Answered step by step

Verified Expert Solution

Question

1 Approved Answer

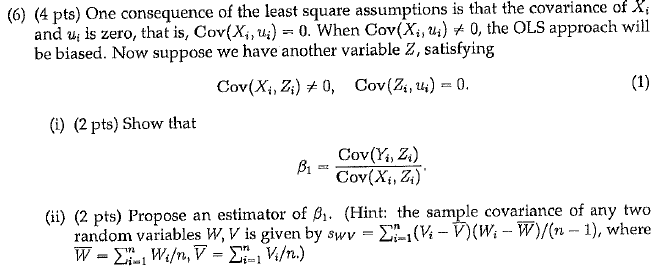

f(6) (4 pts) One consequence of the least square assumptions is that the covariance of X; and u is zero, that is, Cov( X,, w;)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Trigonometry

Authors: Ron Larson, Rosemarie Menager Beeley, Larson/Hostetler

8th Edition

1111789177, 9781111789176