Question: Extract the main features in this article and elaborate on the quotation 'Before engaging in a major ABC implementation project, an organisation should consider the

Extract the main features in this article and elaborate on the quotation 'Before engaging in a major ABC implementation project, an organisation should consider the appropriateness of the ABC system.'

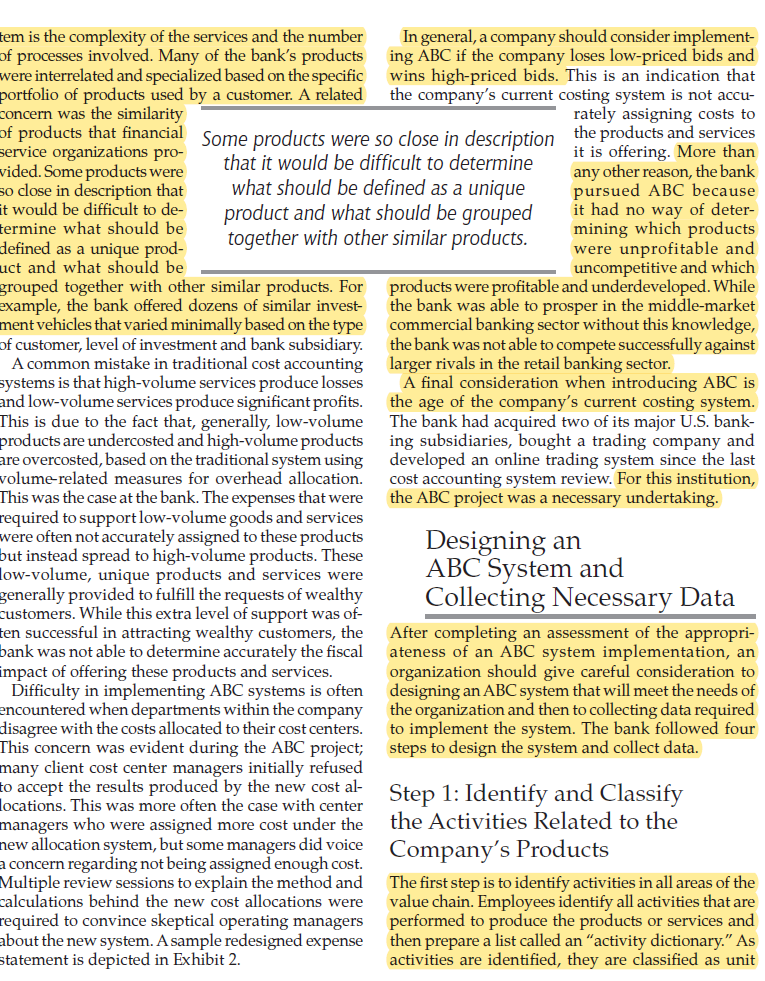

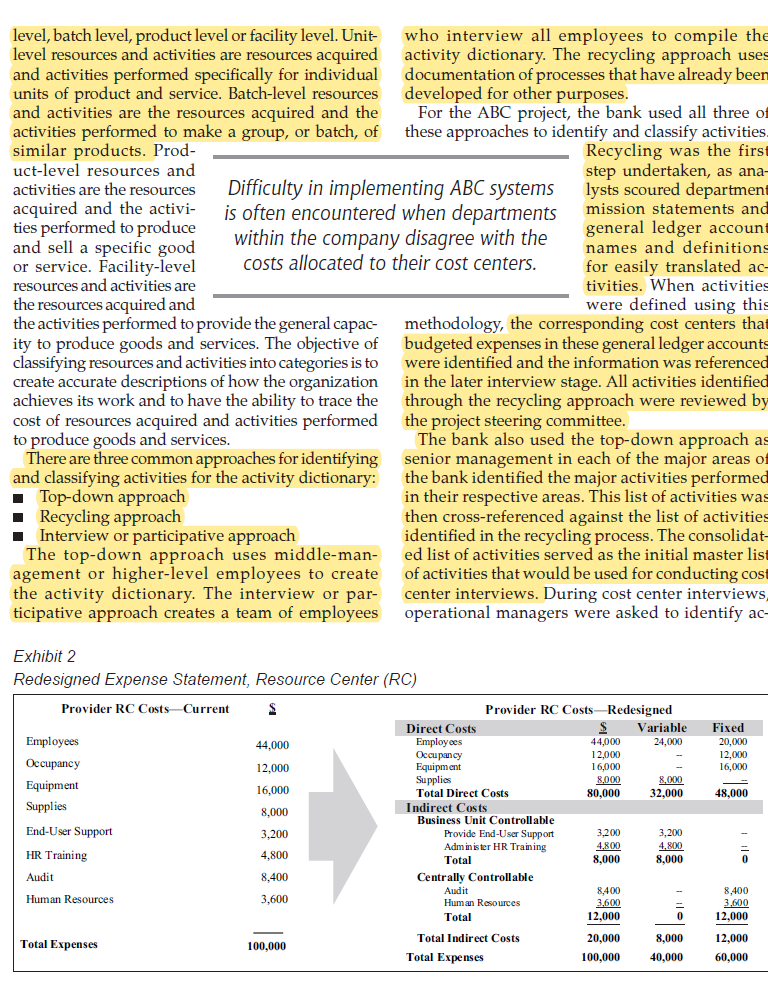

Implementing Activity-Based Costing in the Banking Industry By Jeffrey Witherite and II-woon Kim Benefits include the proper costing of transactions, the ability to trace specific costs to bank customers and the ability to measure customer and product profitability. A ctivity-based costing ("ABC") is widely rec- cost accounting manager thought that an ABC sys- ognized as a superior method for allocating tem would be a viable solution for the bank's product overhead costs. Much emphasis has been profitability concerns. Although the bank was able placed on the implementation of ABC in the manufact to determine how much revenue each of its various turing industry. However, the service industry benefits products and services generated, it was not able to from this system of cost allocation as well, due to the determine with any level of certainty how much it cost fact that service firms usually have high overhead to provide these products and services. At best, senior costs and are labor intensive. These characteristics management was confident that the commercial side of make ABC a logical choice for cost allocation. ABC the bank's business was profitable, while the retail side will help services companies identify and allocate was not as profitable. In addition, bank management overhead costs and quantify labor costs associated was intrigued by the possibility of gaining a better with each activity. For commercial banks, in particular, understanding of the cost associated with the activities the potential benefits of ABC implementation can performed in the bank and the resources dedicated be numerous. These include the proper costing of to performing these activities. Senior management transactions, the ability to trace specific costs to bank thought that there may be some duplication of activi- customers and the ability to measure customer and ties within the organization and that an ABC system product profitability. The end result of these benefits would help identify these areas of duplication. is the ability to improve decision-making and help Six specific benefits were to be realized with the organizations meet their strategic objectives. implementation of ABC (Exhibit 1). Each would A large commercial bank in the United States interact with others to create synergies. recently implemented ABC in four phases over a The first administrative step of the project was to cre- two-year period: preparation and planning; assessing ate a steering committee that would define the planning, appropriateness of ABC; designing an ABC system design and implementation of the system and make im- and collecting necessary data; and implementing the portant decisions at all stages. During the design phase system. This article will discuss the process and ana- of the project, a cost accounting software system was lyze the benefits of and the obstacles to implementing identified through an RFP ("request for proposal") pro- ABC in a financial services environment. cess. After reviewing several ABC applications, software was chosen, primarily because the bank was already Preparation and using this software in its human resources area, and Planning for ABC Jeffrey Witherite is Director of Budgeting at L'Oreal USA, Streetsboro, Ohio. Contact him at jwitherite@us.loreal.com. The bank's cost accounting manager introduced the Il-woon Kim is a Professor of Accounting and International Business at the concept of ABC to senior management because the University of Akron, Akron, Ohio. Contact him at ikimQuakron.edu.the two systems could interface. Recognizing that the cost center interviews, create cost allocations and gain bank lacked the requisite skills to implement the ABC approval for the allocations. Full implementation in sup- system, the steering committee identified a consulting porting centers and cleanup took another six months. firm that could assist in the implementation of the sys- tem, especially with the more technical matters. Assessment of After interviewing representatives from several con- sulting firms, one firm was chosen, primarily because Appropriateness of ABC of its extensive implementation experience. The firm was given a wide-reaching role within the project, Before engaging in a major ABC system implement assisting the steering committee with the design of tation project, an organization should consider the the system to best match the software's functionality, appropriateness of an ABC system. While the ben- designing and preparing the software and processes, efits of ABC system implementation are evident to modifying and loading cost-driver information into most companies, it is important to keep in mind that the new system and assisting in the gathering and many companies have failed to realize all the benefits loading of cost allocations into the system. For cost an ABC system provides. Any company, especially accounting support, the bank decided to use mostly a financial services company, considering an ABC existing internal resources, while hiring some new system implementation should carefully assess the finance employees to assist with the project. While following points, which are identified by many ABC some of the consulting firm's resources were used experts in determining the appropriateness of ABC in a cost accounting capacity, this was intentionally for a particular organization: kept to a minimum in an attempt to control costs and Significant indirect costs avoid potential conflicts of interest. Complex goods and services The new team of analysts was given the responsibility Losses on high-volume products and profits on of introducing the principles of the ABC project to cost low-volume products center managers, conducting cost center interviews and Disagreement by managers over cost allocations creating and recording the new cost allocations. It took Bid results approximately a year and a half to conduct all of the Age of costing system In the case of the bank, Exhibit 1 more than half of the bank's Expected Benefits of ABC Implementation expenses were incurred by support and administrative functions and classified as Compare product Compare Evaluate profitability of Product wholesale lockbox Organizational indirect costs. These func- Assess the cost vs. retail lockbox Performance Performance difference between tions were broken into three item processing in different locations major groups: information technology (IT-providing hardware and software support and application Assess Estimate and development services); ser- Competitiveness Track Costs vice company (providing general support services Evaluate where comptitive Estimate the resources such as check processing, cost advantages may be by Resource Center to meet the wire transfer processing projected demand of ACH transactions and ATM servicing); and the Recover Cost corporate center (providing Determine of Internal services such as finance, hu- Accountability Service Identify the Provided Identify who usad man resources and legal). driver of services and how much they were Another consideration in certain costs charged implementing an ABC sys-tem is the complexity of the services and the number In general, a company should consider implement- of processes involved. Many of the bank's products ing ABC if the company loses low-priced bids and were interrelated and specialized based on the specific wins high-priced bids. This is an indication that portfolio of products used by a customer. A related the company's current costing system is not accu- concern was the similarity rately assigning costs to f products that financial Some products were so close in description the products and services service organizations pro- that it would be difficult to determine it is offering. More than vided. Some products were any other reason, the bank to close in description that what should be defined as a unique pursued ABC because it would be difficult to de- product and what should be grouped it had no way of deter- ermine what should be together with other similar products. mining which products defined as a unique prod- were unprofitable and uct and what should be uncompetitive and which grouped together with other similar products. For products were profitable and underdeveloped. While example, the bank offered dozens of similar invest- the bank was able to prosper in the middle-market ment vehicles that varied minimally based on the type commercial banking sector without this knowledge, f customer, level of investment and bank subsidiary. the bank was not able to compete successfully against A common mistake in traditional cost accounting larger rivals in the retail banking sector. ystems is that high-volume services produce losses A final consideration when introducing ABC is and low-volume services produce significant profits. the age of the company's current costing system. This is due to the fact that, generally, low-volume The bank had acquired two of its major U.S. bank- products are undercosted and high-volume products ing subsidiaries, bought a trading company and are overcosted, based on the traditional system using developed an online trading system since the last volume-related measures for overhead allocation. cost accounting system review. For this institution, This was the case at the bank. The expenses that were the ABC project was a necessary undertaking. equired to support low-volume goods and services were often not accurately assigned to these products but instead spread to high-volume products. These Designing an ow-volume, unique products and services were ABC System and generally provided to fulfill the requests of wealthy Collecting Necessary Data customers. While this extra level of support was of- en successful in attracting wealthy customers, the After completing an assessment of the appropri- bank was not able to determine accurately the fiscal ateness of an ABC system implementation, an mpact of offering these products and services. organization should give careful consideration to Difficulty in implementing ABC systems is often designing an ABC system that will meet the needs of encountered when departments within the company the organization and then to collecting data required disagree with the costs allocated to their cost centers. to implement the system. The bank followed four This concern was evident during the ABC project; steps to design the system and collect data. many client cost center managers initially refused o accept the results produced by the new cost al- ocations. This was more often the case with center Step 1: Identify and Classify managers who were assigned more cost under the the Activities Related to the new allocation system, but some managers did voice a concern regarding not being assigned enough cost. Company's Products Multiple review sessions to explain the method and The first step is to identify activities in all areas of the calculations behind the new cost allocations were value chain. Employees identify all activities that are required to convince skeptical operating managers performed to produce the products or services and about the new system. A sample redesigned expense then prepare a list called an "activity dictionary." As statement is depicted in Exhibit 2. activities are identified, they are classified as unitlevel, batch level, product level or facility level. Unit- who interview all employees to compile the level resources and activities are resources acquired activity dictionary. The recycling approach use and activities performed specifically for individual documentation of processes that have already beer units of product and service. Batch-level resources developed for other purposes. and activities are the resources acquired and the For the ABC project, the bank used all three of activities performed to make a group, or batch, of these approaches to identify and classify activities similar products. Prod- Recycling was the firs uct-level resources and step undertaken, as ana- activities are the resources Difficulty in implementing ABC systems lysts scoured department acquired and the activi- is often encountered when departments mission statements and ties performed to produce within the company disagree with the general ledger accoun and sell a specific good names and definition or service. Facility-level costs allocated to their cost centers. for easily translated ac resources and activities are tivities. When activities the resources acquired and were defined using this the activities performed to provide the general capac- methodology, the corresponding cost centers tha ity to produce goods and services. The objective of budgeted expenses in these general ledger accounts classifying resources and activities into categories is to were identified and the information was referenced create accurate descriptions of how the organization in the later interview stage. All activities identified achieves its work and to have the ability to trace the through the recycling approach were reviewed by cost of resources acquired and activities performed the project steering committee. to produce goods and services. The bank also used the top-down approach a There are three common approaches for identifying senior management in each of the major areas of and classifying activities for the activity dictionary: the bank identified the major activities performed Top-down approach in their respective areas. This list of activities was Recycling approach then cross-referenced against the list of activities Interview or participative approach identified in the recycling process. The consolidat- The top-down approach uses middle-man- ed list of activities served as the initial master list agement or higher-level employees to create of activities that would be used for conducting cost the activity dictionary. The interview or par- center interviews. During cost center interviews ticipative approach creates a team of employees operational managers were asked to identify ac- Exhibit 2 Redesigned Expense Statement, Resource Center (RC) Provider RC Costs-Current S Provider RC Costs-Redesigned Direct Costs Variable Fixed Employees 44,000 Employ ccs 44,00 24,000 20,00 Occupancy 12,000 12.000 Occupancy 12,000 Equipment 16,000 16,000 Equipment Supplies 8.000 8.000 16,000 Total Direct Costs 80,000 32,000 48,000 Supplies 8.000 Indirect Costs Business Unit Controllable End-User Support 3,200 Provide End-User Support 3,200 3,200 Administer HR Training 4,800 4.800 HR Training 4.800 Total 8.000 8.000 Audit 8.400 Centrally Controllable Audit 8,400 8,400 Human Resources 3,600 Human Resources 3.600 3.600 Total 12,000 12.000 Total Expenses Total Indirect Costs 20,000 8.000 12,000 100,000 Total Expenses 100,000 40,000 60,000tivities performed in their centers that were not on the master activity list. The newly identied activities were reviewed by the steering committee and, if approved, added to the master activity list. The main activity distinction used in the project was to dene activities as those that assigned costs directly to bank products and services or those that assigned costs to other cost centers. Step 2: Estimate the Cost of Activities Identied in Step 1 Once activities have been identified, it is necessary to estimate the costs associated with specic activities. These costs include both human resources, such as employee labor for maintenance and production, and physical resources, such as the cost of equipment and buildings The total cost of each activity mustbe calcu lated using employee data from personnel interviews and nancial data from the accounting department. Employees are asked to identify the amount of time they spend on each activity in an average week and then identify the physical resources that were used to support the activity. This information is compiled on an employee activity data sheet. Aspart of the project, analysts conducted activity interviews with cost center managers using detaed budget and actual expense information. This infor mation was used as a reference for assigning costs to activities. Once the relationship between specic expenses and related activities was defined, aggre gate costs were assigned to each activity. Step 3: Calculate a Cost-Driver Rate for Each Activity As soon as the activity cost data from step two is identied, it can be used to calculate costdriver rates the company should use for assigning activity costs to goods and services. Acostdriver rate is the estimated cost of resource consumption per unit of the cost driver for each activity. This rate should use a base that has some causal link to the cost. In order to calculate an accurate costdriver rate, it is neces sary to know the total activity cost and the activity volume. The infom'tation from step two can provide the total activity cost. The activity volume is the total volume of the cost drivers defined in step one for this particular activity. Once the activity cost and activity volume figures are determined, the costdriver rates are calculated by dividing the total activity cost by the total activity volume. The calculation of costdriver rates was made much easier by the extensive amount of historical budget, head count, occupancy and transactional cost infor mation maintained by the company. This infom'tation was easy loaded into the database and referenced in the creation of cost allocations. Step 4: Assign Activity Costs to Products In the nal step, the costdriver rates prepared in step three were used to assign activity costs to goods and services at the bank. There are three key points for assigning activity costs to products and services. First, all the activities related to a given product or service must be identied. Tt'fithout an intimate un derstanding of a company's organizational structure and the relationships between departments, it may be difficult to identify accurately all the activities related to a product or service. Second, the number of units of each activity that are used per unit of product should be determined. It is easier to dene the units of consumption for activities that easily relate to products on a unitary level. For activities that are more unclear or uncertain, dening con sumption may not be as easy. Third, costs should be assigned to products using the costdriver rates for each activity. ABC Implementation and Challenges ThebigratchallengetoimplementingABCatthebank was generating sufficientbuyin from operational man agers. The major concern expressedbybank managers was whether the benets of the new costing system would justify the time and resources dedicated to implementing the system. Afew managers expressed concern that the new cost accounting system was merely going to reshufe the bank's costs and that, unless hard actions were taken to remove costs from the bank, the project would serve no useful purpose. Another concern encountered was that the proj- performed again. While it was difficult to gain ap ect was initially viewed as another program in a proval for cost center allocations from the servic long line of special initiatives and cost-savings providers, it proved even more difficult to ge programs that resulted in uncertain benefits. The approval for the allocations from the client cente bank had recently completed a major restructur managers. This challenge was especially eviden ing initiative. While this initiative redefined the for centers whose assigned costs from a suppor support areas of the or- center increased as a re ganization and resulted The most difficult part of the project was sult of the change in cos in workforce reductions, allocation methodology it was uncertain whether gaining approval for the cost information After gaining approv this program actually re- produced by the new allocations. al from the operating sulted in cost savings. managers with specifi During the cost center product profitability re interview process, another concern encountered sponsibilities, the approval process then required was duplication of effort in collecting informa- approval from the project steering committee an tion. Duplication of effort was most evident when executive-level management. project analysts asked operating managers for cost accounting information that was collected recently The Key to ABC Success as part of prior cost collection activities. In addi- tion, duplication of effort was evident between the The key to successful implementation of ABC is a project and the recently completed organizational organization's employees. It starts with the AB restructuring. If the steering committee had known champion. For this commercial bank, the ABC earlier that much of the same information was col- champion was the cost accounting manager. A lected as part of the restructuring, time could have for all project champions, this role was to convinc been saved and aggravation avoided. management of the viability and necessity of th A further concern was the occasional lack of project and to create enthusiasm that extended to creativity on the part of the center managers. employees throughout the organization. For severa Managers were often inclined to estimates instead reasons, the major factor in the success of an AB of taking time to identify an appropriate cost implementation is gaining the support and coop driver to charge dollars based on actual usage. eration of the organization's employees. First, the Further, when a suitable cost driver was defined, more employees understand and support the ABC t was often difficult to collect the driver infor- initiative, the greater the chance the ABC system mation necessary to support the cost driver. If it will be successful. In this regard, honest and ope became evident that the driver information was communication was effectively carried out not only not available, a new driver would be selected or by the steering committee but also by top manage possibly a new activity or set of activities would ment. Second, the employees should be allowed to be used as a replacement. To support the entry participate fully in the ABC development process and coordination of cost-driver information into facilitate their commitment to the new system. A he system, three analysts focused their attention mentioned above, the process for acquiring activity on data management, with no cost center inter- and cost information included the participation view responsibilities. the employees. Through the use of the interview After all the cost center allocations were created approach, employee involvement became impera and entered into the systems, the most difficult tive to the process. Third, any major changes in th part of the project was gaining approval for the organizational structure will generate employe cost information produced by the new alloca- resistance. Clearly, this was the case for the project ions. From a service provider standpoint, many Communication was integral to the process as th managers were dissatisfied with the result of the committees charged with implementing the ABC allocations and requested that the cost center system made the effort to fully explain the proces interview process for their respective center be and the benefits to the employees

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!