Answered step by step

Verified Expert Solution

Question

1 Approved Answer

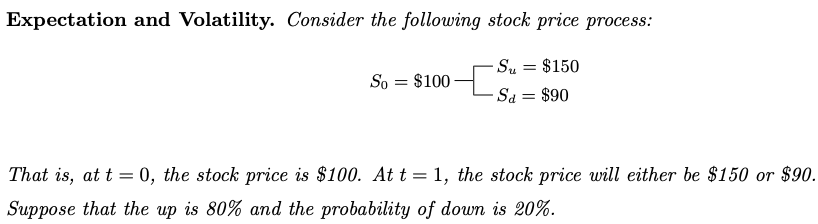

Expectation and Volatility. Consider the following stock price process: So = $100[S Su = $150 Sd = $90 That is, at t = 0, the

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Snap Judgment When To Trust Your Instincts When To Ignore Them And How To Avoid Making Big Mistakes With Your Money

Authors: David E. Adler

1st Edition

0137147783,0137037090