Answered step by step

Verified Expert Solution

Question

1 Approved Answer

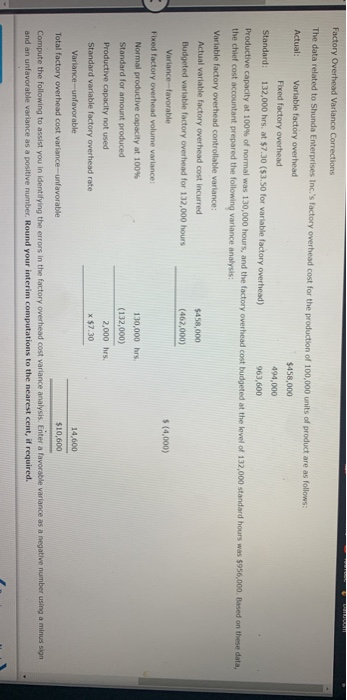

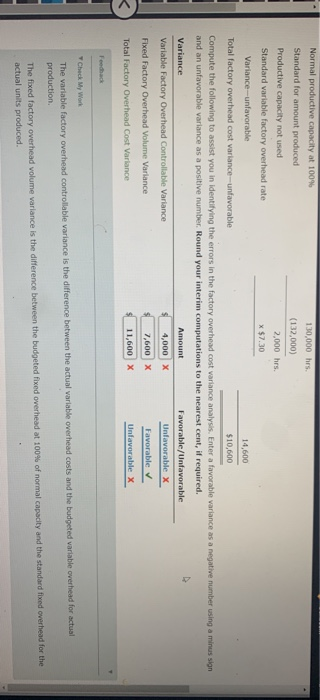

Factory Overhead Variance Corrections The data related to Shunda Enterprises Inc.'s factory overhead cost for the production of 100,000 units of product are as follows:

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing Business Continuity Plans Assess And Improve Your Performance Against ISO 22301

Authors: John Silltow

2nd Edition

058074342X, 978-0580743429