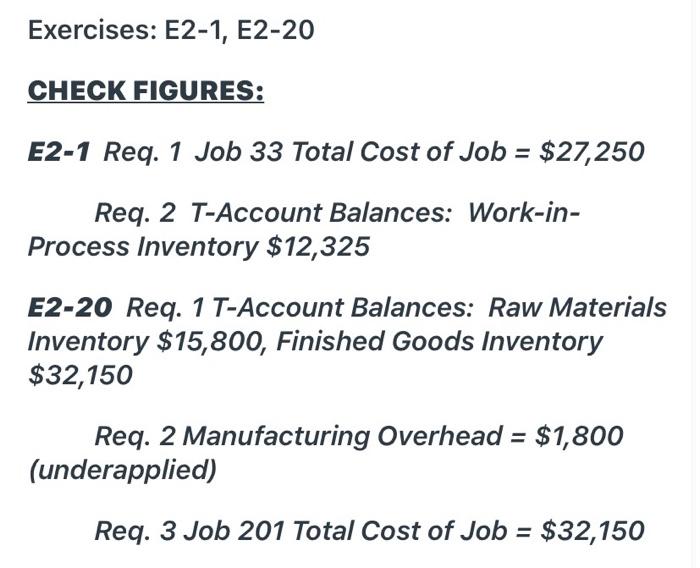

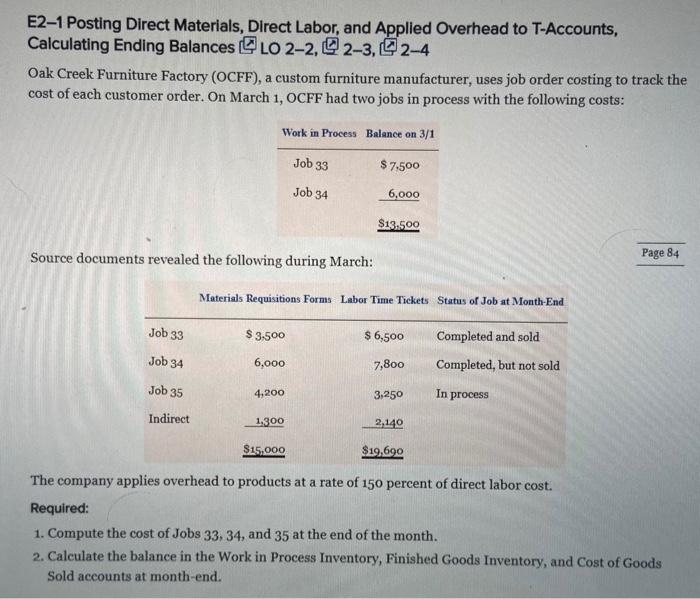

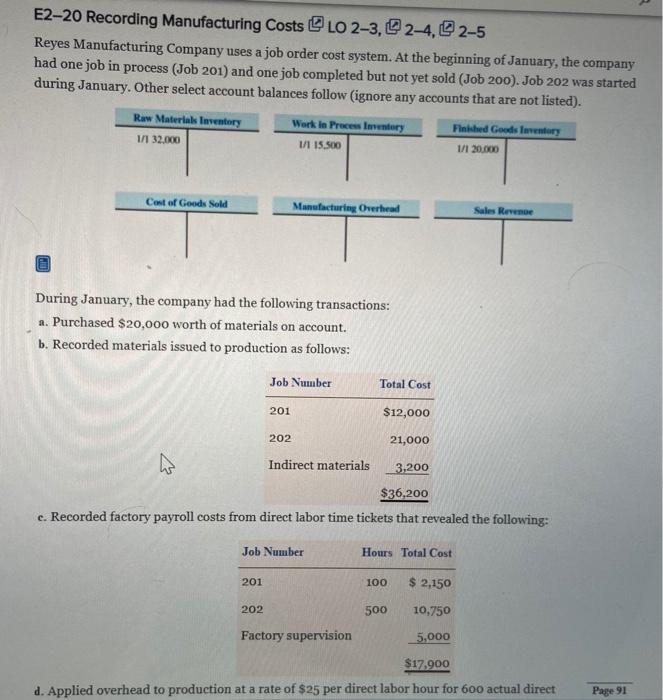

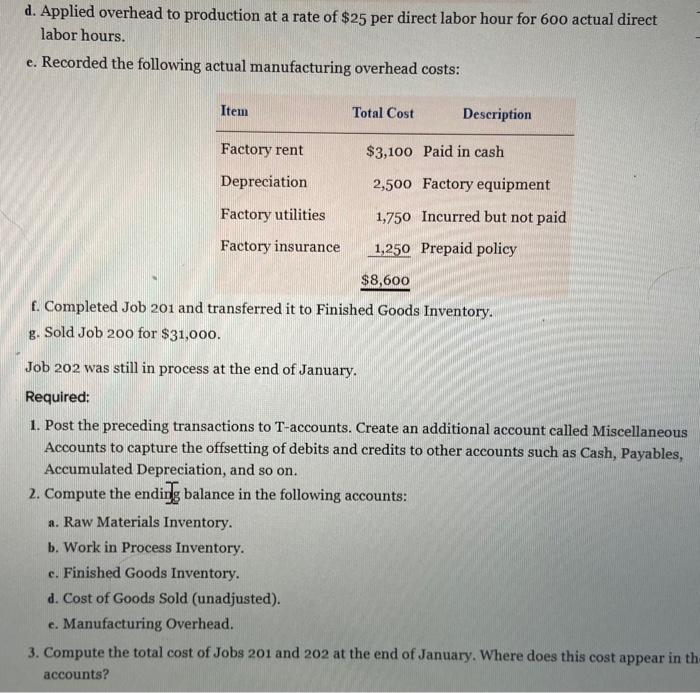

Exercises: E2-1, E2-20 CHECK FIGURES: E2-1 Req. 1 Job 33 Total Cost of Job = $27,250 Req. 2 T-Account Balances: Work-in- Process Inventory $12,325 E2-20 Reg. 1 T-Account Balances: Raw Materials Inventory $15,800, Finished Goods Inventory $32,150 Req. 2 Manufacturing Overhead = $1,800 (underapplied) Req. 3 Job 201 Total Cost of Job = $32,150 E2-1 Posting Direct Materials, Direct Labor, and Applied Overhead to T-Accounts, Calculating Ending Balances LO 2-2,2-3,2-4 Oak Creek Furniture Factory (OCFF), a custom furniture manufacturer, uses job order costing to track the cost of each customer order. On March 1, OCFF had two jobs in process with the following costs: Work in Process Balance on 3/1 Job 33 $7.500 Job 34 6,000 $13.500 Source documents revealed the following during March: Page 84 Materials Requisitions Forms Labor Time Tickets Status of Job at Month-End Job 33 $ 3,500 $ 6,500 Completed and sold Job 34 6,000 7,800 Completed, but not sold Job 35 4,200 3,250 In process Indirect 1.300 2,140 $15.000 $19,690 The company applies overhead to products at a rate of 150 percent of direct labor cost. Required: 1. Compute the cost of Jobs 33, 34, and 35 at the end of the month. 2. Calculate the balance in the Work in Process Inventory, Finished Goods Inventory, and Cost of Goods Sold accounts at month-end. E2-20 Recording Manufacturing Costs LO 2-3, 2-4, 2-5 Reyes Manufacturing Company uses a job order cost system. At the beginning of January, the company had one job in process (Job 201) and one job completed but not yet sold (Job 200). Job 202 was started during January. Other select account balances follow (ignore any accounts that are not listed). Raw Materials Inventory Work in Process Inventory Paked Goods Inventory 1/1 32.000 1/1 15.500 1/1 20.000 Cost of Goods Sold Manufacturing Overhead Sales Revenge During January, the company had the following transactions: a. Purchased $20,000 worth of materials on account. b. Recorded materials issued to production as follows: Job Number Total Cost 201 $12,000 202 21,000 w Indirect materials 3,200 $36,200 c. Recorded factory payroll costs from direct labor time tickets that revealed the following: Job Number Hours Total Cost 201 100 $ 2,150 202 500 10.750 Factory supervision 5,000 $17.900 d. Applied overhead to production at a rate of $25 per direct labor hour for 600 actual direct Page 91 d. Applied overhead to production at a rate of $25 per direct labor hour for 600 actual direct labor hours. e. Recorded the following actual manufacturing overhead costs: Item Total Cost Description Factory rent $3,100 Paid in cash Depreciation 2,500 Factory equipment Factory utilities 1,750 Incurred but not paid Factory insurance 1,250 Prepaid policy $8,600 f. Completed Job 201 and transferred it to Finished Goods Inventory. g. Sold Job 200 for $31,000. Job 202 was still in process at the end of January. Required: 1. Post the preceding transactions to T-accounts. Create an additional account called Miscellaneous Accounts to capture the offsetting of debits and credits to other accounts such as Cash, Payables, Accumulated Depreciation, and so on. 2. Compute the ending balance in the following accounts: a. Raw Materials Inventory. b. Work in Process Inventory. e. Finished Goods Inventory. d. Cost of Goods Sold (unadjusted). e. Manufacturing Overhead. 3. Compute the total cost of Jobs 201 and 202 at the end of January. Where does this cost appear in th accounts