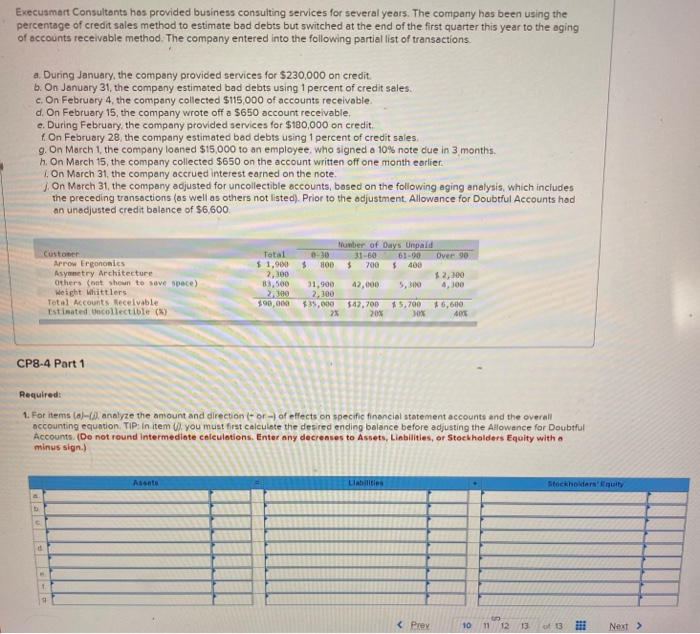

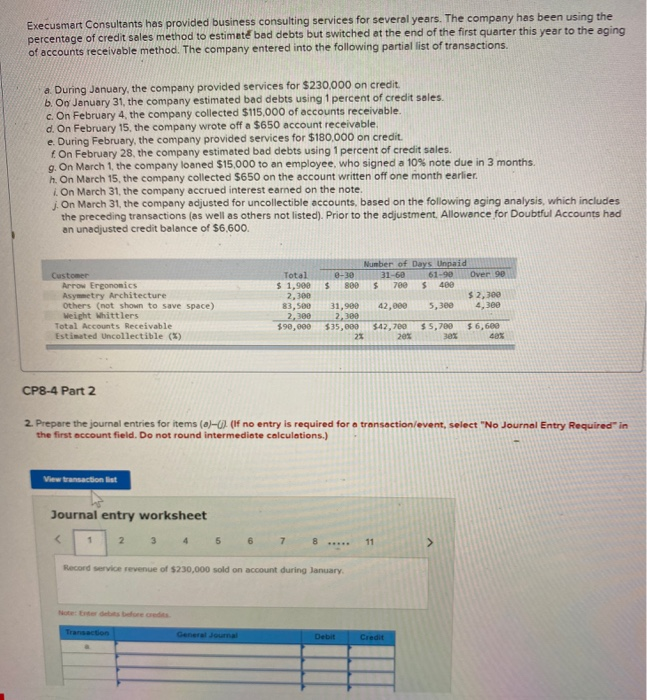

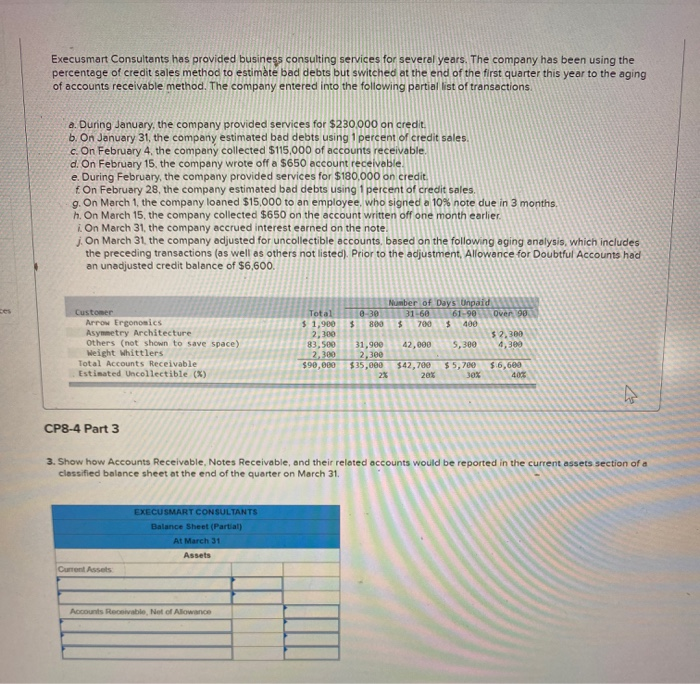

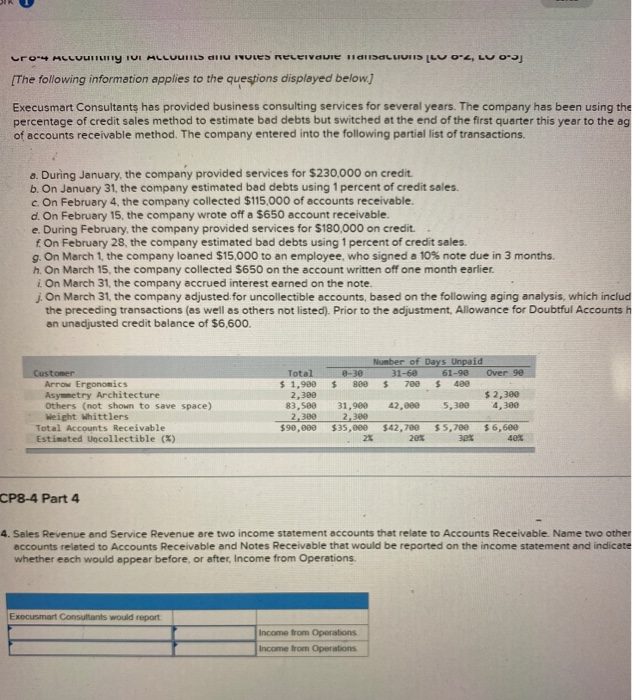

Execusmart Consultants has provided business consulting services for several years. The company has been using the percentage of credit sales method to estimate bad debts but switched at the end of the first quarter this year to the aging of accounts receivable method. The company entered into the following partial list of transactions a. During January, the company provided services for $230,000 on credit. b. On January 31, the company estimated bad debts using 1 percent of credit sales c. On February 4, the company collected $115,000 of accounts receivable d. On February 15, the company wrote off a $650 account receivable. e. During February, the company provided services for $180,000 on credit. 1 On February 28, the company estimated bad debts using 1 percent of credit sales 9. On March 1, the company loaned $15,000 to an employee, who signed a 10% note due in 3 months h. On March 15, the company collected $650 on the account written off one month earlier. 1. On March 31, the company accrued interest earned on the note. J. On March 31, the company adjusted for uncollectible accounts, based on the following aging analysis, which includes the preceding transactions as well as others not listed). Prior to the adjustment. Allowance for Doubtful Accounts had an unadjusted credit balance of $6,600 Number of Days Unpaid 0.30 1-60 61-00 HOD $ 700 $ 400 Over 90 $ Customer Arrow Ergonomics Asymmetry Architecture Others (not shown to save space) Weight Mittlers Total Accounts Receivable Estimated Uncollectible (%) Total $1,900 2,300 83,500 2,300 $90.00 42,000 $ 2,00 4,300 5,300 31,900 2,300 $35,000 $42.700 15,00 BOX $6,600 GIVE CP8.4 Part 1 Required: 1. For items (a)- analyze the amount and direction for of effects on specific financial statement accounts and the overall accounting equation. TIP: In item you must first calculate the desired ending balance before adjusting the Allowance for Doubtful Accounts. (Do not round Intermediate calculations. Enter any decreases to Assets, Liabilities, or Stockholders Equity with a minus sign.) Stockholders' Equity Execusmart Consultants has provided business consulting services for several years. The company has been using the percentage of credit sales method to estimat& bad debts but switched at the end of the first quarter this year to the aging of accounts receivable method. The company entered into the following partial list of transactions. a. During January, the company provided services for $230,000 on credit b. On January 31, the company estimated bad debts using 1 percent of credit sales c. On February 4, the company collected $115,000 of accounts receivable. d. On February 15, the company wrote off a $650 account receivable e. During February, the company provided services for $180,000 on credit. On February 28, the company estimated bad debts using 1 percent of credit sales. 9. On March 1, the company loaned $15,000 to an employee, who signed a 10% note due in 3 months. h. On March 15, the company collected $650 on the account written off one month earlier. 1. On March 31, the company accrued interest earned on the note. j. On March 31, the company adjusted for uncollectible accounts, based on the following aging analysis, which includes the preceding transactions (as well as others not listed). Prior to the adjustment, Allowance for Doubtful Accounts had an unadjusted credit balance of $6,600. Customer Arrow Ergonomics Asymmetry Architecture Others (not shown to save space) Weight Whittlers Total Accounts Receivable Estimated Uncollectible (*) Total $ 1,900 2.300 83,500 2,380 $90,000 Number of Days Unpaid 0-30 31-60 61-90 Over 90 $ 800 $ 700 S 400 $ 2,300 31,900 42,000 5,300 4.300 2,380 $35,000 $42,700 $5,700 $6,600 2% 20% 30% 40% CP8-4 Part 2 2. Prepare the journal entries for items (0-0) (If no entry is required for a transaction event, select "No Journal Entry Required in the first account field. Do not round intermediate calculations.) View transaction list Journal entry worksheet 1 2 3 4 5 6 7 8 ..... Record service revenue of $230,000 sold on account during January Transaction Debit Credit Execusmart Consultants has provided business consulting services for several years. The company has been using the percentage of credit sales method to estimate bad debts but switched at the end of the first quarter this year to the aging of accounts receivable method. The company entered into the following partial list of transactions 6. During January, the company provided services for $230,000 on credit b. On January 31, the company estimated bad debts using 1 percent of credit sales. c. On February 4, the company collected $115,000 of accounts receivable. d On February 15, the company wrote off a $650 account receivable. e. During February, the company provided services for $180,000 on credit On February 28, the company estimated bad debts using 1 percent of credit sales. 0. On March 1, the company loaned $15,000 to an employee, who signed a 10% note due in 3 months h. On March 15, the company collected $650 on the account written off one month earlier i. On March 31, the company accrued interest earned on the note. On March 31. the company adjusted for uncollectible accounts, based on the following aging analysis, which includes the preceding transactions as well as others not listed). Prior to the adjustment, Allowance for Doubtful Accounts had an unadjusted credit balance of $6,600. Customer Arrow Ergonomics Asymmetry Architecture Others (not shown to save space) Weight Whittlers Total Accounts Receivable Estimated Uncollectible (x) Total $ 1,900 2.300 83,500 2,380 $90,000 Number of Days Unpaid 0-30 31-6061-90 over 90 $ 800 $ 700 $ 400 $ 2.300 31,900 42,000 3,300 1,300 2,300 $35,000 $42,200 $5,200 $6.600 2% 20% 30% CP8-4 Part 3 3. Show how Accounts Receivable, Notes Receivable, and their related accounts would be reported in the current assets section of a classified balance sheet at the end of the quarter on March 31. EXECU SMART CONSULTANTS Balance Sheet (Partial) At March 31 Assets cro-4 MELUUTTLIITY TUI MLLUUIILS CITU rules Receivable 11 SALLIVIIS LLU OZ, LU 03) (The following information applies to the questions displayed below) Execusmart Consultants has provided business consulting services for several years. The company has been using the percentage of credit sales method to estimate bad debts but switched at the end of the first quarter this year to the ag of accounts receivable method. The company entered into the following partial list of transactions a. During January, the company provided services for $230,000 on credit. b. On January 31, the company estimated bad debts using 1 percent of credit sales. c. On February 4, the company collected $115,000 of accounts receivable. d. On February 15, the company wrote off a $650 account receivable e. During February, the company provided services for $180,000 on credit. f On February 28, the company estimated bad debts using 1 percent of credit sales. g. On March 1, the company loaned $15,000 to an employee, who signed a 10% note due in 3 months h. On March 15, the company collected $650 on the account written off one month earlier. i. On March 31, the company accrued interest earned on the note. j. On March 31, the company adjusted for uncollectible accounts, based on the following aging analysis, which includ the preceding transactions (as well as others not listed). Prior to the adjustment, Allowance for Doubtful Accounts h an unadjusted credit balance of $6,600. Customer Arrow Ergonomics Asymmetry Architecture Others (not shown to save space) Weight Whittlers Total Accounts Receivable Estimated Uncollectible (%) Total $ 1,900 2.300 83,500 2,380 $90,000 Number of Days Unpaid 0-30 31-60 61-90 Over 90 $ 800 $ 700 $ 400 $ 2,300 31,900 42,000 5,300 4,380 2.300 $35,000 $42,780 $5,700 56,6ee 2% 20% 30 40% CP8-4 Part 4 4. Sales Revenue and Service Revenue are two income statement accounts that relate to Accounts Receivable. Name two other accounts related to Accounts Receivable and Notes Receivable that would be reported on the income statement and indicate whether each would appear before or after Income from Operations Exocusmart Consultants would report Income from Operations Income from Operations