Question

Exercise 9-5 Shown below are the T accounts relating to equipment that was purchased for cash by a company on the first day of the

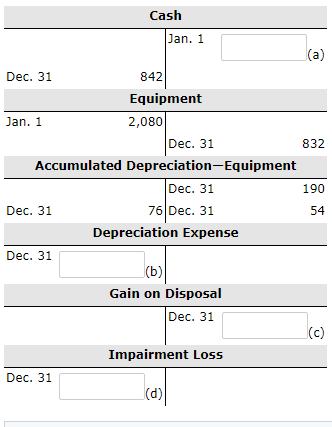

Exercise 9-5

Shown below are the T accounts relating to equipment that was purchased for cash by a company on the first day of the current year. The equipment was depreciated on a straight-line basis with an estimated useful life of 10 years and a residual value of $180. Part of the equipment was sold on the last day of the current year for cash proceeds while the remaining equipment that was not sold became impaired. Reconstruct the journal entries to record the following and derive the missing amounts:

| (a) | Purchase of equipment on January 1. What was the cash paid? | ||

| (b) | Depreciation recorded on December 31. What was the depreciation expense? | ||

| (c) | Sale of part of the equipment on December 31. What was the gain on disposal? | ||

| (d) | Partial impairment loss on the remaining equipment on December 31. What was the impairment loss? |

Cash Jan. 1 ru Dec. 31 842 Equipment Jan. 1 2,080 Dec. 31 832 Accumulated Depreciation-Equipment Dec. 31 190 Dec. 31 76 Dec. 31 54 Depreciation Expense Dec. 31 (b) Gain on Disposal Dec. 31 Impairment Loss Dec. 31 (d)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting An Integrated Statements Approach

Authors: Jonathan E. Duchac, James M. Reeve, Carl S. Warren

2nd Edition

324312113, 978-0324312119