Answered step by step

Verified Expert Solution

Question

1 Approved Answer

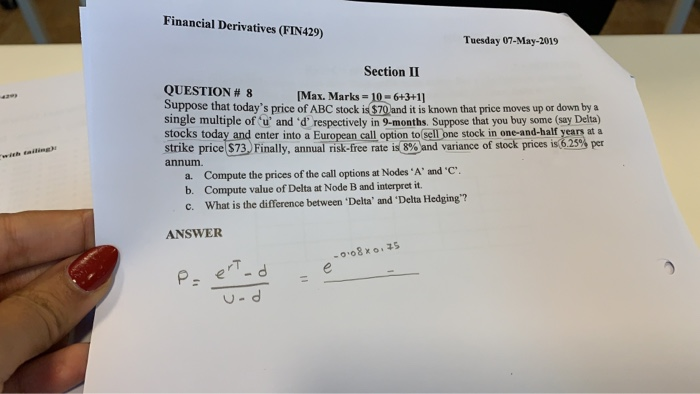

Financial Derivatives (FIN429) Tuesday 07-May-2019 Section II QUESTION # 8 Suppose that today's price of ABC stock is $70and it is known that price moves

Financial Derivatives (FIN429) Tuesday 07-May-2019 Section II QUESTION # 8 Suppose that today's price of ABC stock is $70and it is known that price moves up or down by a single multiple of u' and 'd' respectively in 9-months. Suppose that you buy some (say Delta) stocks today and enter into a strike price $73. Finally, annual risk-free rate is 80 and variance of stock prices is 25% per annum Max. Marks-10-6+3+1] 299 uropean call option to sell one stock in one-and-half years at a S ailingh a. Compute the prices of the call options at Nodes"A" and b. Compute value of Delta at Node B and interpret it. c. What is the difference between 'Delta' and 'Delta Hedging"? ANSWER YT u-d Financial Derivatives (FIN429) Tuesday 07-May-2019 Section II QUESTION # 8 Suppose that today's price of ABC stock is $70and it is known that price moves up or down by a single multiple of u' and 'd' respectively in 9-months. Suppose that you buy some (say Delta) stocks today and enter into a strike price $73. Finally, annual risk-free rate is 80 and variance of stock prices is 25% per annum Max. Marks-10-6+3+1] 299 uropean call option to sell one stock in one-and-half years at a S ailingh a. Compute the prices of the call options at Nodes"A" and b. Compute value of Delta at Node B and interpret it. c. What is the difference between 'Delta' and 'Delta Hedging"? ANSWER YT u-d

Financial Derivatives (FIN429) Tuesday 07-May-2019 Section II QUESTION # 8 Suppose that today's price of ABC stock is $70and it is known that price moves up or down by a single multiple of u' and 'd' respectively in 9-months. Suppose that you buy some (say Delta) stocks today and enter into a strike price $73. Finally, annual risk-free rate is 80 and variance of stock prices is 25% per annum Max. Marks-10-6+3+1] 299 uropean call option to sell one stock in one-and-half years at a S ailingh a. Compute the prices of the call options at Nodes"A" and b. Compute value of Delta at Node B and interpret it. c. What is the difference between 'Delta' and 'Delta Hedging"? ANSWER YT u-d Financial Derivatives (FIN429) Tuesday 07-May-2019 Section II QUESTION # 8 Suppose that today's price of ABC stock is $70and it is known that price moves up or down by a single multiple of u' and 'd' respectively in 9-months. Suppose that you buy some (say Delta) stocks today and enter into a strike price $73. Finally, annual risk-free rate is 80 and variance of stock prices is 25% per annum Max. Marks-10-6+3+1] 299 uropean call option to sell one stock in one-and-half years at a S ailingh a. Compute the prices of the call options at Nodes"A" and b. Compute value of Delta at Node B and interpret it. c. What is the difference between 'Delta' and 'Delta Hedging"? ANSWER YT u-d

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Risk Management In Forex How To Minimize Losses And Maximize Returns

Authors: Eunice Loar

1st Edition

979-8388778864