Question

Existing Information about Lucy: Lucy (66) is a widow and not currently employed. She has come to you for help designing and implementing a retirement

Existing Information about Lucy:

Lucy (66) is a widow and not currently employed. She has come to you for help designing and implementing a retirement plan. She has $2,000,000 in an inherited spousal IRA; and receives $1,500 monthly from Social Security. Lucy has $100,000 in a money market account at Vanguard, proceeds from the sale of her home. Lucy has one living daughter who is an attorney. Lucy has two grandchildren who are 11 and 13. Lucy would be interested in helping with their education but her daughter does not require any assistance to send the children to college. Lucy and her daughter have not been getting along, the daughter disproves of Lucys new church home.

Lucy estimates she spends between $6,000 and $8,000 a month. About $3,000 are fixed costs including her rent, bills and car payment. Her remaining monthly costs vary and include travel to see kids, doctors visits and giving to her church. She has a IRS back tax bill due of $10,000 from the year her husband died; she is making $500 monthly payments. The bill was incurred when Lucy was grieving and did not remember to file a tax return.

Lucy indicates she would be comfortable taking some risk has self selected as a moderate risk taker, and could lose up to 9% of her portfolio in a year before she would lose sleep. Her mother lived to be 88 and Lucy is in good health; taking only blood pressure medication and vitamins. Lucy is opposed to investing in sin stocks such as gambling or alcohol stocks.

Lucy filled out a reliable and valid risk tolerance questionnaire. She would be most comfortable with a portfolio that contained between 50 and 60% equities; 10 and 20% cash or fixed value equivalents and 40 to 50% bonds. However, she is open to other ideas.

Lucy was told she should be in the S&P 500 by a friend, but she is not familiar with the dynamics of the stock market. She was happy with her performance last year but unhappy that it holds sin stocks.

When asked about her socially conscious investing issues; Lucy affirms that her faith encourages her to not participate in gambling or consuming alcohol and she would like to avoid investing in those types of companies. She is comfortable investing in defense companies, firearm manufactures and international companies. Lucy appears indifferent to earth-friendly or green investing.

Lucy has a daughter, Grace, whom is a successful attorney in Chicago. Lucy would like to leave her church at least $1,000,000 at her death. Lucy would like to begin giving annually to her church at least $20,000 if possible. Lucy understands that her asset balance may shrink during retirement. Lucy is open to helping her grandchildren, but at this time is disappointed with Grace.

She is happy with her Toyota and does not believe she will need another car in the next five years. Lucy is open to paying fees or commissions. Lucy has a FICO score of 750. Lucy is in good health and would qualify as standard for the purposes of purchasing any insurance.

Lucys swank one bedroom apartment is located downtown (Choose any city) and she enjoys the urban elements. She is worried rent will start increasing, as new buildings have gone up in the area. She is open to purchasing a condo but does not want to stress about maintenance. Lucys current apartment is close to her church.

Perform a risk analysis addressing Lucy's top ten risks.

(Include at least one recommendation Lucy can implement and alternative recommendations if appropriate. Consider property, human capital, retirement, longevity, investment and other risks.)

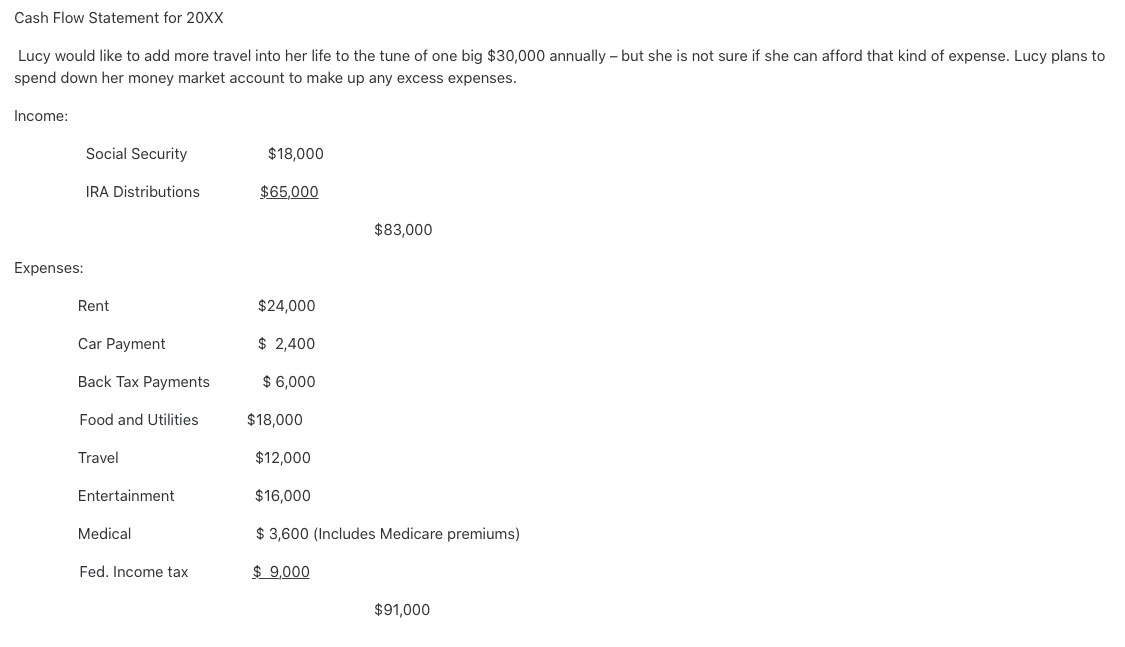

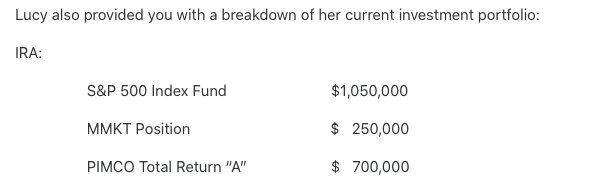

Assets: IRA (rollover from Husband into Lucy's IRA) $2,000,000 MMKT (Vanguard) $ 100,000 Personal Property $ 46,000 2015 Toyota $ 15,000 $2,161,000 Liabilities: Tax Bill - 2014 Return $ 10,000 Credit Card (19% Int) $ 16,000 Car note $ 10,000 $ 36,000 Net Worth: $2,125,000 Cash Flow Statement for 20XX Lucy would like to add more travel into her life to the tune of one big $30,000 annually - but she is not sure if she can afford that kind of expense. Lucy plans to spend down her money market account to make up any excess expenses. Income: Social Security $18,000 IRA Distributions $65,000 $83,000 Expenses: Rent $24,000 Car Payment $ 2,400 Back Tax Payments $ 6,000 Food and Utilities $18,000 Travel $12,000 Entertainment $16,000 Medical $ 3,600 (Includes Medicare premiums) Fed. Income tax $ 9,000 $91,000 Lucy also provided you with a breakdown of her current investment portfolio: IRA: S&P 500 Index Fund $1,050,000 MMKT Position $ 250,000 PIMCO Total Return "A" $ 700,000 Assets: IRA (rollover from Husband into Lucy's IRA) $2,000,000 MMKT (Vanguard) $ 100,000 Personal Property $ 46,000 2015 Toyota $ 15,000 $2,161,000 Liabilities: Tax Bill - 2014 Return $ 10,000 Credit Card (19% Int) $ 16,000 Car note $ 10,000 $ 36,000 Net Worth: $2,125,000 Cash Flow Statement for 20XX Lucy would like to add more travel into her life to the tune of one big $30,000 annually - but she is not sure if she can afford that kind of expense. Lucy plans to spend down her money market account to make up any excess expenses. Income: Social Security $18,000 IRA Distributions $65,000 $83,000 Expenses: Rent $24,000 Car Payment $ 2,400 Back Tax Payments $ 6,000 Food and Utilities $18,000 Travel $12,000 Entertainment $16,000 Medical $ 3,600 (Includes Medicare premiums) Fed. Income tax $ 9,000 $91,000 Lucy also provided you with a breakdown of her current investment portfolio: IRA: S&P 500 Index Fund $1,050,000 MMKT Position $ 250,000 PIMCO Total Return "A" $ 700,000Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Global Business Today

Authors: Charles Hill

7th Edition

0078137217, 9780078137211