Exercise 7-21B Complete the accounting cycle using long-term asset transactions (LO7-4, 7-7)

Exercise 7-21B Complete the accounting cycle using long-term asset transactions (LO7-4, 7-7)

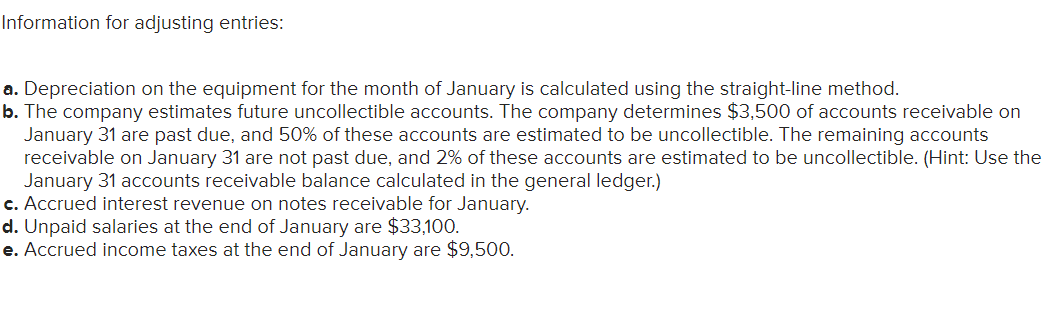

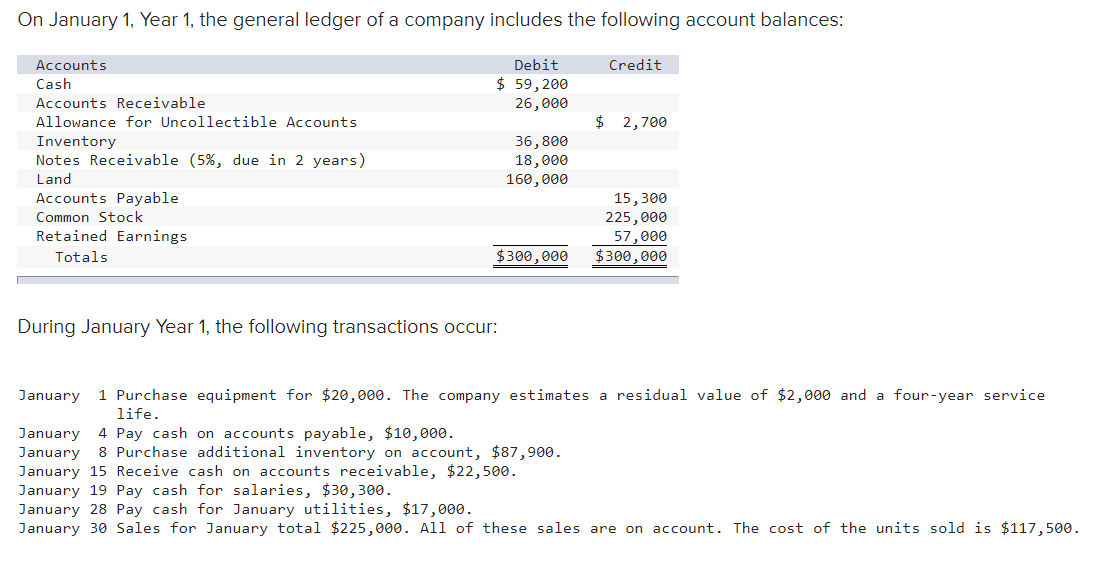

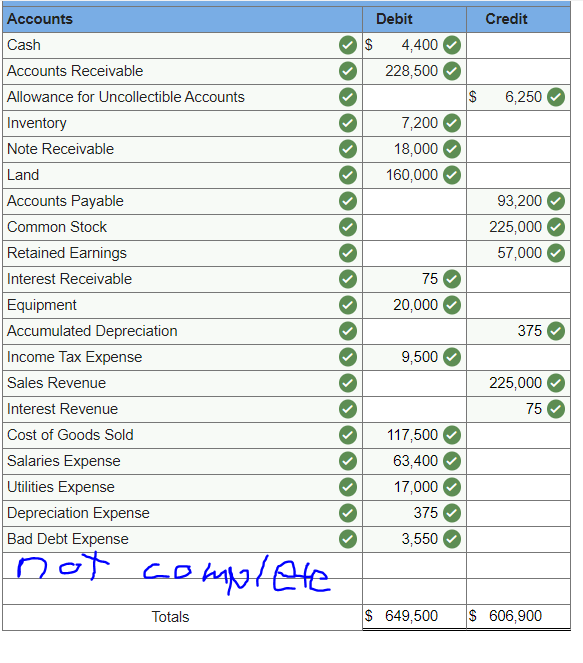

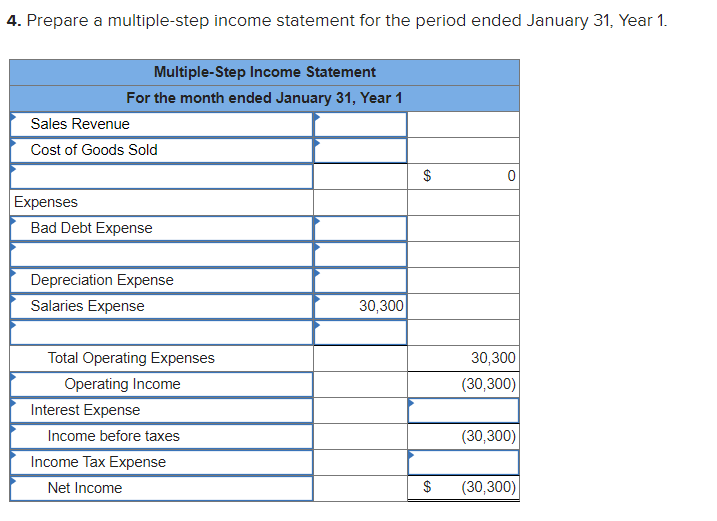

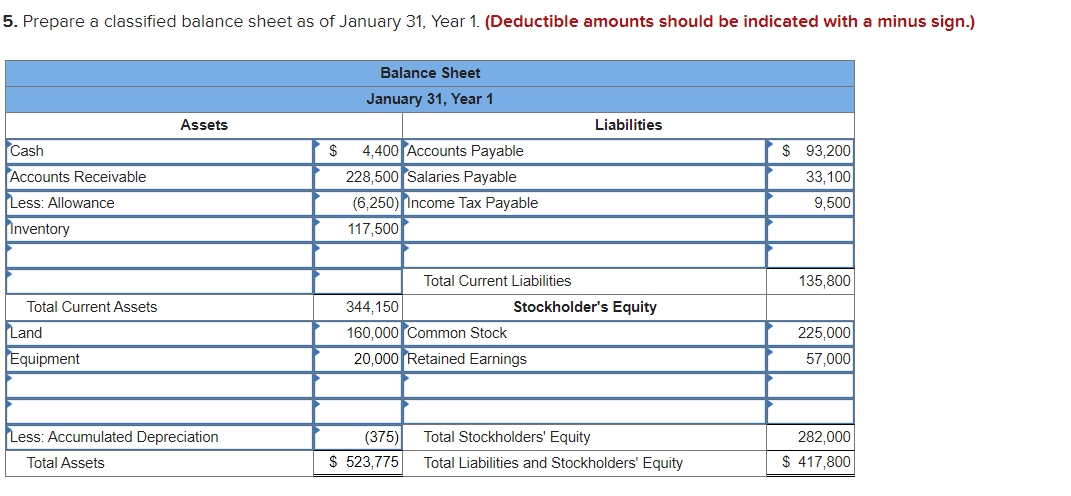

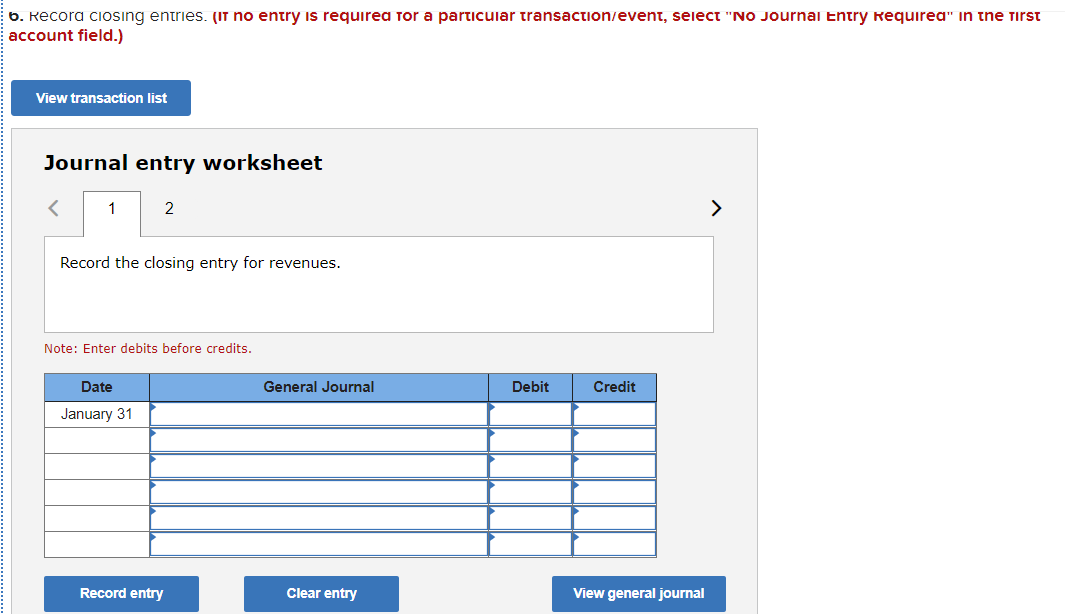

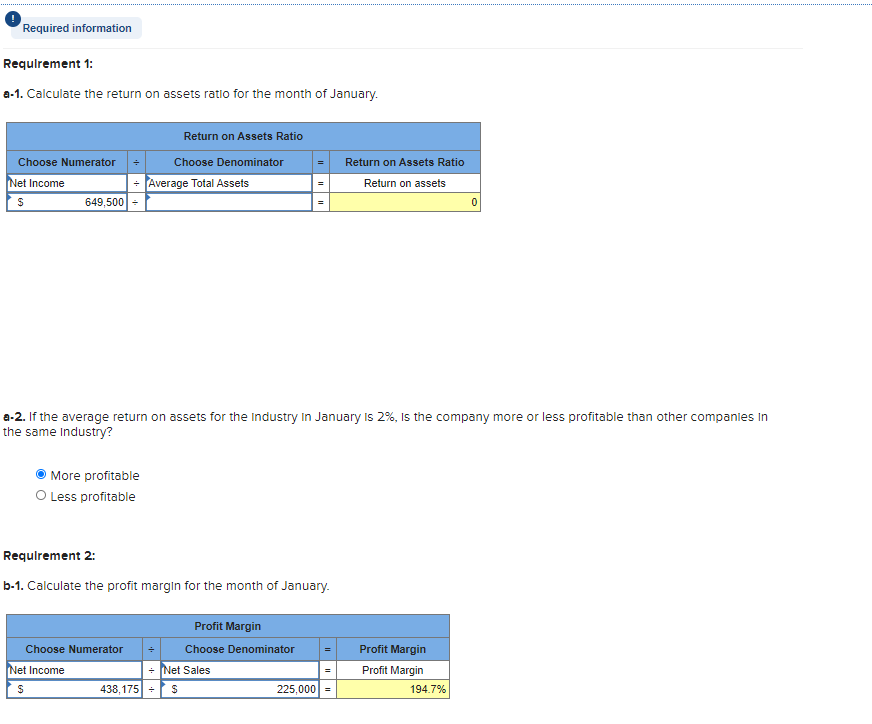

Information for adjusting entries: a. Depreciation on the equipment for the month of January is calculated using the straight-line method. b. The company estimates future uncollectible accounts. The company determines $3,500 of accounts receivable on January 31 are past due, and 50% of these accounts are estimated to be uncollectible. The remaining accounts receivable on January 31 are not past due, and 2% of these accounts are estimated to be uncollectible. (Hint: Use the January 31 accounts receivable balance calculated in the general ledger.) c. Accrued interest revenue on notes receivable for January. d. Unpaid salaries at the end of January are $33,100. e. Accrued income taxes at the end of January are $9,500. On January 1, Year 1, the general ledger of a company includes the following account balances: Credit Debit $ 59,200 26,000 $ 2,700 Accounts Cash Accounts Receivable Allowance for Uncollectible Accounts Inventory Notes Receivable (5%, due in 2 years) Land Accounts Payable Common Stock Retained Earnings Totals 36,800 18,000 160,000 15,300 225,000 57,000 $300,000 $300,000 During January Year 1, the following transactions occur: January 1 Purchase equipment for $20,000. The company estimates a residual value of $2,000 and a four-year service life. January 4 Pay cash on accounts payable, $10,000. January 8 Purchase additional inventory on account, $87,900. January 15 Receive cash on accounts receivable, $22,500. January 19 Pay cash for salaries, $30,300. January 28 Pay cash for January utilities, $17,000. January 30 Sales for January total $225,000. All of these sales are on account. The cost of the units sold is $117,500. Credit Debit $ 4,400 228,500 $ 6,250 7,200 18,000 160,000 93,200 225,000 57,000 Accounts Cash Accounts Receivable Allowance for Uncollectible Accounts Inventory Note Receivable Land Accounts Payable Common Stock Retained Earnings Interest Receivable Equipment Accumulated Depreciation Income Tax Expense Sales Revenue Interest Revenue Cost of Goods Sold Salaries Expense Utilities Expense Depreciation Expense Bad Debt Expense CD 75 20.000 375 9,500 225,000 75 117,500 63,400 17,000 375 3,550 not Totals $ 649,500 $ 606,900 4. Prepare a multiple-step income statement for the period ended January 31, Year 1. Multiple-Step Income Statement For the month ended January 31, Year 1 Sales Revenue Cost of Goods Sold $ 0 Expenses Bad Debt Expense Depreciation Expense Salaries Expense 30,300 30,300 (30,300) Total Operating Expenses Operating Income Interest Expense Income before taxes Income Tax Expense Net Income (30,300) $ (30,300) 5. Prepare a classified balance sheet as of January 31, Year 1. (Deductible amounts should be indicated with a minus sign.) Balance Sheet January 31, Year 1 Assets Liabilities Cash $ Accounts Receivable Less: Allowance 4,400 Accounts Payable 228,500 Salaries Payable (6,250) Income Tax Payable 117,500 $ 93,200 33,100 9,500 Inventory 135,800 Total Current Assets Land Equipment Total Current Liabilities 344,150 Stockholder's Equity 160,000 Common Stock 20,000 Retained Earnings 225,000 57,000 Less: Accumulated Depreciation Total Assets (375) $ 523,775 Total Stockholders' Equity Total Liabilities and Stockholders' Equity 282,000 $ 417,800 6. Recora ciosing entries. (If no entry is required for a particular transaction/event, select "NO Journal Entry Requirea" in the first account field.) View transaction list Journal entry worksheet Record the closing entry for revenues. Note: Enter debits before credits. Date General Journal Debit Credit January 31 Record entry Clear entry View general journal Required information Requirement 1: a-1. Calculate the return on assets ratio for the month of January Choose Numerator Return on Assets Ratio Choose Denominator Average Total Assets Return on Assets Ratio Return on assets Net Income S 649,5001 - 0 a-2. If the average return on assets for the Industry In January is 2%, is the company more or less profitable than other companies in the same Industry? More profitable Less profitable Requirement 2: b-1. Calculate the profit margin for the month of January Profit Margin Choose Numerator Choose Denominator Net Income - Net Sales Profit Margin Profit Margin 194.7% S 438,175] + S 225,000/=