File Tools View article V ACCOUNTING - & FINANCE 0 Accounting and Finance 49 (2009) E49~871 An exploratory study of operational reasons to budget Prabhu

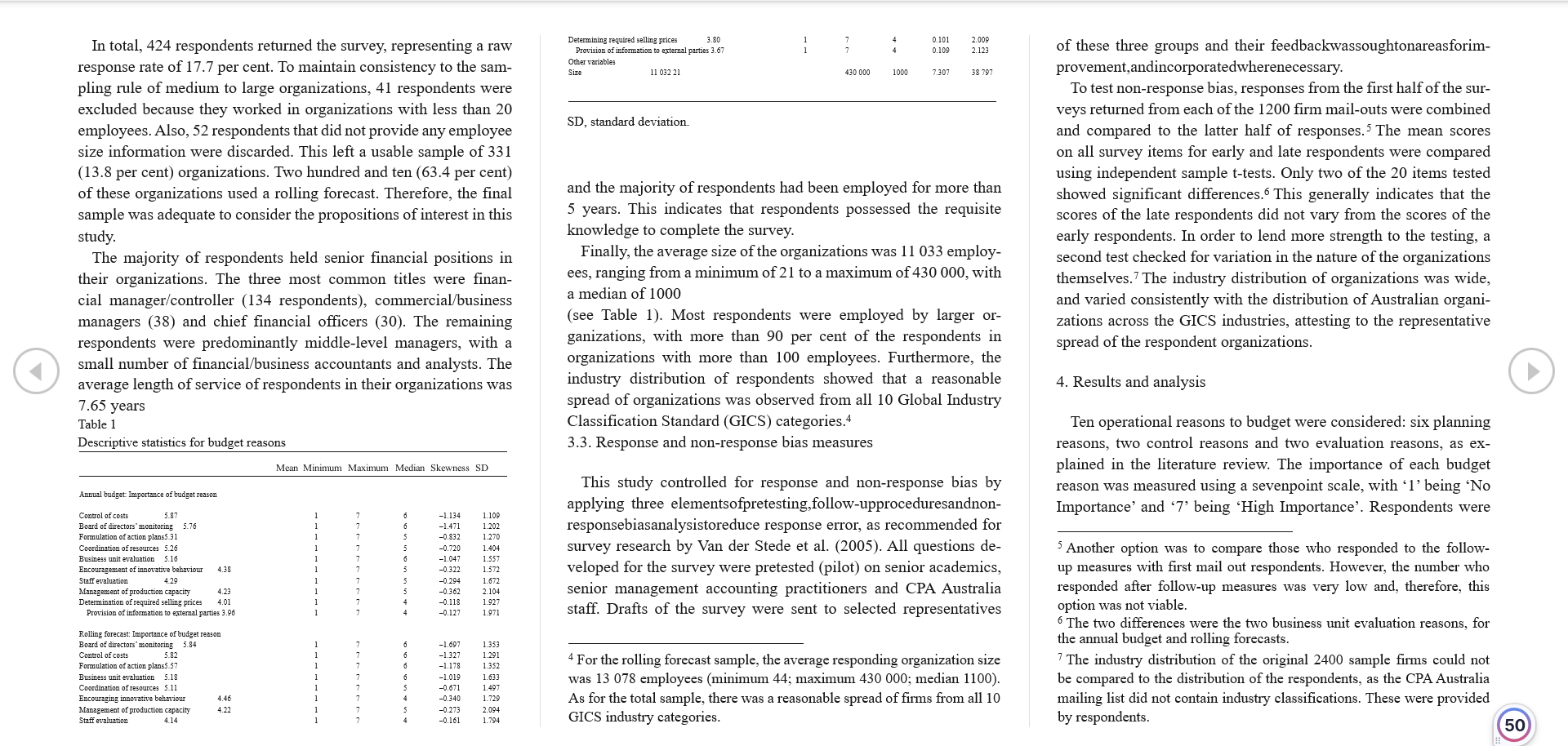

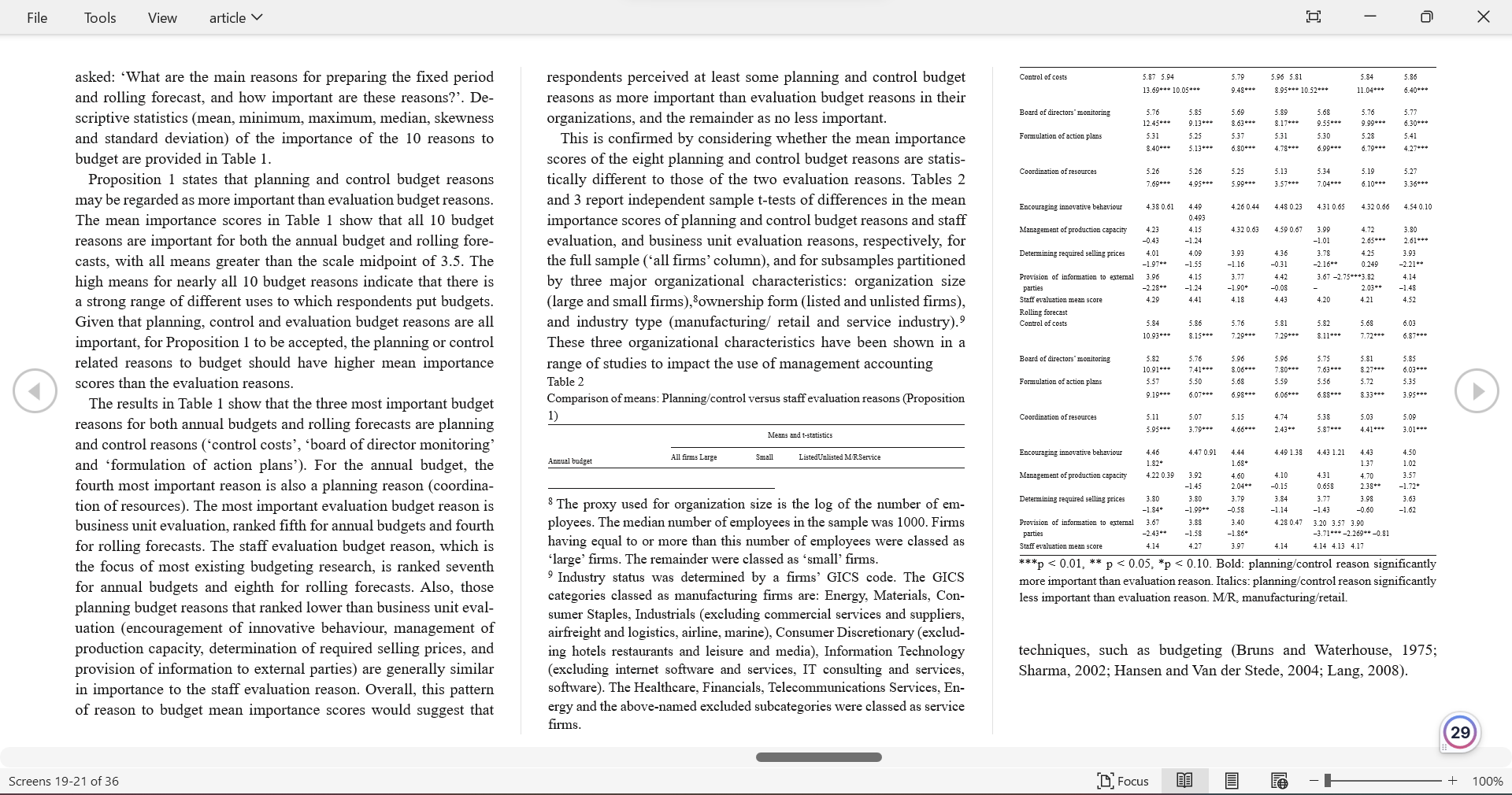

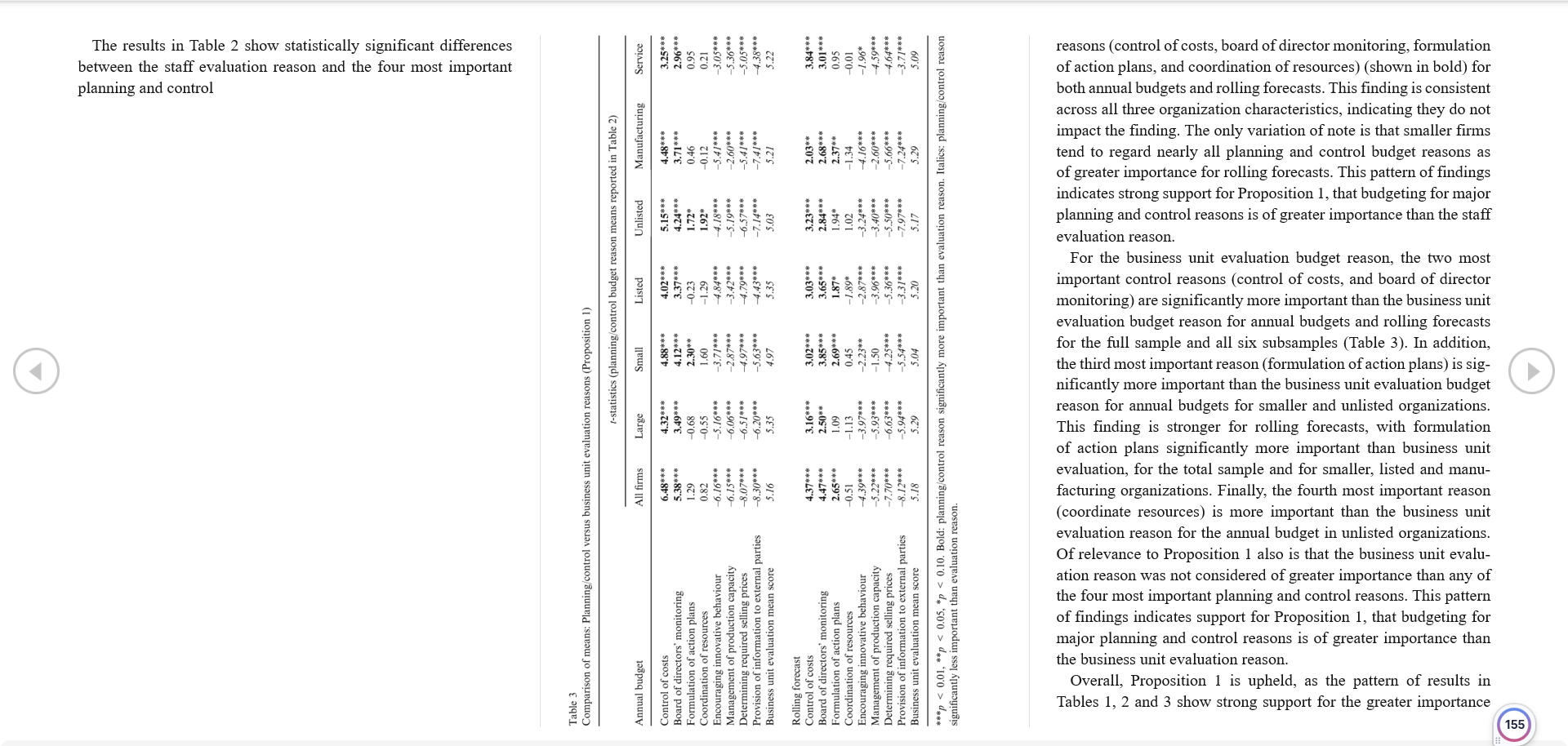

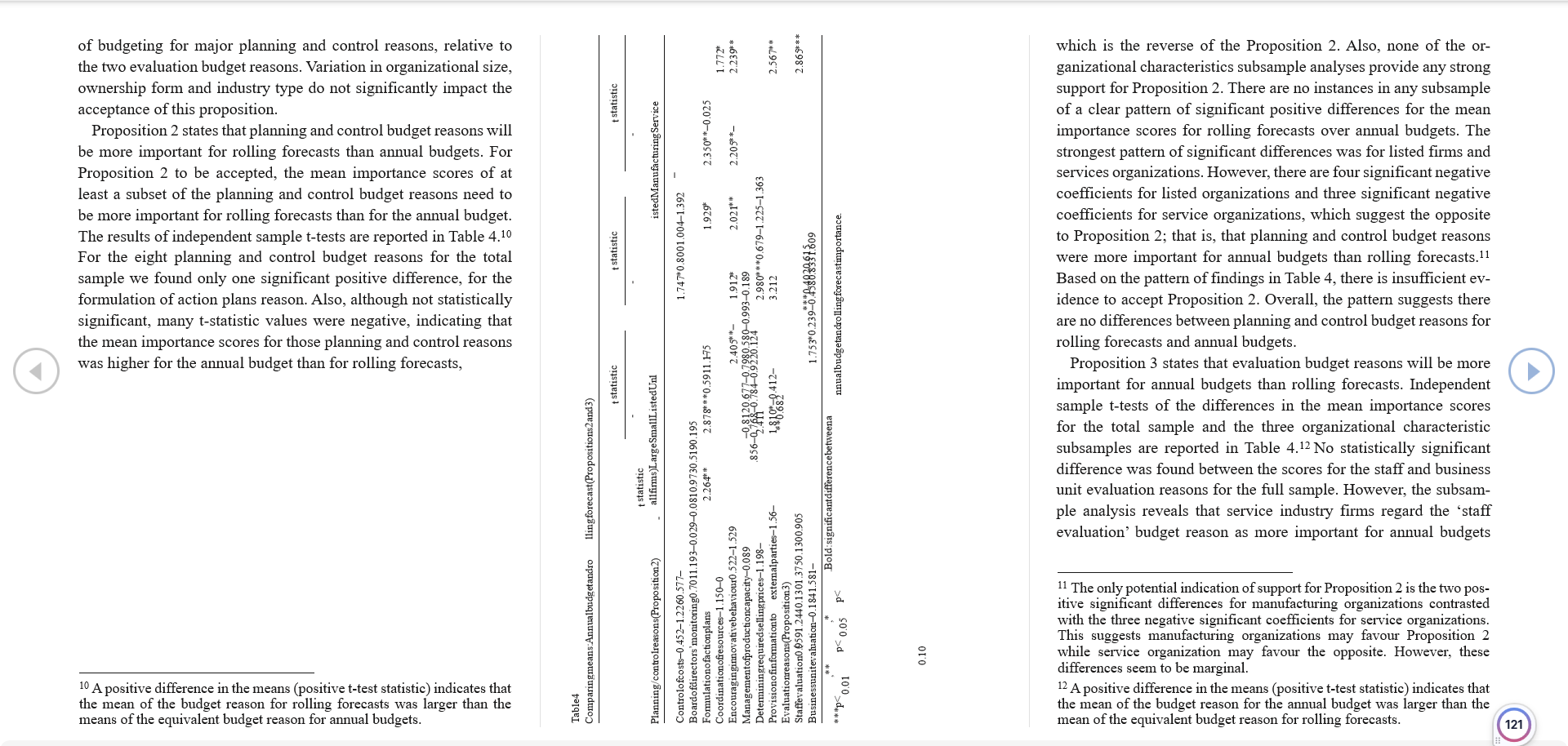

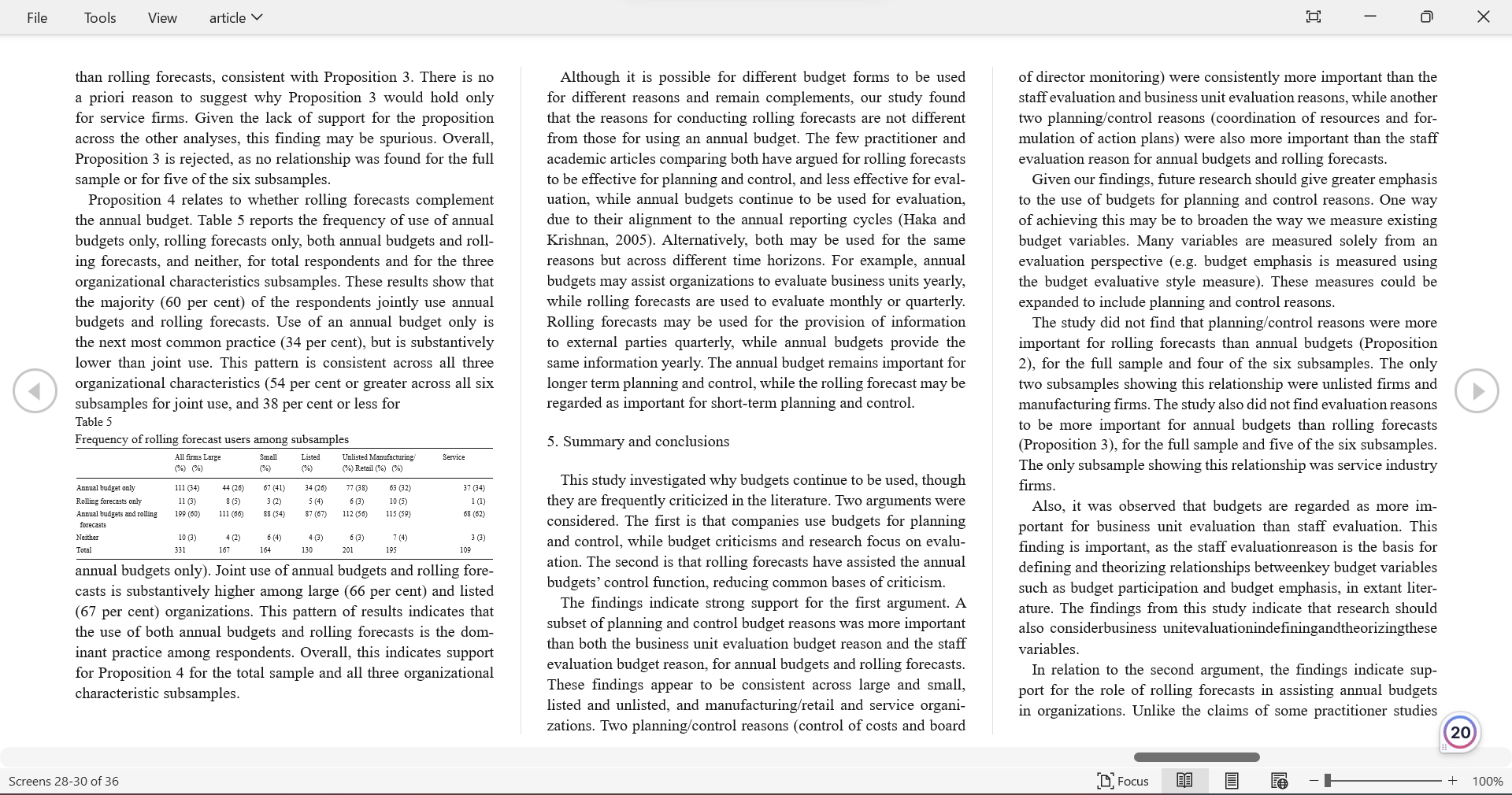

File Tools View article V ACCOUNTING - & FINANCE 0"\" Accounting and Finance 49 (2009) E49~871 An exploratory study of operational reasons to budget Prabhu Sivabalana, Peter Boothe, Teemu Malinib, David A. Browna a School of Accounting, University of Technology, Sydney. 20 07, Australia 'a Department of Accounting and Finance, Helsinki School of Economics, 00101 Helsinki, Finland Abstract Budgets are usedwidely but criticized. mainly for performance evaluation reasons. Wefindthatorganizationsregardbudgetsasmore irnportantforplanningandcontrol man evaluation, thus proposing a rationale for their continued use irrespective of evaluation-based criticisms. This nding is also important, because most extant budget research focuses on evaluation, suggesting a potential dis- connect between budget research and practice. We also find that rolling forecasts are used in tandemwiththe annualbudget in most organizations and for the samereasons. Thiswasunexpected.asco existencesuggeststheiradoptionfordifferentreasons. Key words: Budget; Management control; Rolling forecast JEL classication: M00 doi: 10.1111/j.1467~629X.2009.00305.x Screens 173 of 36 1. Introduction Budgets are often strongly criticized by practitioners and aca- demics (Wallander, 1999; Hope and Fraser. 2003; Jensen, 2003). Despite this, studies have shown that the vast majority of organ izations still use budgets (Umapathy, 1987; Ekholm and Wallin, 2000).1 This raises the question: if budgets are so problematic,why is it matmost organizations continue to use them? This study investigates two possible reasons. First, organizations may budget for reasons oier than those considered by critics of budgeting. Most budget research and prac titioner criticism focus on the use of budgets for evaluation reasons (Jensen, 2003; Hansen and Van der Stede, 2004). However, formal financial controls, such as annual budgets, migit also be used for planning and control reasons (Merchant and Van der Stede, 2003). Consequently, ifbudgets are used for planning and control as opposed to evaluation. many budget criticisms might no longer be relevant (or less so), and, therefore, explaining an organization's continued use of budgets. Second, rolling forecasts are argued by practitioners to be a substitute for die annual budget (Bogiages, 2004). Rolling forecasts involve more frequent forecasting by companies in order to gener- ate more accurate financial predictions; therefore. they overcome many of the problems claimed for annual budgets, which have been the focus of critique to date. Similar to die argument above, the use of improved budgeting practices may explain why budgeting persists despite the signicant criticisms in the literature. The present study examines the importance of 10 possible oper- ational reasons to budget in organizations. encompassing planning. control and evaluation. It also considers Whether rolling forecasts .EI. - a may enhance the outcomes from budgetary planning. control and evaluation. By examining these two major rationales, the study provides insights into the continued use of budgets, irrespective of criticisms. Results from our survey of 331 accountants in medium to large organizations indicate mat planning and control reasons are re- garded as more important than evaluation reasons for budgets. Furthermore, rolling forecasts seem to be used as complements to (not substitutes for) die annual budget. In addition, annual budgets and rolling forecasts are used for nearly identical reasons, Which is somewhat surprising. as We expected that the two budget forms would be used for di'ering purposes. Overall, the study contributes to the budget research literature by providing empirical evidence for the higher importance of a range of planning and control operational budget reasons in organizations. relative to evaluation reasons. This is sigiificant. because current contingency linkages between organizational char acteristics and budgetary characteristics such as budget emphasis, budget participation and budget use assume the evaluation reason when conceptualizing these variables (Brownell and Hirst, 1986; Brownell and Dunk, 1991). Therefore, the way in which research defines and theorizes budget variables could be broadened beyond the evaluation reason to maintain relevance in the analysis of esmblished contingency relationships. This study also contributes to developing literature on rolling forecasts by providing empirical evidence that annual budgets and rolling forecasts are used in parallel for essentially similar opera tional budget reasons. This suggests a collaborative use of annual budgets and rolling forecasts rather than the current arguments that rolling forecasts are substitutes for annual budgets. The next section reviews the budget literature by first examining research that has investigated evaluation budget reasons. This is X E I+ 33: Focus i00% followed by a discussion of the 10 operational budget reasons considered in this study. Following from this is an analysis of the relationship between rolling forecasts and annual budgets, Section 3 outlines the research method adopted for this study. This is followed by a discussion ofthe results, conclusions and limitations of the study. 2. Literature review and proposition development 2.1. Evaluation focus The three key performance evaluation constructs used in budget research are budget emphasis, budget participation and budget use. All three have been considered extensively, including the participa tive budgeting and Reliance on Accounting Performance Measures (RAPM) research areas.1 The budget emphasis construct considers the focus given by an organization to the budget (Hopwood, 1972). Budget emphasis proxies the extent to which a company focuses on budgets as a management control device. A high budget emphasis indicates a strong focus. while a low budget emphasis is the reverse. An analysis of the items used to measure this construct shows that mey have a strong staff evaluation focus (see Hopwood, 1972). Indeed. the term used to describe the budget emphasis measure is 'budget evaluative style\impacts on budget use may be different. For example, in a high uncertainty environment. organizations may not use budgets to evaluate staff due to the difcult predictive circumstances making the budget an irrelevant performance benchmark. However. in the same setting, organizations may still want to know how a business unit has been performing relative to a budget. Although uncon- trollable factors might have impacted upon this assessment, it is still useful for an organization to know whether its business units have done better or worse than budget. In this setting, the use of budgets for business unit evaluation may be mgr. While it may be low for staff evaluation. Therefore, it is possible that in different contexts me use of budgets for staff evaluation and for business unit evaluation may be aligned in different Ways. This specificityin the analysis of evaluation budget reasons has not been considered in existing research. 2.2.2. Flaming reasons Operational planning budget reasons include coordination of resources. formulation of action plans. management of production capacity. determination of required selling prices, encouragement of innovative behaviour and provision of information to exter- nal parties. These reasons were derived from an investigation of existing academic and practitioner research. Coordination of resources is a key operational planning reason that is discussed in extant participative budgeting research. but not explicitly studied. Organizations often create budgets in order to inform departments and other organizational units about their funding constraints. prior to period commencement. Departments request a budget, and a budget committee comprising senior man a gers negotiates an amount with departments. The resulting budget must be adhered to by departments (Brownell and Dunk1 1991). Therefore, coordination of resources is the process of requesting and negotiating budget funds. A budget might also be used as a means of formulation of action plans. In many organizations. budgets assist organizations to cost a range of alternative courses of action (Merchant and Van der Stede. 2003). This reason may not be department specic. It relates to the use of budget dam to assist choosing between competing alternatives, Budgets might also be used to assist organizations in the man- agement ofproduction capacity in an upcoming period. Through standard costing variables such as the 'normal capacity' value, budgets allow organizations to reect on their level of activity and the extent to which they utilize their operating capacity (Langfield Smith et al., 2005). The expected costs determined in a budget may be used as the ba- sis for the determination of required selling prices in an upcoming period. The use of standard costing systems in many organizations requires the implementation of forecast numbers to cost products in advance (LangeldSmith et al.. 2005). This directly impacts upon the determination of selling prices. Budgets may be created for me encouragement of innovative be- haviour. Through the planning process. orgamzations can increase the amounts allocated to specic areas of die business, to stimulate certain types of behaviours amongst staff The relationship between budget emphasis and innovative behaviours within a management control context has been explored in existing management ac counting research. For example, Subramaniarn and Mia (2003) find that the allocation ofmore flexible budget-based evaluation suited marketing managers due to their greater emphasis on innova tion, relative to production managers. Therefore, an appropriately constructed budget might encourage innovative actions. Budget numbers are oen created for the provision of infor mation to external parties (Merchant and Van der Stede, 2003). Most publicly listed medium and large organizations create annual budgets and shoner period forecasts to satisfy market information requirements. Budgets may also be provided to creditors. inform- ing them of an organization's expected future nancial position. 2.2.3. Control reasons The two control budget reasons are a monitoring device by the board of directors and control of costs. Both relate to the man agement of organizations using budgets during a specic period. Budgets are oen used as a monitoring device by the board of directors of an organization througi formal approval of What is expected in a future period and then regular review of perfor mance against budget (Baysinger and Butler, 1985), The budget is one of the few formal financial controls provided to directors and represents a nancial expectation communicated from senior management to directors, From an operational perspective. direc tors may use me budget to monitor an organization's progress intraperiod, noting signicant deviations and questioning senior management regarding progress. During a period. budgets also directly allow the control ofcosts by organizations mtraperiod, by managing their budgeted spending constraints. Given that budgets embed knowledge ofspending ex- pectations, organizations are better able to focus on keeping costs to budget during a period and actively engage in efforts to control costs. Having considered the 10 operational budget reasons. We now explain how the main budget criticisms relate primarily to the two evaluation reasons. This is important, as the motivation for organizations to continue using budgeting irrespective of criticisms only has validity if the root criticisms of budgeting stem from the evaluation reason. 2. 3. Budget criticisms The seminal research by Argyris (1952) established the core themes of evaluationrelated budget criticism. He explained that most organizations use budgets as a device for motivating staff, but mat this motivating factor could be over-ridden by the presence of Job-Related Tension (JRT). Argyris (1952) argues that IRT occurs when staff perceive budgets as difficult to achieve. The presence of RT causes employees to modify their behaviour in suboptimal ways) to achieve the budget target Employees do so because they feel the pressure of meeting a budget and they alter the opera tional conditions in meir environment or the budgeting process in response. Hopwood (1972) and Otley (1978) similarly considered the relation between budget emphasis (staff evaluation focus) and or ganizational outcomes. Furthermore, budget research in doe 1980s and 19905 was characterized by panicipative budgeting (Shields and Shields, 1998) and RAPM (Hartmarm, 2000) research, which predominantly focused on budgets as an evaluative mechanism. Later research focused on the evaluation challenges. including Wallander's Work (1999) and the stream of participative budgeting research discussed in Shields and Shields (1998). The RAPM liter attire also acknowledges the detrimental effects of budget use when used as an evaluation device. in their consideration of budgetbased targets for performance measurement (Hartmann. 2000). While the use of budgets for planning and control also may be problematic, these difculties may partly result from the use of budgets for evaluation. For example, when companies use budg- ets to evaluate staff, staff may engage in gameplaying (Jensen, 2003) during the preperiod planning stage. This directly thwarts the planning and control processes relating to budgeting, as the budget numbers developed are not sufficiently accurate and, therefore. not regarded as important by staff (often the same individuals gaming the budget). Therefore, planning and control difficulties result from the use of budgets for evaluation. Hope and Fraser (2003) similarly argued that as a result ofthe evaluationrelated problems in budg eting, organizations should abandon budgeting and adopt a more activity-focused approach to forecasting that is cross-departmental and less likely to engender managerial gaming. If me majority of budget criticisms relate to budgets as an eval- uation tool, and organizations continue to use budgets, mis may be explained by organizations placing greater imponance on planning and control budget reasons than on evaluation reasons. Of course, it is unrealistic to assert that all planning and control reasons will be more impormnt, given the exploratory nature of this study. However. at least a subset of planning and control reasons should be more important, given the arguments presented. This leads to the first proposition: Pi: Flaming and control budget reasons are more important than evaluation budget reasons. 2.4. Rolling forecasts Organizations are increasingly using alternative budget forms such as rolling forecasts for management control (Barrett, 2003; Bogiages. 2004; Lynn and Madison. 2004; Haka and Krishnan, 2005). A rolling forecast is usually produced monthly or quarterly, and enables organizations to periodically adjust its expected num- bers within an annual period to reect the current market realities faced by companies (Haka and Krishnan, 2005). Existing studies argue that by using rolling forecasts to forecast more frequently than once per annum (annual budget). companies are able to re duce the detrimental effects of uncertainty on budgeting (Bogiages, 2004). In some organization case studies, practitioners have described the use of rolling forecasts (Bittlestone, 2000). Howeven little research has investigated the extent to which rolling forecasts ex- ist across organizations. Furthermore, the majority of practitioner studies have argued for the use of rolling forecasts as a substitute for annual budgets (Bittlestone. 2000; Bogiages, 2004; Lynn and Madison, 2004). However, this argument appears contrary to the reality of high annual budget use in organizations (Umapathy, 1987; Ekholm and Wallin, 2000). The present study provides em- pirical insights to inform the debate on whether roUing forecasts are substitutes for or complements to the annual budget. This study also considers the reasons for using rolling forecasts and compares them to the reasons for using annual budgets. By forecasting over short periods, the rolling forecast reduces the time interval between planning and business reality. This should make organizations more competitive and responsive to change (Gurton. 1999; Neely et al.. 2001), especially When economic con ditions rapidly change. The annual budget, by contrast, has been argued to be out ofdate too soon after it is created (Myers. 2001). This problem is minimized when budgeting more frequently. Also. and as a result of more accurate and frequent predictions, rolling forecasts facilitate organizational learning and provide managers with more confidence in the budget numbers that are used for short term operational planning (Hansen et al.. 2003; Haka and Krishnan, 2005). From a performance evaluation perspective, evidence on the impact of rolling forecasts is mixed. Staff may nd it more dif- ficult to take 'free rides' (Myers. 2001) when their annual targets are met well prior to the end of a period, since, under a rolling File Tools View article V forecast system. updates to numbers occur monthly or quarterly. Thereforerolling forecasts reduce the 'free ride' period and, hence. provide more relevant accounting numbers for performance eval- uation. However. Gurton (1999) argues that rolling forecasts can negatively affect performance evaluation. because evaluating indi viduals over shorter periods provides much higher administrative workloads for management, and the performance evaluation pro- cess becomes more cumbersome. Also. because budgets are prone to change. it is difficult to provide staff with a performance eval uation target using rolling forecasts, The target will continually change as budgets change. Haka and Krishnan (2005) similarly argued that rolling forecasts reduce goal congruence, as they frequently shift budget targets for staff. when used for evaluation. Ifrollingforecastsareintroducedprimarilyforensuringbetterqual ityshort-term predictions.andtheannualbudgetislesscapableofpro- ducingaccuratepredictions (Haka and Krishnan. 2005). men plan- ning and control reasons should be more importantforrollingfore- caststhanforannualbudgets.asproposedbelow. P2: Planning and control budget reasons are regarded as more important for rolling forecasts than for annual budgets. However. as noted above, rolling forecasts can cause goal con gruence problems for employees. as targets frequently change wim each new forecast (Haka and Krishnan. 2005). This makes it increasingly diicult for employees to know what performance targets to aim for. and the use of rolling forecasts for performance evaluation can be difficult. Annual budgets are also more suited to staff evaluation than rolling forecasts, as formal performance evaluation is most often conducted on an annual basis. Hence. the setting of annual evaluation targets based on annual budgets is more aligned, Although evaluation budget reasons are expected to be less important than planning and control reasons. they will be more important for annual budgets than for rolling forecasts. Screens 10712 of 35 P3: Evaluation budget reasons are regarded as more important for annual budgets man for rolling forecasts, The final proposition relates to whether the rolling forecast is a substitute for or complement to the annual budget. Extant research has shown that annual budget usage is high in organiza tions (Umapathy, 1987; Ekhohn and Wallin, 2000). Practitioners have suggested that the rolling forecast addresses the predictive deficiencies of the annual budget (Bogiages, 2004). and many practitioner articles have argued that it should replace the annual budget However. if rolling forecasts are used for different budget reasons, as presented in Propositions 2 and 3. both budget forms may complement each other and coexist. It is also possible that bom rolling forecasts and annual budgets may coexist in some cir cumstances Where they are used for the same reasons. For example. the annual budget may be used for annual business unit evaluation. wim rolling forecasts used for monthly or quarterly business unit evaluation, This leads to the following proposition. Pi: Rolling forecasts complement the annual budget 3. Research method 3.1. Overview The study used a crosssectional mailed survey of senior man agement accountants With a CPA qualication. The study repre sented collaboration between the University of Technology, Syd- ney and CPA Australia. which provided a grant to suppon the project, including access to its membership databaseJThe CPA Australia professional accounting body is one of the two largest accounting bodies in Australia. and comprises approximately 110 2 The grant investigated two related management accounting issues. re- sulting in an industry report for CPAAustralia members. .EI. - G 000 members around the World. across 92 countries. Given the ac counting background of its members. the use of the CPAAustralia members for studying budgeting was deemed appropriate. 3.2. Survey approach and sample The cross-sectional survey was sent to 2400 respondents ran domly selected from the CPAAustralia membership. To explore the rolling forecast propositions. a reasonable number of rolling fore- cast users was required. As overall survey response rates could be around 20 per cent. and as Hansen and Van der Stede (2004) found that around 25 per cent ofrespondents use a rolling forecast. a large sample was needed to ensure a reasonable number of responses from both annual budget and rolling forecast users for statistical analysis, The sample selected from the CPA Australia membership database comprised members wim senior managerial job titles (finance manager. chief financial ofce and financial controller). employed in medium and large organizations3 or strategic business units of larger organizations. Only one member was surveyed from any one organization/strategic business unit. For administrative convenience. the survey mailout was con ducted in two stages, 6 weeks apart. with 1200 potential respond- ents in each. No organization in the first mailout was a part of the second mail~out For each mailout. respondents were given 4 weeks to respond. A follow-up reminder postcard was then sent. encouraging participation. Follow-up respondents who required another survey copy were provided With a contact number to request the survey 3 This study only considers medium to large organizations. The Australian Bureau of Statistics denes a medium organization by employee Size in be no less than 20 employees. E I+ 33: Focus l00% In total, 424 respondents returned the survey, representing a raw Determining required selling prices 3.80 0.10 2.009 Provision of information to external parties 3.67 0.100 2.123 of these three groups and their feedbackwassoughtonareasforim- response rate of 17.7 per cent. To maintain consistency to the sam- Other variables Siz 11 032 21 430 000 1000 7.307 38 797 provement, andincorporatedwherenecessary. pling rule of medium to large organizations, 41 respondents were To test non-response bias, responses from the first half of the sur- excluded because they worked in organizations with less than 20 veys returned from each of the 1200 firm mail-outs were combined SD, standard deviation. employees. Also, 52 respondents that did not provide any employee and compared to the latter half of responses. The mean scores size information were discarded. This left a usable sample of 331 on all survey items for early and late respondents were compared (13.8 per cent) organizations. Two hundred and ten (63.4 per cent) using independent sample t-tests. Only two of the 20 items tested of these organizations used a rolling forecast. Therefore, the final and the majority of respondents had been employed for more than showed significant differences. This generally indicates that the sample was adequate to consider the propositions of interest in this 5 years. This indicates that respondents possessed the requisite scores of the late respondents did not vary from the scores of the study. knowledge to complete the survey. early respondents. In order to lend more strength to the testing, a The majority of respondents held senior financial positions in Finally, the average size of the organizations was 11 033 employ- second test checked for variation in the nature of the organizations their organizations. The three most common titles were finan- ees, ranging from a minimum of 21 to a maximum of 430 000, with themselves. The industry distribution of organizations was wide, cial manager/controller (134 respondents), commercial/business a median of 1000 and varied consistently with the distribution of Australian organi- managers (38) and chief financial officers (30). The remaining (see Table 1). Most respondents were employed by larger or- zations across the GICS industries, attesting to the representative respondents were predominantly middle-level managers, with a ganizations, with more than 90 per cent of the respondents in spread of the respondent organizations. small number of financial/business accountants and analysts. The organizations with more than 100 employees. Furthermore, the average length of service of respondents in their organizations was industry distribution of respondents showed that a reasonable 4. Results and analysis 7.65 years spread of organizations was observed from all 10 Global Industry Table 1 Classification Standard (GICS) categories. Ten operational reasons to budget were considered: six planning Descriptive statistics for budget reasons 3.3. Response and non-response bias measures reasons, two control reasons and two evaluation reasons, as ex- Mean Minimum Maximum Median Skewness SD plained in the literature review. The importance of each budget This study controlled for response and non-response bias by Annual budget Importance of budget reason reason was measured using a sevenpoint scale, with '1' being 'No applying three elementsofpretesting, follow-upproceduresandnon- Control of costs 5.87 Importance' and '7' being 'High Importance'. Respondents were -1.134 1.109 Board of directors' monitoring 5.76 -1.4 1.202 responsebiasanalysistoreduce response error, as recommended for Formulation of action plans5.31 -0.832 1.270 Coordination of resources 5.26 -0.720 1.404 Business unit evaluation 5 1.047 survey research by Van der Stede et al. (2005). All questions de- Another option was to compare those who responded to the follow- Encouragement of innovative behaviour 4.38 HUHPPPPPP 0.322 1.572 veloped for the survey were pretested (pilot) on senior academics, up measures with first mail out respondents. However, the number who Staff evaluation 4.29 0.294 1.672 Management of production capacity 1 23 0.362 2.104 senior management accounting practitioners and CPA Australia responded after follow-up measures was very low and, therefore, this Determination of required selling prices 4.01 1.927 Provision of information to external parties 3.90 1.971 staff. Drafts of the survey were sent to selected representatives option was not viable. The two differences were the two business unit evaluation reasons, for Rolling forecast: Importance of budget reason Board of directors" monitoring 5.84 the annual budget and rolling forecasts. Control of costs 1327 1.353 5.82 1.291 Formulation of action plans5.57 1.178 1.352 For the rolling forecast sample, the average responding organization size The industry distribution of the original 2400 sample firms could not Business unit evaluation 5.18 1.019 1.633 Coordination of resources 5.11 0.671 1.497 was 13 078 employees (minimum 44; maximum 430 000; median 1100). be compared to the distribution of the respondents, as the CPA Australia Encouraging innovative behaviour 4.46 0.340 1.729 As for the total sample, there was a reasonable spread of firms from all 10 4.22 mailing list did not contain industry classifications. These were provided Management of production capacity 0.2 2.094 Staff evaluation 4.14 0.161 GICS industry categories. by respondents. 50File Tools View article V X asked: 'What are the main reasons for preparing the fixed period respondents perceived at least some planning and control budget Control of costs 5.87 5.94 5.79 5.96 5.81 5.84 5.86 13.69*+* 10.05+*+ 9.48+*+ 8.95*+$ 10.52+*+ 11.04+*+ 6.40*++ and rolling forecast, and how important are these reasons?'. De- reasons as more important than evaluation budget reasons in their Board of directors' monitoring 5.82 scriptive statistics (mean, minimum, maximum, median, skewness organizations, and the remainder as no less important. 3.70 5.69 3.89 5.68 5.76 5.73 12.45+4. 9.13+. 8.63+*+ 8.17*+ 9.55+4. 9.90-+ 6.30*+ and standard deviation) of the importance of the 10 reasons to This is confirmed by considering whether the mean importance Formulation of action plans 5.31 5.25 5.37 5.31 5.30 5.28 5.41 8.40*+ 5.13*4. 6.80*+. 6.99+4 6.79*+ 4.27*++ budget are provided in Table 1. scores of the eight planning and control budget reasons are statis- tically different to those of the two evaluation reasons. Tables 2 Coordination of resources 5.26 3.20 5.23 5.13 5.34 5.19 3.27 Proposition 1 states that planning and control budget reasons 7.69-+ 4.95++* 3.57+4+ 7.04++* 6.10*++ 3.36+*+ may be regarded as more important than evaluation budget reasons. and 3 report independent sample t-tests of differences in the mean Encouraging innovative behaviour 4.38 0.61 4.49 4.26 0.44 4.48 0.23 4.31 0.65 4.32 0.66 4.54 0.10 The mean importance scores in Table 1 show that all 10 budget importance scores of planning and control budget reasons and staff 0.493 Management of production capacity 4.2 4 15 4.32 0.63 4.59 0.67 3.99 4.72 3.80 reasons are important for both the annual budget and rolling fore- evaluation, and business unit evaluation reasons, respectively, for -0.43 -1.24 .1.01 2.65*+ 2.610*+ Determining required selling prices 4.01 4.09 3.9 4,30 3.78 425 3.93 casts, with all means greater than the scale midpoint of 3.5. The the full sample ('all firms' column), and for subsamples partitioned -1.97** 1 55 1 16 -0.31 2.16* 0.249 -2.21* high means for nearly all 10 budget reasons indicate that there is by three major organizational characteristics: organization size Provision of information to external 3.96 4.15 3.37 4.42 3.67 -2.75**+3.82 4.14 parties -2.28++ -1.90 0.08 2.03- -1.48 a strong range of different uses to which respondents put budgets. (large and small firms), Sownership form (listed and unlisted firms) Staff evaluation mean score 4 41 4 18 4.21 4 52 Rolling forecast Given that planning, control and evaluation budget reasons are all and industry type (manufacturing retail and service industry)." Control of costs 5.84 5.86 5.76 5.81 5.82 5.68 6.03 8.15+. 7.29+4. 8.11*.* important, for Proposition 1 to be accepted, the planning or control 6.87++ These three organizational characteristics have been shown in a 10.93+ related reasons to budget should have higher mean importance range of studies to impact the use of management accounting Board of directors' monitoring 3.82 5.76 5.96 5.96 5,72 5.81 5.85 10.91+4. 7.41+4. 8.06+* 7.63+4. 8.27+. 6.03-+. scores than the evaluation reasons. Table 2 Formulation of action plans 5.57 5.50 5.68 5 50 5.56 5 72 5.35 9.19-4. 5.07-4. 6.06+* The results in Table 1 show that the three most important budget Comparison of means: Planning control versus staff evaluation reasons (Proposition 8.33+.+ 3.05+ + 1) Coordination of resources 5.11 5.07 5.15 5.03 5.09 reasons for both annual budgets and rolling forecasts are planning 5.95+4. 3.70-+ 4.66*** 2.43*+ 5.87++. Means and t-statistics 4.41**+ 3.01*+ and control reasons ('control costs', 'board of director monitoring' All firms Large Small ListedUnlisted MR.Service Encouraging innovative behaviour 4.4 4.47 0.91 4.44 4.49 1.38 4.43 1.21 4.43 4.50 and 'formulation of action plans'). For the annual budget, the Annual budget 1.82* 1 68 1.02 Management of production capacity 4.22 0.39 3.9. 4.60 431 70 3.57 fourth most important reason is also a planning reason (coordina -1.45 2.04*+ 0.15 0.658 2.38+- -1.72+ tion of resources). The most important evaluation budget reason is The proxy used for organization size is the log of the number of em- Determining required selling prices 3.80 3.80 3.79 3.84 3.77 3.98 3.63 -1.84 -1.99+ -0.58 -1.14 -1.43 -0.60 -1.62 business unit evaluation, ranked fifth for annual budgets and fourth ployees. The median number of employees in the sample was 1000. Firms Provision of information to external 3.67 3.88 3.40 4.28 0.47 3.20 3.57 3.90 parties -2.43*+ -1.58 -1.86* -3.71**-2.269"* -0.81 for rolling forecasts. The staff evaluation budget reason, which is having equal to or more than this number of employees were classed as Staff evaluation mean score 4.14 3.0 4.14 .14 4.13 4.17 the focus of most existing budgeting research, is ranked seventh 'large' firms. The remainder were classed as 'small' firms. * **p

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance