Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Explain each solution concisely. Suppose that you have purchased a 3-year zero-coupon bond with face value of $1000 and a price of $900. Answer the

Explain each solution concisely.

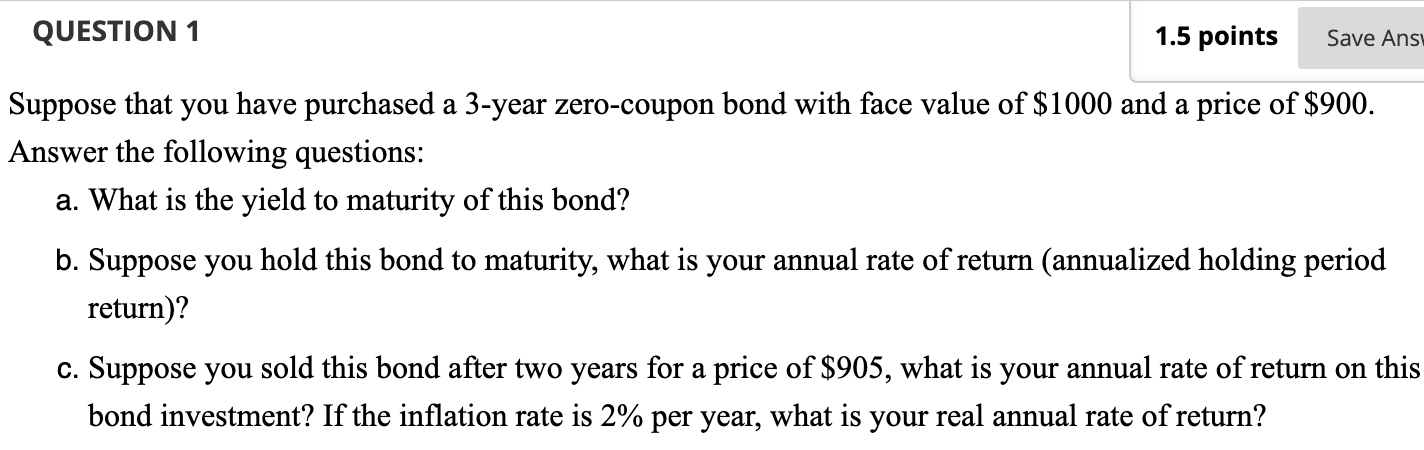

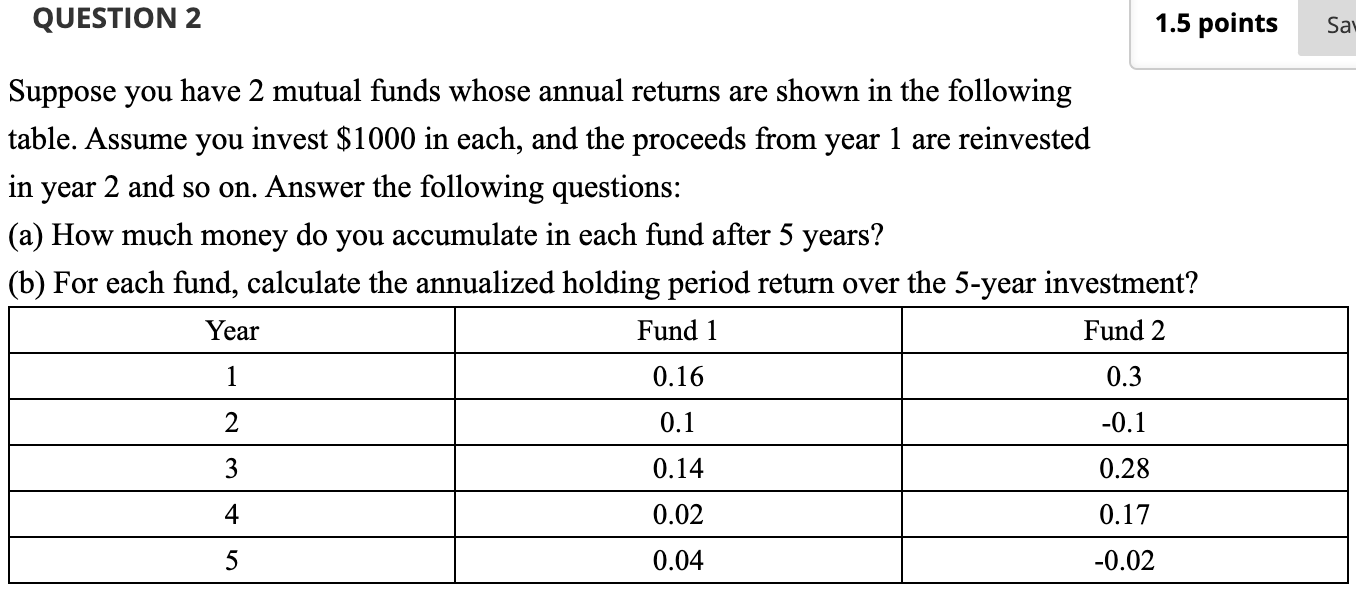

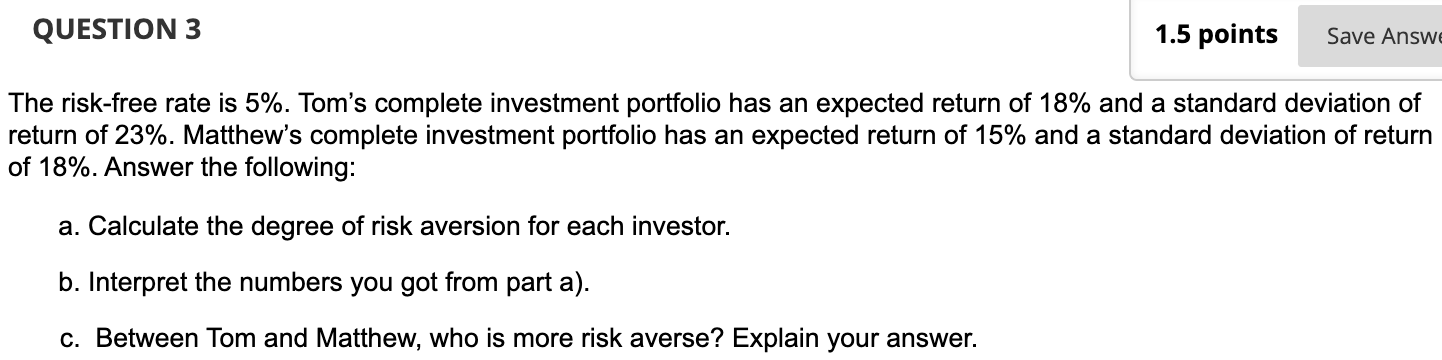

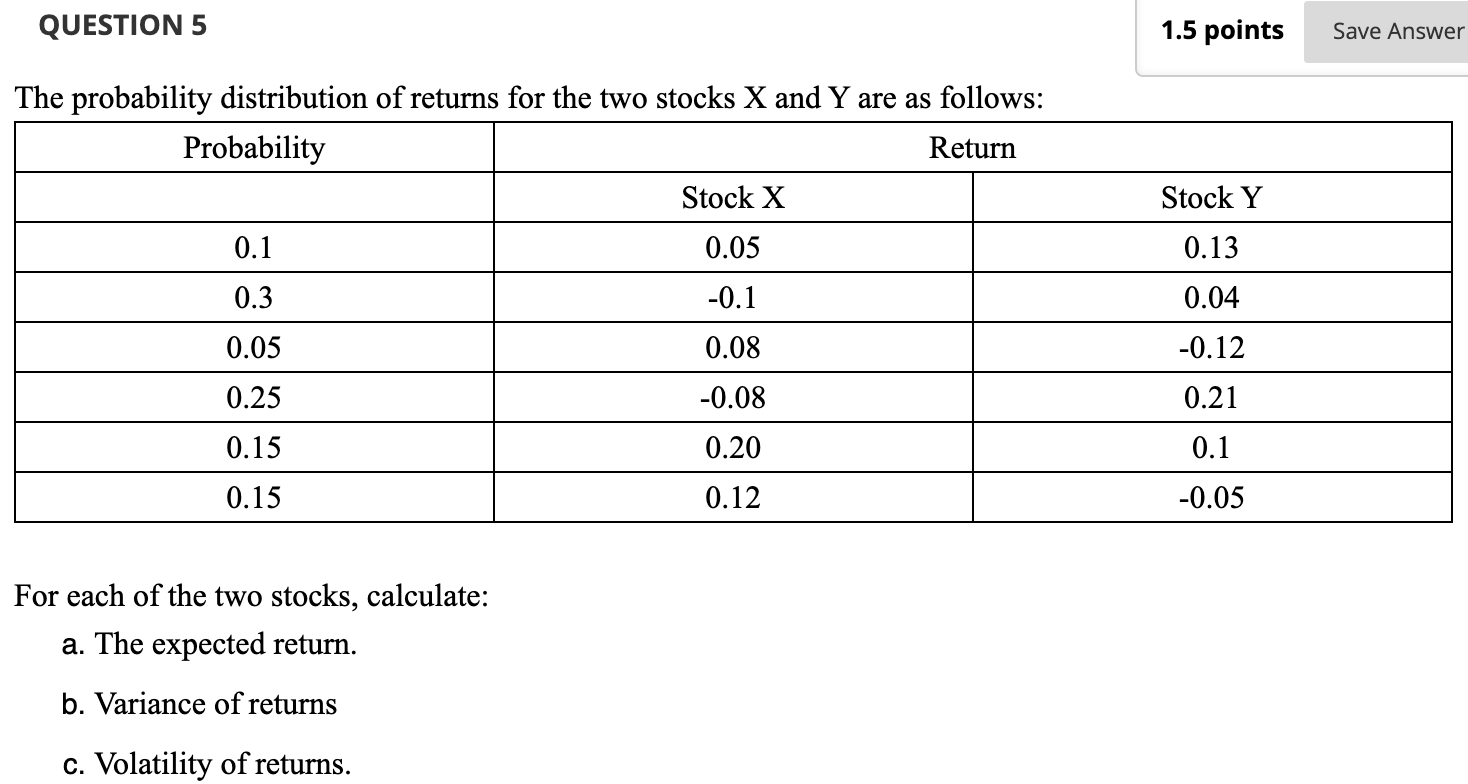

Suppose that you have purchased a 3-year zero-coupon bond with face value of $1000 and a price of $900. Answer the following questions: a. What is the yield to maturity of this bond? b. Suppose you hold this bond to maturity, what is your annual rate of return (annualized holding period return)? c. Suppose you sold this bond after two years for a price of $905, what is your annual rate of return on this bond investment? If the inflation rate is 2% per year, what is your real annual rate of return? The risk-free rate is 5%. Tom's complete investment portfolio has an expected return of 18% and a standard deviation of return of 23%. Matthew's complete investment portfolio has an expected return of 15% and a standard deviation of return of 18%. Answer the following: a. Calculate the degree of risk aversion for each investor. b. Interpret the numbers you got from part a). c. Between Tom and Matthew, who is more risk averse? Explain your answer. Bank A offers credit cards with APR of 15%, compounded monthly. Bank B offers credit cards with APR of 16%, compounded 30 times in a year. You are considering obtaining a credit card from one of these two banks, which bank would you choose? Show all calculations and state the reasoning behind your choice. Suppose you have 2 mutual funds whose annual returns are shown in the following table. Assume you invest $1000 in each, and the proceeds from year 1 are reinvested in year 2 and so on. Answer the following questions: (a) How much money do you accumulate in each fund after 5 years? (b) For each fund, calculate the annualized holding period return over the 5-year invest QUESTION 5 The probability distribution of returns for the two stocks X and Y are as follows: For each of the two stocks, calculate: a. The expected return. b. Variance of returns c. Volatility of returnsStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance For Dummies

Authors: Eric Tyson

9th Edition

1119517893, 978-1119517894