Answered step by step

Verified Expert Solution

Question

1 Approved Answer

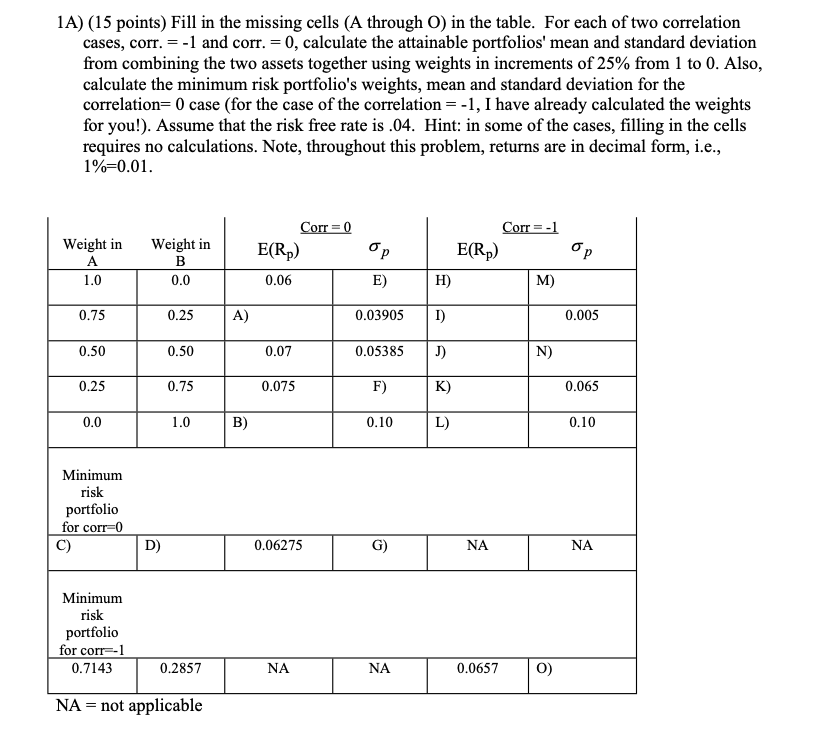

Fill in the missing cells ( A through O ) in the table. For each of two correlation cases, corr. = - 1 and corr.

Fill in the missing cells A through O in the table. For each of two correlation

cases, corr. and corr. calculate the attainable portfolios' mean and standard deviation

from combining the two assets together using weights in increments of from to Also,

calculate the minimum risk portfolio's weights, mean and standard deviation for the

correlation case for the case of the correlation I have already calculated the weights

for you! Assume that the risk free rate is Hint: in some of the cases, filling in the cells

requires no calculations. Note, throughout this problem, returns are in decimal form, ie

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Successful Fundraising For Arts And Cultural Organizations

Authors: Carolyn S. Friedman, Karen B. Hopkins

2nd Edition

1573560294, 978-1573560290