Answered step by step

Verified Expert Solution

Question

1 Approved Answer

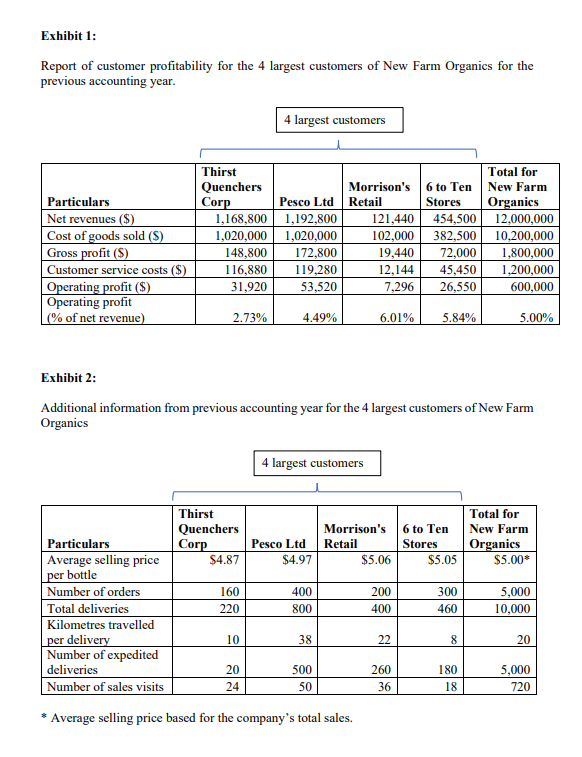

Explain the method used in the case study. Calculate the cost as per activity based costing Company background New Farm Organics Ltd is based in

Explain the method used in the case study. Calculate the cost as per activity based costing

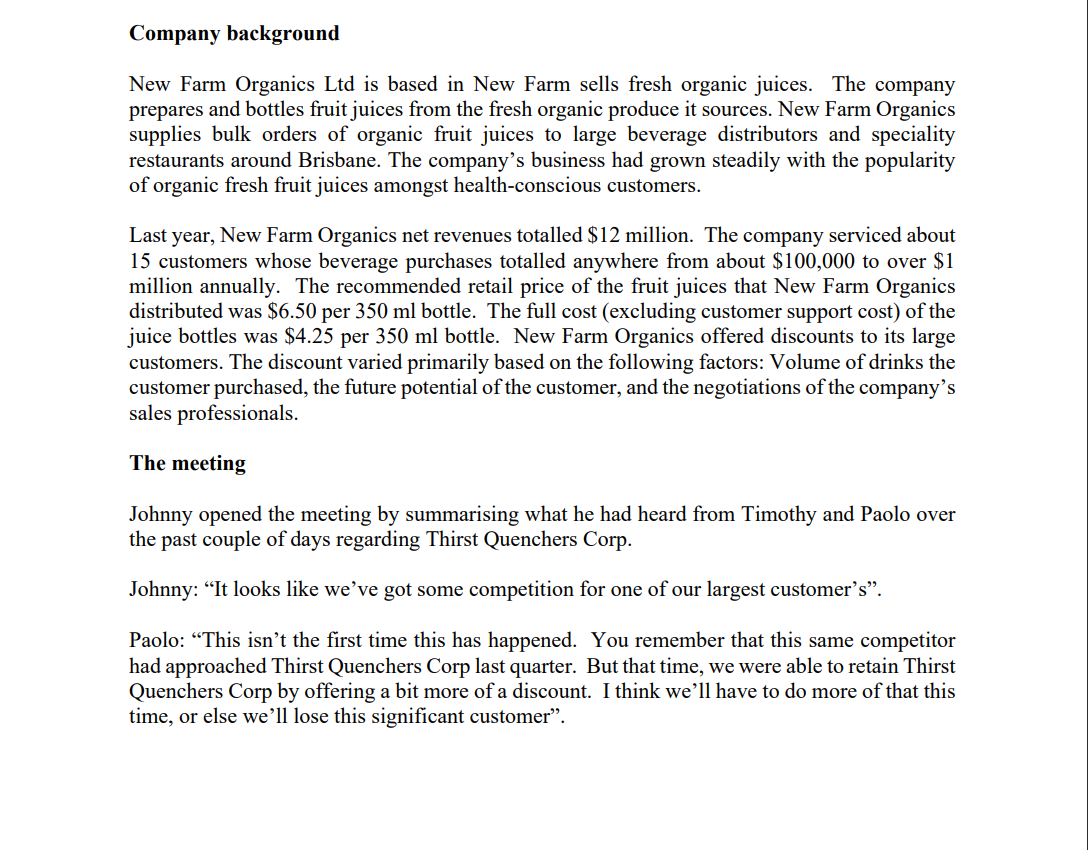

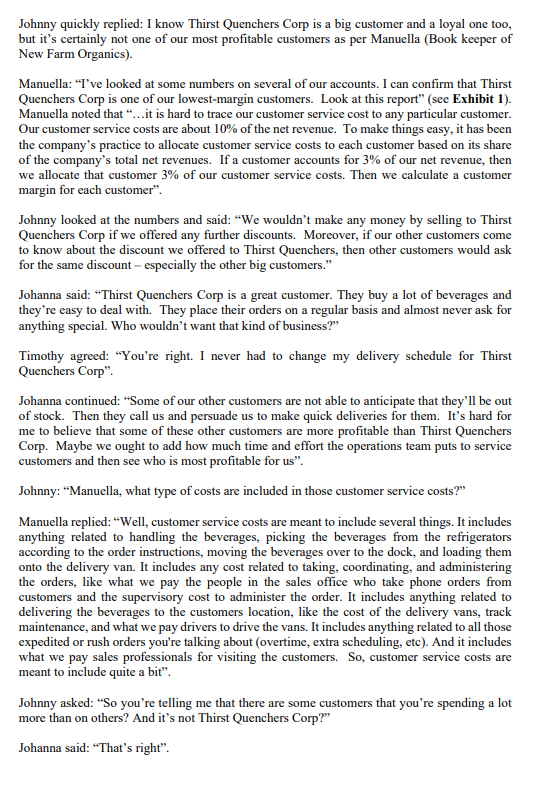

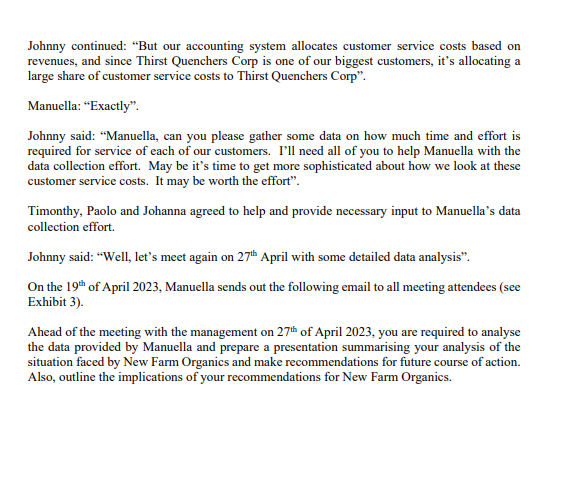

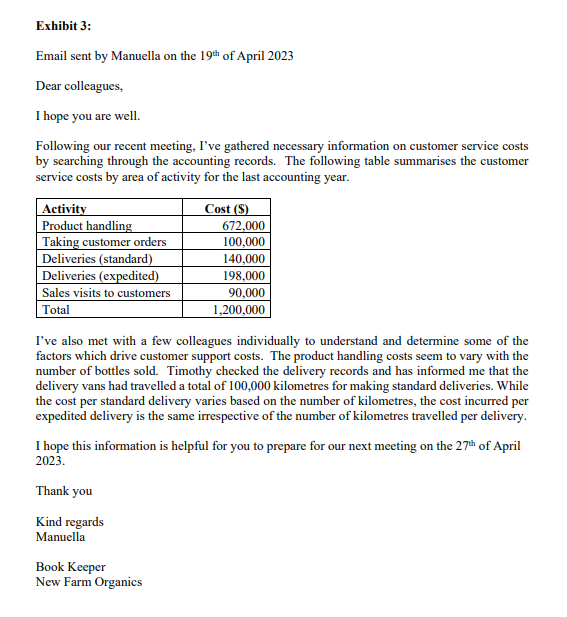

Company background New Farm Organics Ltd is based in New Farm sells fresh organic juices. The company prepares and bottles fruit juices from the fresh organic produce it sources. New Farm Organics supplies bulk orders of organic fruit juices to large beverage distributors and speciality restaurants around Brisbane. The company's business had grown steadily with the popularity of organic fresh fruit juices amongst health-conscious customers. Last year, New Farm Organics net revenues totalled $12 million. The company serviced about 15 customers whose beverage purchases totalled anywhere from about $100,000 to over $1 million annually. The recommended retail price of the fruit juices that New Farm Organics distributed was $6.50 per 350ml bottle. The full cost (excluding customer support cost) of the juice bottles was $4.25 per 350ml bottle. New Farm Organics offered discounts to its large customers. The discount varied primarily based on the following factors: Volume of drinks the customer purchased, the future potential of the customer, and the negotiations of the company's sales professionals. The meeting Johnny opened the meeting by summarising what he had heard from Timothy and Paolo over the past couple of days regarding Thirst Quenchers Corp. Johnny: "It looks like we've got some competition for one of our largest customer's". Paolo: "This isn't the first time this has happened. You remember that this same competitor had approached Thirst Quenchers Corp last quarter. But that time, we were able to retain Thirst Quenchers Corp by offering a bit more of a discount. I think we'll have to do more of that this time, or else we'll lose this significant customer". Johnny quickly replied: I know Thirst Quenchers Corp is a big customer and a loyal one too, but it's certainly not one of our most profitable customers as per Manuella (Book keeper of New Farm Organics). Manuella: "I've looked at some numbers on several of our accounts. I can confirm that Thirst Quenchers Corp is one of our lowest-margin customers. Look at this report" (see Exhibit 1). Manuella noted that "....it is hard to trace our customer service cost to any particular customer. Our customer service costs are about 10% of the net revenue. To make things easy, it has been the company's practice to allocate customer service costs to each customer based on its share of the company's total net revenues. If a customer accounts for 3% of our net revenue, then we allocate that customer 3% of our customer service costs. Then we calculate a customer margin for each customer". Johnny looked at the numbers and said: "We wouldn't make any money by selling to Thirst Quenchers Corp if we offered any further discounts. Moreover, if our other customers come to know about the discount we offered to Thirst Quenchers, then other customers would ask for the same discount - especially the other big customers." Johanna said: "Thirst Quenchers Corp is a great customer. They buy a lot of beverages and they're easy to deal with. They place their orders on a regular basis and almost never ask for anything special. Who wouldn't want that kind of business?" Timothy agreed: "You're right. I never had to change my delivery schedule for Thirst Quenchers Corp". Johanna continued: "Some of our other customers are not able to anticipate that they'll be out of stock. Then they call us and persuade us to make quick deliveries for them. It's hard for me to believe that some of these other customers are more profitable than Thirst Quenchers Corp. Maybe we ought to add how much time and effort the operations team puts to service customers and then see who is most profitable for us". Johnny: "Manuella, what type of costs are included in those customer service costs?" Manuella replied: "Well, customer service costs are meant to include several things. It includes anything related to handling the beverages, picking the beverages from the refrigerators according to the order instructions, moving the beverages over to the dock, and loading them onto the delivery van. It includes any cost related to taking, coordinating, and administering the orders, like what we pay the people in the sales office who take phone orders from customers and the supervisory cost to administer the order. It includes anything related to delivering the beverages to the customers location, like the cost of the delivery vans, track maintenance, and what we pay drivers to drive the vans. It includes anything related to all those expedited or rush orders you're talking about (overtime, extra scheduling, etc). And it includes what we pay sales professionals for visiting the customers. So, customer service costs are meant to include quite a bit". Johnny asked: "So you're telling me that there are some customers that you're spending a lot more than on others? And it's not Thirst Quenchers Corp?' Johanna said: "That's right". Johnny continued: "But our accounting system allocates customer service costs based on revenues, and since Thirst Quenchers Corp is one of our biggest customers, it's allocating a large share of customer service costs to Thirst Quenchers Corp". Manuella: "Exactly". Johnny said: "Manuella, can you please gather some data on how much time and effort is required for service of each of our customers. I'll need all of you to help Manuella with the data collection effort. May be it's time to get more sophisticated about how we look at these customer service costs. It may be worth the effort". Timonthy, Paolo and Johanna agreed to help and provide necessary input to Manuella's data collection effort. Johnny said: "Well, let's meet again on 27th April with some detailed data analysis". On the 19th of April 2023, Manuella sends out the following email to all meeting attendees (see Exhibit 3). Ahead of the meeting with the management on 27th of April 2023, you are required to analyse the data provided by Manuella and prepare a presentation summarising your analysis of the situation faced by New Farm Organics and make recommendations for future course of action. Also, outline the implications of your recommendations for New Farm Organics. Exhibit 3: Email sent by Manuella on the 19th of April 2023 Dear colleagues, I hope you are well. Following our recent meeting, I've gathered necessary information on customer service costs by searching through the accounting records. The following table summarises the customer service costs by area of activity for the last accounting year. I've also met with a few colleagues individually to understand and determine some of the factors which drive customer support costs. The product handling costs seem to vary with the number of bottles sold. Timothy checked the delivery records and has informed me that the delivery vans had travelled a total of 100,000 kilometres for making standard deliveries. While the cost per standard delivery varies based on the number of kilometres, the cost incurred per expedited delivery is the same irrespective of the number of kilometres travelled per delivery. I hope this information is helpful for you to prepare for our next meeting on the 27th of April 2023. Thank you Kind regards Manuella Book Keeper New Farm Organics Report of customer profitability for the 4 largest customers of New Farm Organics for the previous accounting year. Exhibit 2: Additional information from previous accounting year for the 4 largest customers of New Farm Organics 4largestcustomers * Average selling price based for the company's total sales. Company background New Farm Organics Ltd is based in New Farm sells fresh organic juices. The company prepares and bottles fruit juices from the fresh organic produce it sources. New Farm Organics supplies bulk orders of organic fruit juices to large beverage distributors and speciality restaurants around Brisbane. The company's business had grown steadily with the popularity of organic fresh fruit juices amongst health-conscious customers. Last year, New Farm Organics net revenues totalled $12 million. The company serviced about 15 customers whose beverage purchases totalled anywhere from about $100,000 to over $1 million annually. The recommended retail price of the fruit juices that New Farm Organics distributed was $6.50 per 350ml bottle. The full cost (excluding customer support cost) of the juice bottles was $4.25 per 350ml bottle. New Farm Organics offered discounts to its large customers. The discount varied primarily based on the following factors: Volume of drinks the customer purchased, the future potential of the customer, and the negotiations of the company's sales professionals. The meeting Johnny opened the meeting by summarising what he had heard from Timothy and Paolo over the past couple of days regarding Thirst Quenchers Corp. Johnny: "It looks like we've got some competition for one of our largest customer's". Paolo: "This isn't the first time this has happened. You remember that this same competitor had approached Thirst Quenchers Corp last quarter. But that time, we were able to retain Thirst Quenchers Corp by offering a bit more of a discount. I think we'll have to do more of that this time, or else we'll lose this significant customer". Johnny quickly replied: I know Thirst Quenchers Corp is a big customer and a loyal one too, but it's certainly not one of our most profitable customers as per Manuella (Book keeper of New Farm Organics). Manuella: "I've looked at some numbers on several of our accounts. I can confirm that Thirst Quenchers Corp is one of our lowest-margin customers. Look at this report" (see Exhibit 1). Manuella noted that "....it is hard to trace our customer service cost to any particular customer. Our customer service costs are about 10% of the net revenue. To make things easy, it has been the company's practice to allocate customer service costs to each customer based on its share of the company's total net revenues. If a customer accounts for 3% of our net revenue, then we allocate that customer 3% of our customer service costs. Then we calculate a customer margin for each customer". Johnny looked at the numbers and said: "We wouldn't make any money by selling to Thirst Quenchers Corp if we offered any further discounts. Moreover, if our other customers come to know about the discount we offered to Thirst Quenchers, then other customers would ask for the same discount - especially the other big customers." Johanna said: "Thirst Quenchers Corp is a great customer. They buy a lot of beverages and they're easy to deal with. They place their orders on a regular basis and almost never ask for anything special. Who wouldn't want that kind of business?" Timothy agreed: "You're right. I never had to change my delivery schedule for Thirst Quenchers Corp". Johanna continued: "Some of our other customers are not able to anticipate that they'll be out of stock. Then they call us and persuade us to make quick deliveries for them. It's hard for me to believe that some of these other customers are more profitable than Thirst Quenchers Corp. Maybe we ought to add how much time and effort the operations team puts to service customers and then see who is most profitable for us". Johnny: "Manuella, what type of costs are included in those customer service costs?" Manuella replied: "Well, customer service costs are meant to include several things. It includes anything related to handling the beverages, picking the beverages from the refrigerators according to the order instructions, moving the beverages over to the dock, and loading them onto the delivery van. It includes any cost related to taking, coordinating, and administering the orders, like what we pay the people in the sales office who take phone orders from customers and the supervisory cost to administer the order. It includes anything related to delivering the beverages to the customers location, like the cost of the delivery vans, track maintenance, and what we pay drivers to drive the vans. It includes anything related to all those expedited or rush orders you're talking about (overtime, extra scheduling, etc). And it includes what we pay sales professionals for visiting the customers. So, customer service costs are meant to include quite a bit". Johnny asked: "So you're telling me that there are some customers that you're spending a lot more than on others? And it's not Thirst Quenchers Corp?' Johanna said: "That's right". Johnny continued: "But our accounting system allocates customer service costs based on revenues, and since Thirst Quenchers Corp is one of our biggest customers, it's allocating a large share of customer service costs to Thirst Quenchers Corp". Manuella: "Exactly". Johnny said: "Manuella, can you please gather some data on how much time and effort is required for service of each of our customers. I'll need all of you to help Manuella with the data collection effort. May be it's time to get more sophisticated about how we look at these customer service costs. It may be worth the effort". Timonthy, Paolo and Johanna agreed to help and provide necessary input to Manuella's data collection effort. Johnny said: "Well, let's meet again on 27th April with some detailed data analysis". On the 19th of April 2023, Manuella sends out the following email to all meeting attendees (see Exhibit 3). Ahead of the meeting with the management on 27th of April 2023, you are required to analyse the data provided by Manuella and prepare a presentation summarising your analysis of the situation faced by New Farm Organics and make recommendations for future course of action. Also, outline the implications of your recommendations for New Farm Organics. Exhibit 3: Email sent by Manuella on the 19th of April 2023 Dear colleagues, I hope you are well. Following our recent meeting, I've gathered necessary information on customer service costs by searching through the accounting records. The following table summarises the customer service costs by area of activity for the last accounting year. I've also met with a few colleagues individually to understand and determine some of the factors which drive customer support costs. The product handling costs seem to vary with the number of bottles sold. Timothy checked the delivery records and has informed me that the delivery vans had travelled a total of 100,000 kilometres for making standard deliveries. While the cost per standard delivery varies based on the number of kilometres, the cost incurred per expedited delivery is the same irrespective of the number of kilometres travelled per delivery. I hope this information is helpful for you to prepare for our next meeting on the 27th of April 2023. Thank you Kind regards Manuella Book Keeper New Farm Organics Report of customer profitability for the 4 largest customers of New Farm Organics for the previous accounting year. Exhibit 2: Additional information from previous accounting year for the 4 largest customers of New Farm Organics 4largestcustomers * Average selling price based for the company's total salesStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting Principles Volume 2 Chapters 13 To 26

Authors: Jerry J. Weygandt

11th Edition

1118342070, 978-1118342077