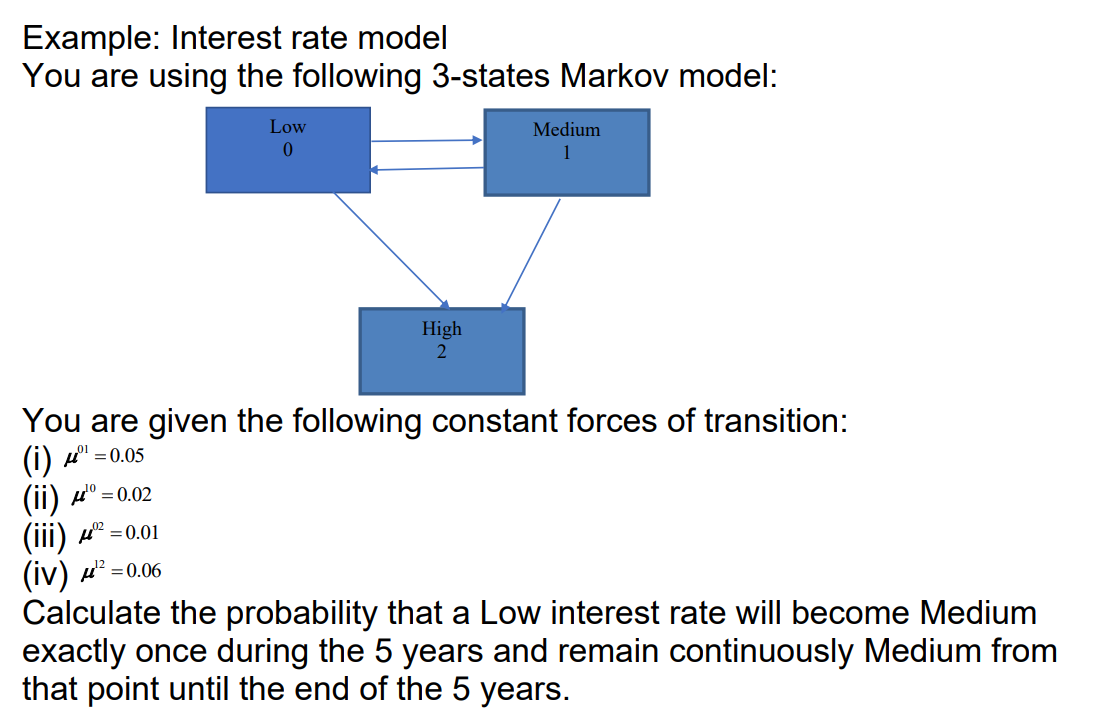

Example: Interest rate model You are using the following 3-states Markov model: You are given the following constant forces of transition: (i) 01=0.05 (ii) 10=0.02

Example: Interest rate model You are using the following 3-states Markov model: You are given the following constant forces of transition: (i) 01=0.05 (ii) 10=0.02 (iii) 02=0.01 (iv) 12=0.06 Calculate the probability that a Low interest rate will become Medium exactly once during the 5 years and remain continuously Medium from that point until the end of the 5 years

Example: Interest rate model You are using the following 3-states Markov model: You are given the following constant forces of transition: (i) 01=0.05 (ii) 10=0.02 (iii) 02=0.01 (iv) 12=0.06 Calculate the probability that a Low interest rate will become Medium exactly once during the 5 years and remain continuously Medium from that point until the end of the 5 years Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Regulation In The EU From Resilience To Growth

Authors: Raphaël Douady , Clément Goulet, Pierre-Charles Pradier

1st Edition

3319442864,3319442872