Answered step by step

Verified Expert Solution

Question

1 Approved Answer

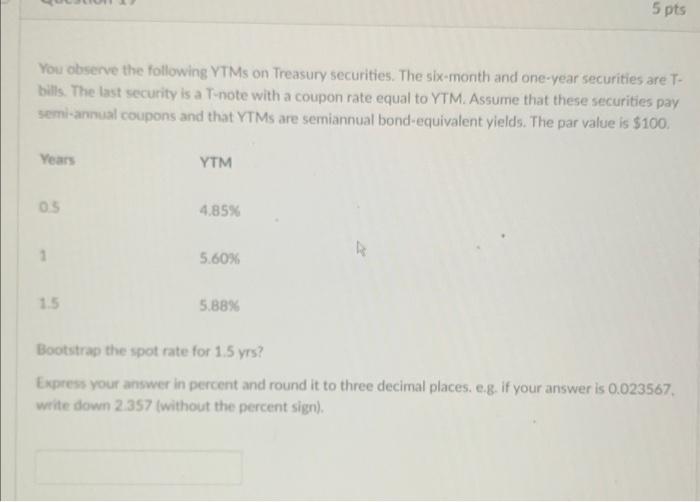

finance You observe the following YTMs on Treasury securities. The six-month and one-year securities are Tbills. The last security is a T-note with a coupon

finance

You observe the following YTMs on Treasury securities. The six-month and one-year securities are Tbills. The last security is a T-note with a coupon rate equal to YTM. Assume that these securities pay sem-annual coupons and that YTMs are semiannual bond-equivalent yields. The par value is $100. Bootstrap the spot rate for 1.5 yrs? Express your answer in percent and round it to three decimal places. e.g. if your answer is 0.023567. write down 2.357 (without the percent sign) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Sport Funding And Finance

Authors: Bob Stewart

2nd Edition

041583984X, 978-0415839846