Answered step by step

Verified Expert Solution

Question

1 Approved Answer

finance questions it is clear you do one thing pass that question to finance guy it was added by mistake by to advanced math Company

finance questions

it is clear you do one thing pass that question to finance guy it was added by mistake by to advanced math

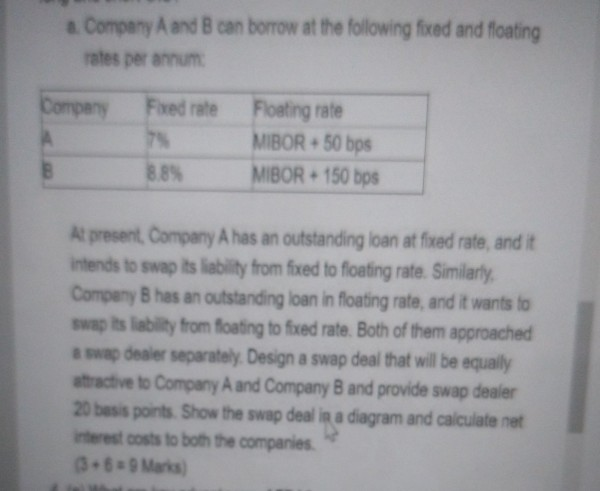

Company A and B can borrow at the following fixed and floating rates per annum Company Fixed rate 75 8.8% Foating rate MIBOR +50 bps MIBOR - 150 bps B At present Company A has an outstanding loan at fixed rate, and it intends to swap its liability from fixed to floating rate. Similarly, Company B has an outstanding loan in floating rate, and it wants to swap its ability from floating to fixed rate. Both of them approached & swap dealer separately. Design a swap deal that will be equally attractive to Company A and Company B and provide swap dealer 20 basis points. Show the swap deal in a diagram and calculate net interest costs to both the companies 3.69 Mars)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Term Structure Models A Graduate Course

Authors: Damir Filipovic

2009th Edition

364226915X, 978-3642269158