Answered step by step

Verified Expert Solution

Question

1 Approved Answer

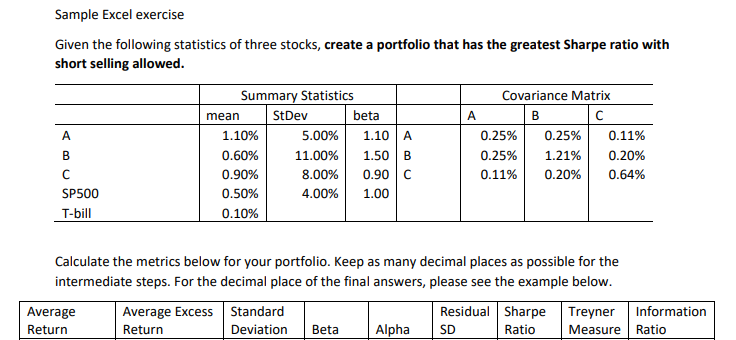

Explanations and steps please Sample Excel exercise Given the following statistics of three stocks, create a portfolio that has the greatest Sharpe ratio with short

Explanations and steps please

Sample Excel exercise Given the following statistics of three stocks, create a portfolio that has the greatest Sharpe ratio with short selling allowed. Covariance Matrix | 1.10A 0.25% 0.25% | Summary Statistics mean StDev beta 1.10% 5.00% 0.60% 11.00% 1.50 0.90% 8.00% 0.90 0.50% 4.00% 1.00 0.10% 0.25% 0.11% 0.20% 0.64% 0.11% 0.20% SP500 T-bill Calculate the metrics below for your portfolio. Keep as many decimal places as possible for the intermediate steps. For the decimal place of the final answers, please see the example below. Average Average Excess Standard Residual Sharpe Treyner Information Return Return Deviation Beta Alpha SD Ratio Measure Ratio Sample Excel exercise Given the following statistics of three stocks, create a portfolio that has the greatest Sharpe ratio with short selling allowed. Covariance Matrix | 1.10A 0.25% 0.25% | Summary Statistics mean StDev beta 1.10% 5.00% 0.60% 11.00% 1.50 0.90% 8.00% 0.90 0.50% 4.00% 1.00 0.10% 0.25% 0.11% 0.20% 0.64% 0.11% 0.20% SP500 T-bill Calculate the metrics below for your portfolio. Keep as many decimal places as possible for the intermediate steps. For the decimal place of the final answers, please see the example below. Average Average Excess Standard Residual Sharpe Treyner Information Return Return Deviation Beta Alpha SD Ratio Measure RatioStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting Tools for business decision making

Authors: Paul D. Kimmel, Jerry J. Weygandt, Donald E. Kieso

6th Edition

978-1119191674, 047053477X, 111919167X, 978-0470534779