Answered step by step

Verified Expert Solution

Question

1 Approved Answer

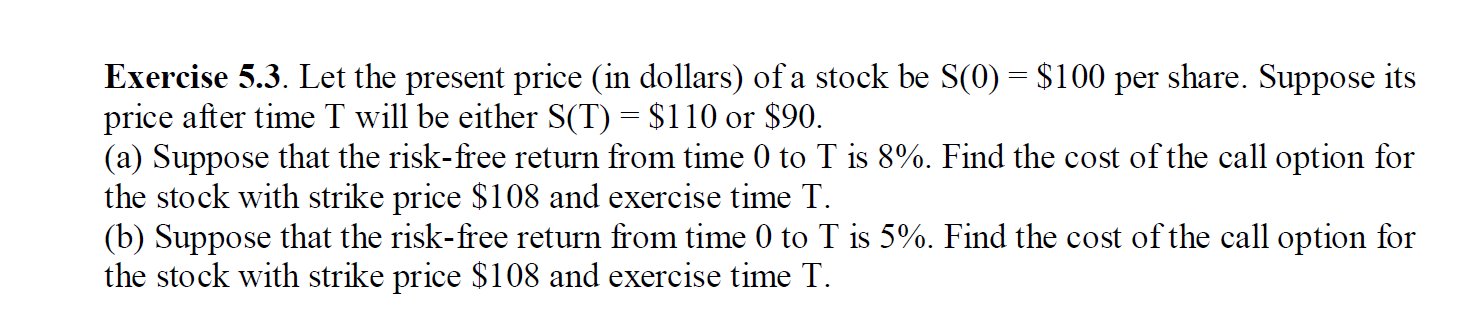

- Exercise 5.3. Let the present price (in dollars) of a stock be S(0) = $100 per share. Suppose its price after time I will

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

How To Get Money For College Financing Your Future Beyond Federal Aid

Authors: Mark D. Snider

1st Edition

0768928869, 978-0768928860