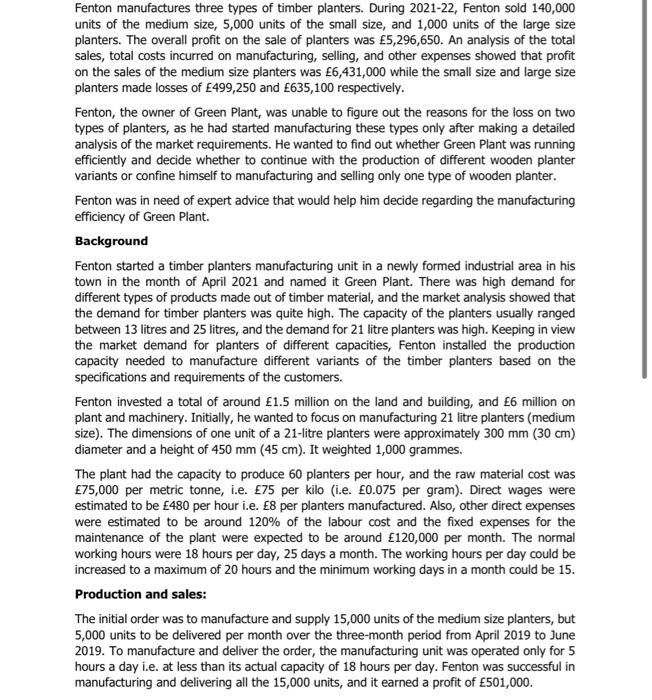

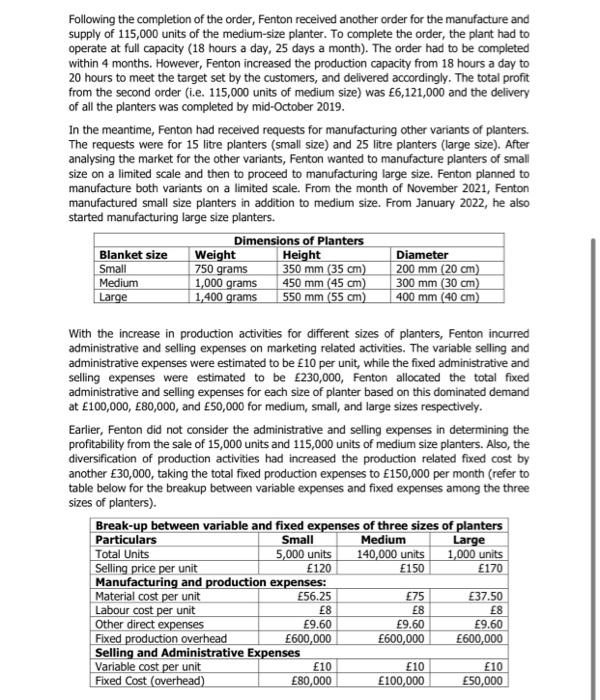

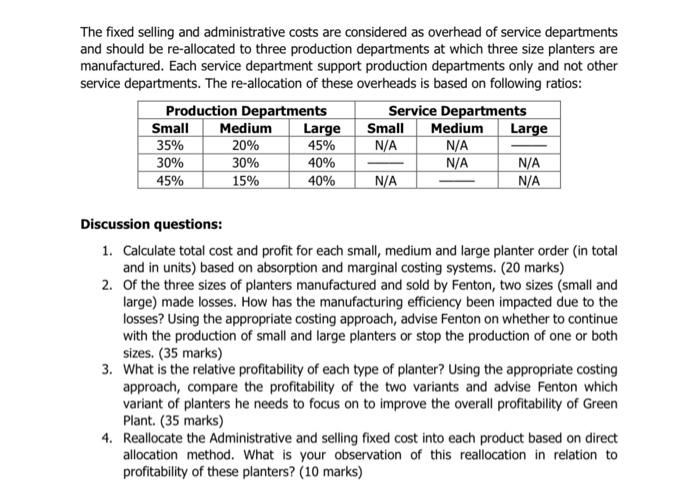

Fenton manufactures three types of timber planters. During 2021-22, Fenton sold 140,000 units of the medium size, 5,000 units of the small size, and 1,000 units of the large size planters. The overall profit on the sale of planters was 5,296,650. An analysis of the total sales, total costs incurred on manufacturing, selling, and other expenses showed that profit on the sales of the medium size planters was 6,431,000 while the small size and large size planters made losses of 499,250 and 635,100 respectively. Fenton, the owner of Green Plant, was unable to figure out the reasons for the loss on two types of planters, as he had started manufacturing these types only after making a detailed analysis of the market requirements. He wanted to find out whether Green Plant was running efficiently and decide whether to continue with the production of different wooden planter variants or confine himself to manufacturing and selling only one type of wooden planter. Fenton was in need of expert advice that would help him decide regarding the manufacturing efficiency of Green Plant. Background Fenton started a timber planters manufacturing unit in a newly formed industrial area in his town in the month of April 2021 and named it Green Plant. There was high demand for different types of products made out of timber material, and the market analysis showed that the demand for timber planters was quite high. The capacity of the planters usually ranged between 13 litres and 25 litres, and the demand for 21 litre planters was high. Keeping in view the market demand for planters of different capacities, Fenton installed the production capacity needed to manufacture different variants of the timber planters based on the specifications and requirements of the customers. Fenton invested a total of around 1.5 million on the land and building, and 6 million on plant and machinery. Initially, he wanted to focus on manufacturing 21 litre planters (medium size). The dimensions of one unit of a 21-litre planters were approximately 300 mm (30 cm) diameter and a height of 450 mm (45 cm). It weighted 1,000 grammes. The plant had the capacity to produce 60 planters per hour, and the raw material cost was 75,000 per metric tonne, i.e. 75 per kilo (i.e. 0.075 per gram). Direct wages were estimated to be 480 per hour i.e. 8 per planters manufactured. Also, other direct expenses were estimated to be around 120% of the labour cost and the fixed expenses for the maintenance of the plant were expected to be around 120,000 per month. The normal working hours were 18 hours per day, 25 days a month. The working hours per day could be increased to a maximum of 20 hours and the minimum working days in a month could be 15. Production and sales: The initial order was to manufacture and supply 15,000 units of the medium size planters, but 5,000 units to be delivered per month over the three-month period from April 2019 to June 2019. To manufacture and deliver the order, the manufacturing unit was operated only for 5 hours a day i.e. at less than its actual capacity of 18 hours per day. Fenton was successful in manufacturing and delivering all the 15,000 units, and it earned a profit of 501,000. Following the completion of the order, Fenton received another order for the manufacture and supply of 115,000 units of the medium-size planter. To complete the order, the plant had to operate at full capacity (18 hours a day, 25 days a month). The order had to be completed within 4 months. However, Fenton increased the production capacity from 18 hours a day to 20 hours to meet the target set by the customers, and delivered accordingly. The total profit from the second order (f.e. 115,000 units of medium size) was 6,121,000 and the delivery of all the planters was completed by mid-October 2019. In the meantime, Fenton had received requests for manufacturing other variants of planters. The requests were for 15 litre planters (small size) and 25 litre planters (large size). After analysing the market for the other variants, Fenton wanted to manufacture planters of small size on a limited scale and then to proceed to manufacturing large size. Fenton planned to manufacture both variants on a limited scale. From the month of November 2021, Fenton manufactured small size planters in addition to medium size. From January 2022, he also started manufacturing large size planters. Dimensions of Planters Blanket size Weight Height Diameter Small 750 grams 350 mm (35 cm) 200 mm (20 cm) Medium 1,000 grams 450 mm (45 cm) 300 mm (30 cm) Large 1,400 grams 550 mm (55 cm) 400 mm (40 cm) With the increase in production activities for different sizes of planters, Fenton incurred administrative and selling expenses on marketing related activities. The variable selling and administrative expenses were estimated to be 10 per unit, while the fixed administrative and selling expenses were estimated to be 230,000, Fenton allocated the total fixed administrative and selling expenses for each size of planter based on this dominated demand at 100,000, 80,000, and 50,000 for medium, small , and large sizes respectively. Earlier, Fenton did not consider the administrative and selling expenses in determining the profitability from the sale of 15,000 units and 115,000 units of medium size planters. Also, the diversification of production activities had increased the production related fixed cost by another 30,000, taking the total fixed production expenses to 150,000 per month (refer to table below for the breakup between variable expenses and fixed expenses among the three sizes of planters). Break-up between variable and fixed expenses of three sizes of planters Particulars Small Medium Large Total Units 5,000 units 140,000 units 1,000 units Selling price per unit 120 150 170 Manufacturing and production expenses: Material cost per unit 56.25 75 37.50 Labour cost per unit Other direct expenses 9.60 9.60 9.60 Fixed production overhead 600,000 600,000 600,000 Selling and Administrative Expenses Variable cost per unit 10 10 10 Fixed Cost (overhead) 80,000 100,000 50,000 8 E8 E8 The fixed selling and administrative costs are considered as overhead of service departments and should be re-allocated to three production departments at which three size planters are manufactured. Each service department support production departments only and not other service departments. The re-allocation of these overheads is based on following ratios: Production Departments Service Departments Small Medium Large Small Medium Large 20% 45% N/A N/A 30% 30% 40% N/A N/A 45% 15% 40% N/A N/A 35% Discussion questions: 1. Calculate total cost and profit for each small, medium and large planter order (in total and in units) based on absorption and marginal costing systems. (20 marks) 2. Of the three sizes of planters manufactured and sold by Fenton, two sizes (small and large) made losses. How has the manufacturing efficiency been impacted due to the losses? Using the appropriate costing approach, advise Fenton on whether to continue with the production of small and large planters or stop the production of one or both sizes. (35 marks) 3. What is the relative profitability of each type of planter? Using the appropriate costing approach, compare the profitability of the two variants and advise Fenton which variant of planters he needs to focus on to improve the overall profitability of Green Plant. (35 marks) 4. Reallocate the Administrative and selling fixed cost into each product based on direct allocation method. What is your observation of this reallocation in relation to profitability of these planters? (10 marks)