Answered step by step

Verified Expert Solution

Question

1 Approved Answer

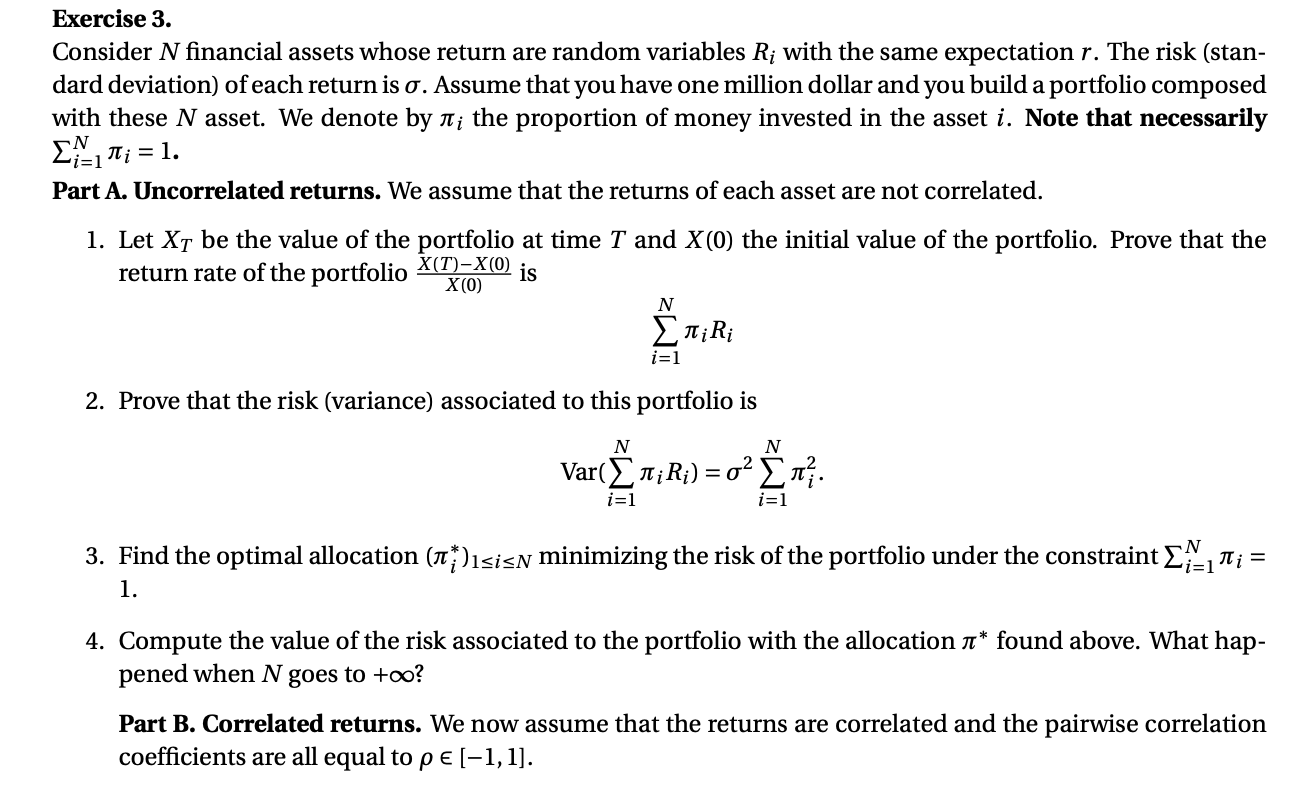

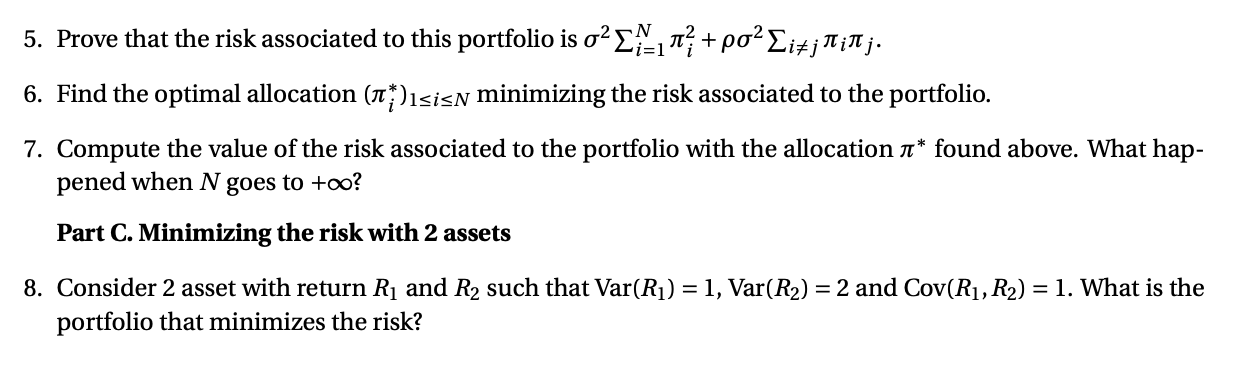

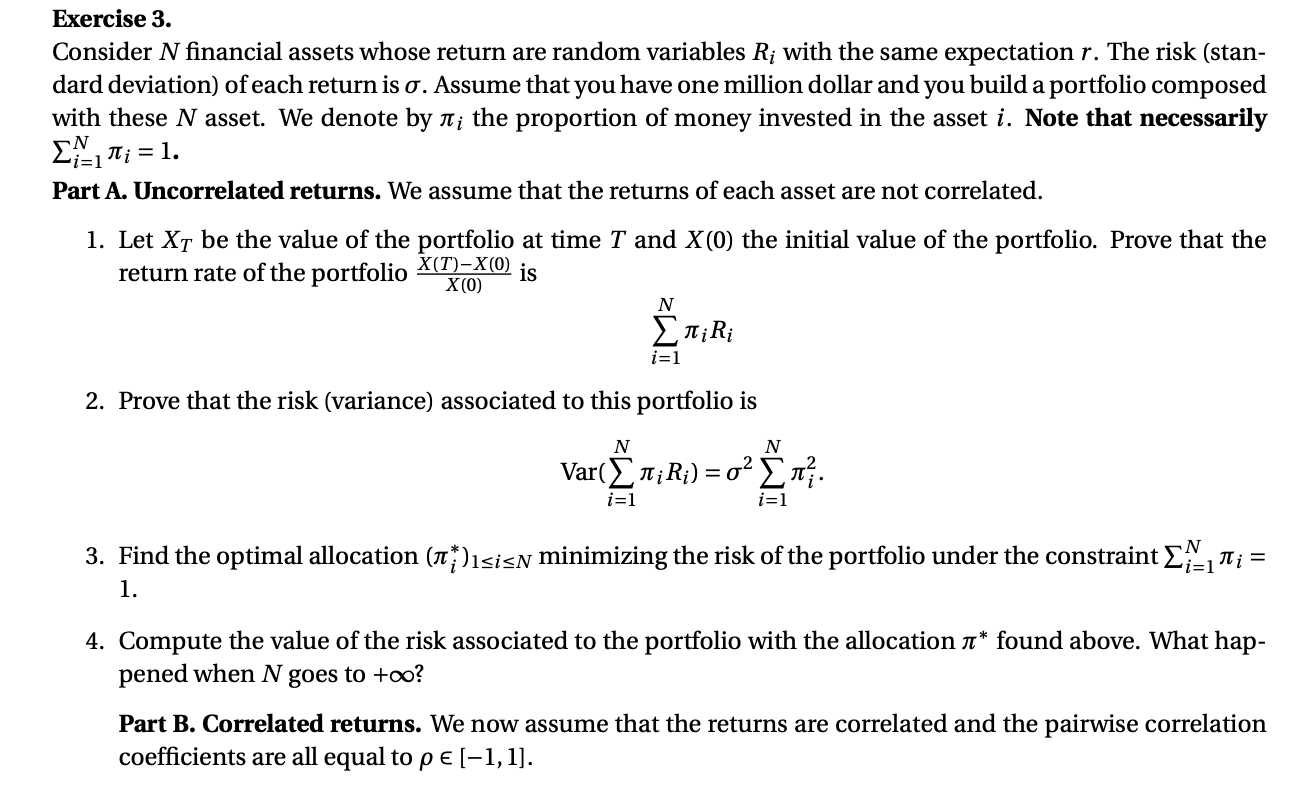

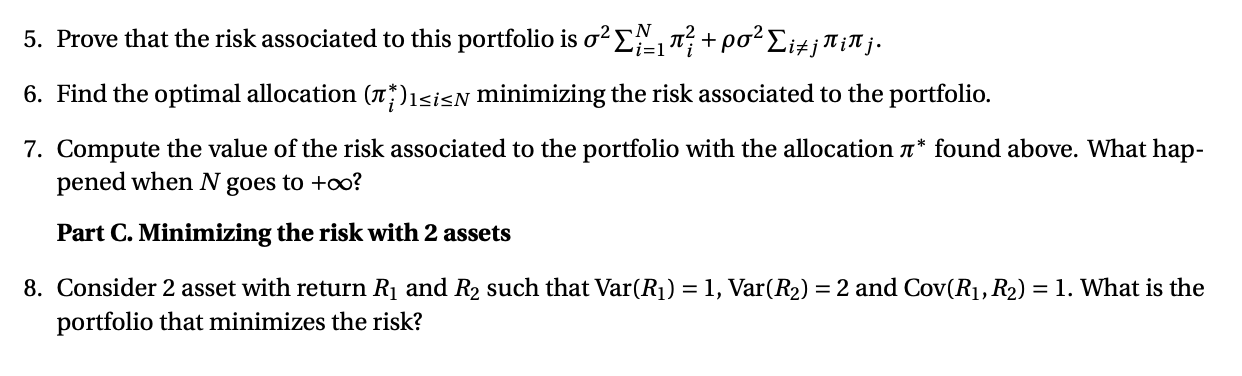

Exercise 3. Consider N nancial assets whose return are random variables R;- with the same expectation r. The risk (stan- dard deviation} of each return

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Calculus Single And Multivariable

Authors: Deborah Hughes Hallett, Andrew M Gleason, William G McCallum, Daniel E Flath, Patti Frazer Lock, Sheldon P Gordon, David O Lomen, David Lovelock, Brad

6th Edition

1118475712, 9781118475713