Answered step by step

Verified Expert Solution

Question

1 Approved Answer

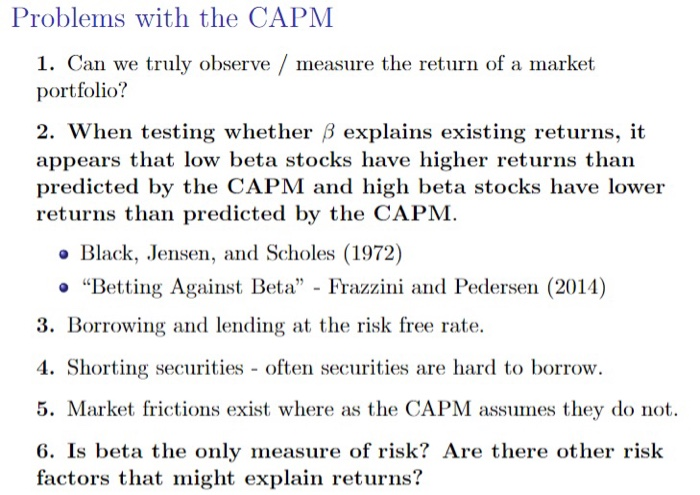

explain these problems Problems with the CAPM 1. Can we truly observe measure the return of a market portfolio? 2. When testing whether explains existing

explain these problems

Problems with the CAPM 1. Can we truly observe measure the return of a market portfolio? 2. When testing whether explains existing returns, it appears that low beta stocks have higher returns than predicted by the CAPM and high beta stocks have lower returns than predicted by the CAPM. o Black, Jensen, and Scholes (1972) o "Betting Against Beta" Frazzini and Pedersen (2014) 3. Borrowing and lending at the risk free rate. 4. Shorting securities often securities are hard to borrow. 5. Market frictions exist where as the CAPM assumes they do not. 6. Is beta the only measure of risk? Are there other risk factors that might explain returns Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance Introduction To Institutions Investments And Management

Authors: Ronald W. Melicher, Edgar A. Norton

11th Edition

0470004460, 978-0470004463