Exercise # 5-7

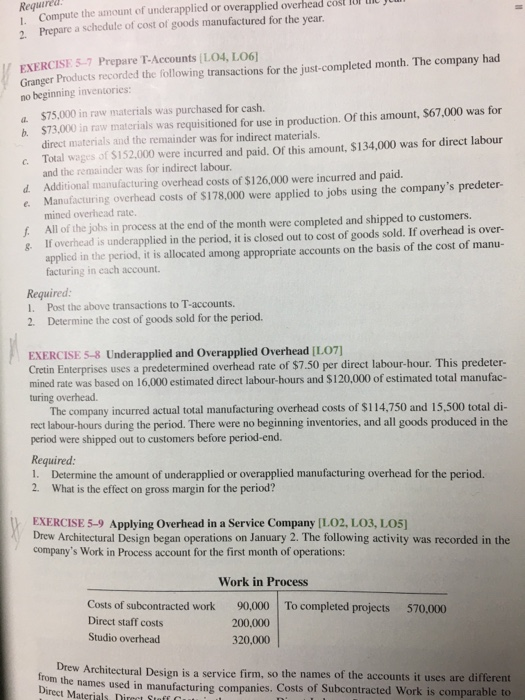

Required! 2 Compute the amount of underapplied or overapplied overhead cost IUI I J Prepare a schedule of cost of goods manufactured for the year. EXERCISE 5-7 Prepare T-Accounts (L04, LO6] Granger Products recorded the following transactions for the just completed month. The company had no beginning inventories: a $75,000 in raw materials was purchased for cash. be $73.000 in raw materials was requisitioned for use in production. Of this amount, $67,000 was for direct materials and the remainder was for indirect materials. C. Total wages of $152,000 were incurred and paid. Of this amount, $134,000 was for direct labour and the remainder was for indirect labour. d Additional manufacturing overhead costs of $126,000 were incurred and paid. e Manufacturing overhead costs of $178,000 were applied to jobs using the company's predeter- mined overhead rate. 1. All of the jobs in process at the end of the month were completed and shipped to customers. 8. If overhead is underapplied in the period, it is closed out to cost of goods sold. If overhead is over- applied in the period, it is allocated among appropriate accounts on the basis of the cost of manu- facturing in each account. Required: 1. Post the above transactions to T-accounts. 2. Determine the cost of goods sold for the period. EXERCISE 5-8 Underapplied and Overapplied Overhead [L07] Cretin Enterprises uses a predetermined overhead rate of $7.50 per direct labour-hour. This predeter- mined rate was based on 16,000 estimated direct labour-hours and $120,000 of estimated total manufac. turing overhead. The company incurred actual total manufacturing overhead costs of $114,750 and 15,500 total di rect labour-hours during the period. There were no beginning inventories, and all goods produced in the period were shipped out to customers before period-end. Required: 1. Determine the amount of underapplied or overapplied manufacturing overhead for the period. 2. What is the effect on gross margin for the period? EXERCISE 5-9 Applying Overhead in a Service Company (LO2, LO3, L05] Drew Architectural Design began operations on January 2. The following activity was recorded in the company's Work in Process account for the first month of operations: Work in Process To completed projects 570,000 Costs of subcontracted work Direct staff costs Studio overhead 90,000 200,000 320,000 Drew Architectural Desien is a service firm, so the names of the accounts it uses are different the names used in manufacturing companies. Costs of Subcontracted Work is comparable to Direct Materials Direct Stoff