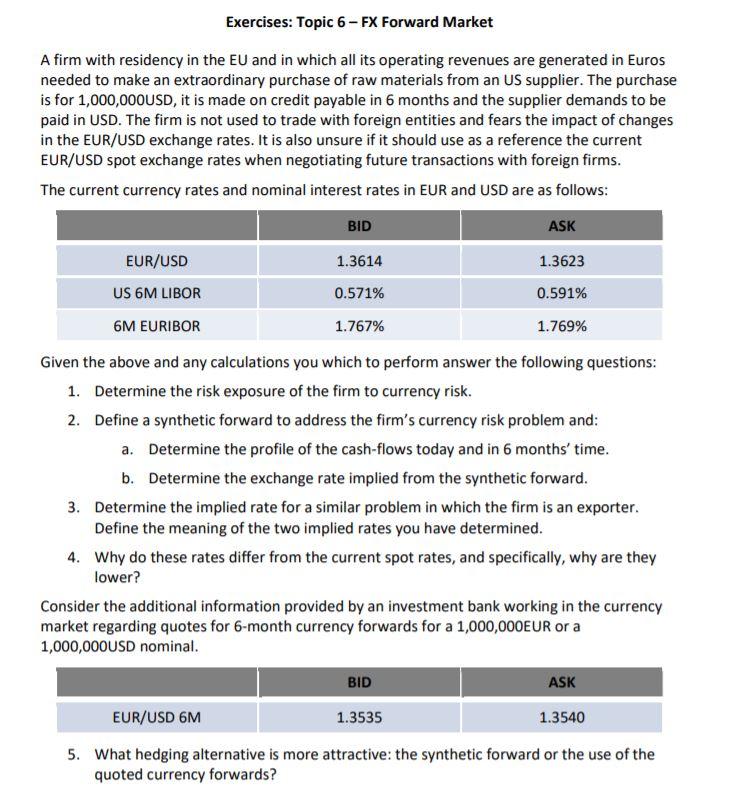

Exercises: Topic 6 - FX Forward Market A firm with residency in the EU and in which all its operating revenues are generated in Euros needed to make an extraordinary purchase of raw materials from an US supplier. The purchase is for 1,000,000USD, it is made on credit payable in 6 months and the supplier demands to be paid in USD. The firm is not used to trade with foreign entities and fears the impact of changes in the EUR/USD exchange rates. It is also unsure if it should use as a reference the current EUR/USD spot exchange rates when negotiating future transactions with foreign firms. The current currency rates and nominal interest rates in EUR and USD are as follows: BID ASK 1.3614 1.3623 EUR/USD US 6M LIBOR 6M EURIBOR 0.571% 0.591% 1.767% 1.769% Given the above and any calculations you which to perform answer the following questions: 1. Determine the risk exposure of the firm to currency risk. 2. Define a synthetic forward to address the firm's currency risk problem and: a. Determine the profile of the cash-flows today and in 6 months' time. b. Determine the exchange rate implied from the synthetic forward. 3. Determine the implied rate for a similar problem in which the firm is an exporter. Define the meaning of the two implied rates you have determined. 4. Why do these rates differ from the current spot rates, and specifically, why are they lower? Consider the additional information provided by an investment bank working in the currency market regarding quotes for 6-month currency forwards for a 1,000,000EUR or a 1,000,000USD nominal. BID ASK EUR/USD 6M 1.3535 1.3540 5. What hedging alternative is more attractive: the synthetic forward or the use of the quoted currency forwards? Exercises: Topic 6 - FX Forward Market A firm with residency in the EU and in which all its operating revenues are generated in Euros needed to make an extraordinary purchase of raw materials from an US supplier. The purchase is for 1,000,000USD, it is made on credit payable in 6 months and the supplier demands to be paid in USD. The firm is not used to trade with foreign entities and fears the impact of changes in the EUR/USD exchange rates. It is also unsure if it should use as a reference the current EUR/USD spot exchange rates when negotiating future transactions with foreign firms. The current currency rates and nominal interest rates in EUR and USD are as follows: BID ASK 1.3614 1.3623 EUR/USD US 6M LIBOR 6M EURIBOR 0.571% 0.591% 1.767% 1.769% Given the above and any calculations you which to perform answer the following questions: 1. Determine the risk exposure of the firm to currency risk. 2. Define a synthetic forward to address the firm's currency risk problem and: a. Determine the profile of the cash-flows today and in 6 months' time. b. Determine the exchange rate implied from the synthetic forward. 3. Determine the implied rate for a similar problem in which the firm is an exporter. Define the meaning of the two implied rates you have determined. 4. Why do these rates differ from the current spot rates, and specifically, why are they lower? Consider the additional information provided by an investment bank working in the currency market regarding quotes for 6-month currency forwards for a 1,000,000EUR or a 1,000,000USD nominal. BID ASK EUR/USD 6M 1.3535 1.3540 5. What hedging alternative is more attractive: the synthetic forward or the use of the quoted currency forwards