Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Exercise-L.2 - Question 2 Phillip, Samuel and Tracy were in partnership sharing profits and losses in the ratio 3:1:1. The draft statement of financial position

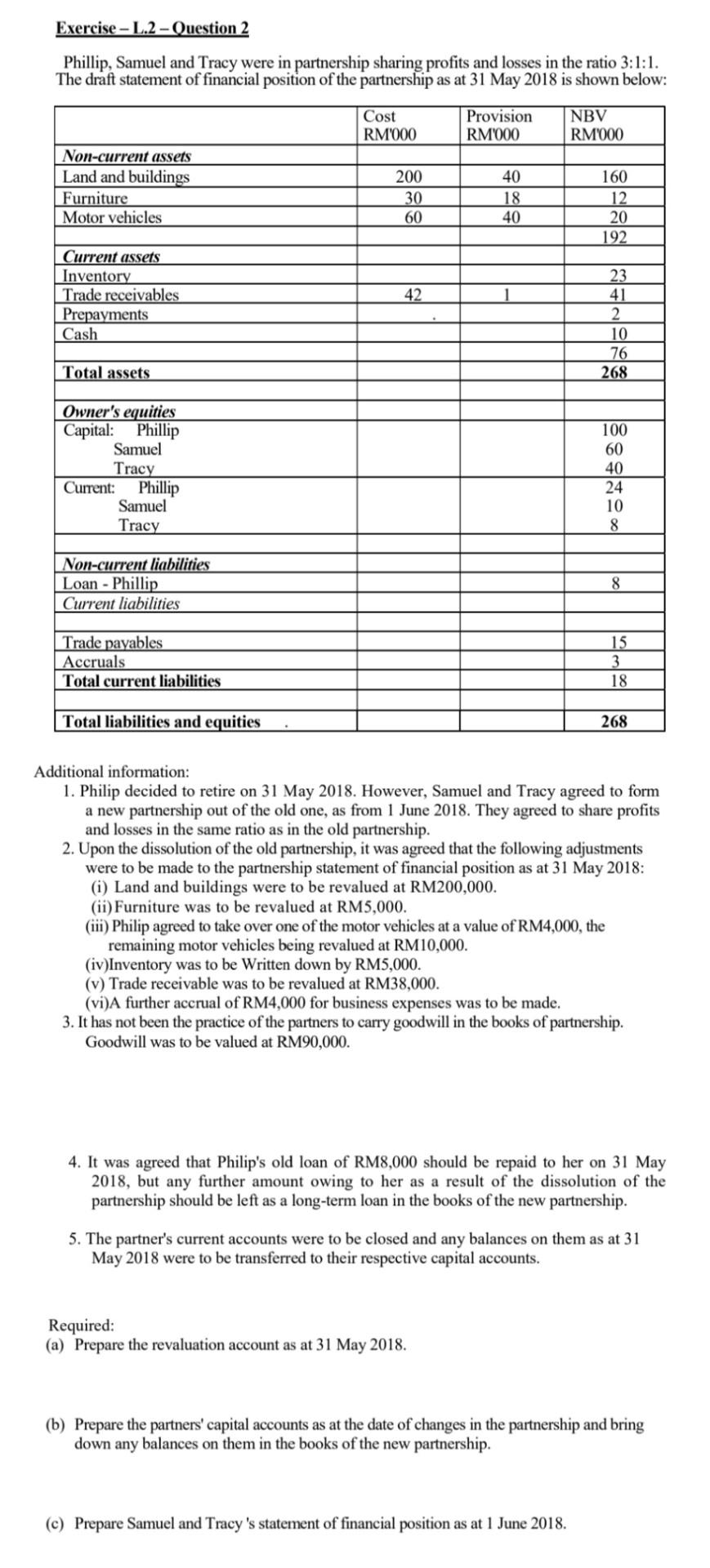

Exercise-L.2 - Question 2 Phillip, Samuel and Tracy were in partnership sharing profits and losses in the ratio 3:1:1. The draft statement of financial position of the partnership as at 31 May 2018 is shown below: Provision NBV Cost RM'000 RM'000 RM000 Non-current assets Land and buildings 40 160 Furniture 18 12 Motor vehicles 40 20 192 Current assets Inventory 23 Trade receivables 41 Prepayments 2 Cash 10 76 Total assets 268 Owner's equities Capital: Phillip 100 Samuel 60 Tracy 40 Current: Phillip 24 Samuel 10 Tracy 8 Non-current liabilities Loan-Phillip 8 Current liabilities Trade payables 15 Accruals 3 Total current liabilities 18 Total liabilities and equities 268 Additional information: 1. Philip decided to retire on 31 May 2018. However, Samuel and Tracy agreed to form a new partnership out of the old one, as from 1 June 2018. They agreed to share profits and losses in the same ratio as in the old partnership. 2. Upon the dissolution of the old partnership, it was agreed that the following adjustments were to be made to the partnership statement of financial position as at 31 May 2018: (i) Land and buildings were to be revalued at RM200,000. (ii) Furniture was to be revalued at RM5,000. (iii) Philip agreed to take over one of the motor vehicles at a value of RM4,000, the remaining motor vehicles being revalued at RM10,000. (iv)Inventory was to be Written down by RM5,000. (v) Trade receivable was to be revalued at RM38,000. (vi)A further accrual of RM4,000 for business expenses was to be made. 3. It has not been the practice of the partners to carry goodwill in the books of partnership. Goodwill was to be valued at RM90,000. 4. It was agreed that Philip's old loan of RM8,000 should be repaid to her on 31 May 2018, but any further amount owing to her as a result of the dissolution of the partnership should be left as a long-term loan in the books of the new partnership. 5. The partner's current accounts were to be closed and any balances on them as at 31 May 2018 were to be transferred to their respective capital accounts. Required: (a) Prepare the revaluation account as at 31 May 2018. (b) Prepare the partners' capital accounts as at the date of changes in the partnership and bring down any balances on them in the books of the new partnership. (c) Prepare Samuel and Tracy's statement of financial position as at 1 June 2018. 200 30 60 42

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Not For Profit Audit Committee Best Practices

Authors: Warren Ruppel

1st Edition

0471697419, 978-0471697411