Answered step by step

Verified Expert Solution

Question

1 Approved Answer

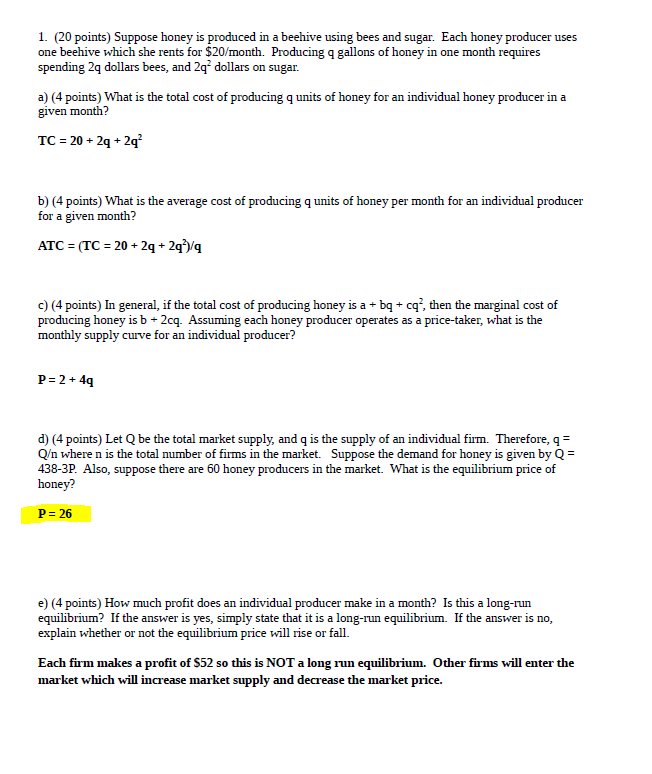

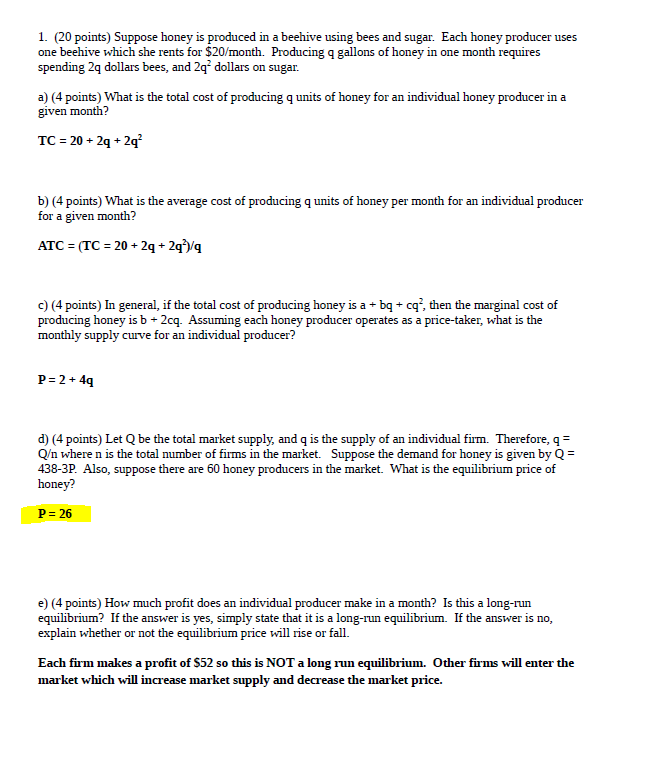

1_ (20 points) Suppose honey is produced in a beehive using bees and sugar Each honey producer uses one beehive which she rents for

1_ (20 points) Suppose honey is produced in a beehive using bees and sugar Each honey producer uses one beehive which she rents for S20/month. Producing q gallons of honey in one month requires spending 2q dollars bees, and 2q2 dollars on sugar. a) (4 points) What is the total cost of producing q units of honey for an individual honey producer in a gieen month? TC=20+2q+2q2 b) (4 points) What is the average cost of producing q units of honey per month for an individual producer for a given month? c) (4 points) In general, if the total cost of producing honey is a + bq + cq2, ffen the marginal cost of producing honey is b * 2cq_ Assuming each honey producer operates as a price-taker, what is the monthly supply cuve for an individual producer? P=2+4q d) (4 points) Let Q be the total market supply, and q is the supply of an individual firrm Therefore, q Qn where n is the total number of films In the market. Suppose the demand for honey given by Q 438-32 Also, suppose there are 60 honey producers in the market. WQat is the equilibrium puce of honey? e) (4 points) How much profit does an individual producer make in a month? Is this a long-run equilibrium? If the answer is yes, simply state that it is a long-run equilibrium. If the answer is no, explain whether or not the equilibrium puce will rise or fall _ Each firm makes a profit of S52 so this is NOT a long run equilibrium. Other firnE will enter the market which will increase market supply and decrease the market price.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Economics

Authors: John Sloman, Jon Guest, Dean Garratt

10th edition

1292187859, 9781292187907 , 978-1292187853