Answered step by step

Verified Expert Solution

Question

1 Approved Answer

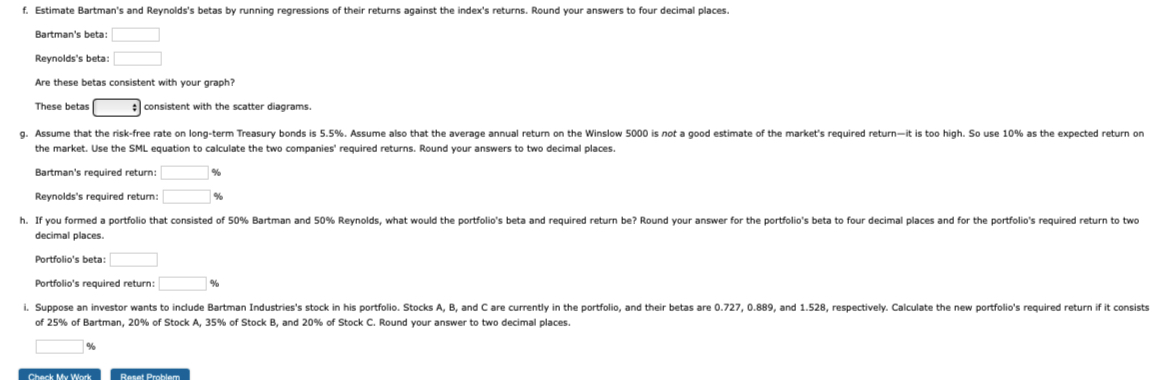

f . Estimate Bartman's and Reynolds's betas by running regressions of their returns against the index's returns. Round your answers to four decimal places. Bartman's

f Estimate Bartman's and Reynolds's betas by running regressions of their returns against the index's returns. Round your answers to four decimal places.

Bartman's beta:

Reynolds's beta:

Are these betas consistent with your graph?

These betas consistent with the scatter diagrams.

the market. Use the SML equation to calculate the two companies' required returns. Round your answers to two decimal places.

Bartman's required return:

Reynolds's required return:

decimal places.

Portfolio's beta:

Portfolio's required return:

of of Bartman, of Stock A of Stock B and of Stock C Round your answer to two decimal places.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Big Tech In Finance

Authors: Igor Pejic

1st Edition

139860898X, 978-1398608986