Answered step by step

Verified Expert Solution

Question

1 Approved Answer

a. Explain how a hedge fund manager might appear to be able to beat the market for several years, and yet have no privileged

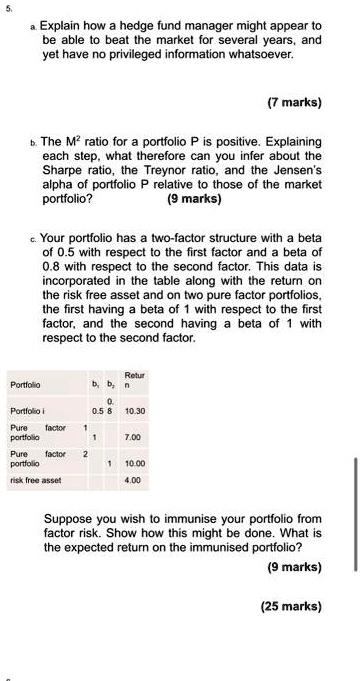

a. Explain how a hedge fund manager might appear to be able to beat the market for several years, and yet have no privileged information whatsoever. b. The M ratio for a portfolio P is positive. Explaining each step, what therefore can you infer about the Sharpe ratio, the Treynor ratio, and the Jensen's alpha of portfolio P relative to those of the market portfolio? (9 marks) c. Your portfolio has a two-factor structure with a beta of 0.5 with respect to the first factor and a beta of 0.8 with respect to the second factor. This data is incorporated in the table along with the return on the risk free asset and on two pure factor portfolios, the first having a beta of 1 with respect to the first factor, and the second having a beta of 1 with respect to the second factor. Portfolio Portfolio Pure factor 1 portfolio Pure factor 2 portfolio risk free asset b, b, 0. 0.5 8 1 Retur n 10.30 (7 marks) 7.00 1 10.00 4.00 Suppose you wish to immunise your portfolio from factor risk. Show how this might be done. What is the expected return on the immunised portfolio? (9 marks) (25 marks)

Step by Step Solution

★★★★★

3.44 Rating (157 Votes )

There are 3 Steps involved in it

Step: 1

Question 1 Explain how a hedge fund manager might appear to be able to beat the market for several years and yet have no privileged information whatsoever A hedge fund manager can seem to outperform t...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Corporate Finance

Authors: Richard Brealey, Stewart Myers, Alan Marcus

8th edition

77861620, 978-0077861629