Question: FINANCIAL MODELING ----------------------------------------------------------------------------------------------------------------- formulae 7. Consider the following boundary value problem in the domain [0,T]R : tF+21x2x22F+x=0F(T,x)=ln(x2) Using the Feynman-Kac stochastic representation formula, find the

FINANCIAL MODELING

-----------------------------------------------------------------------------------------------------------------

formulae

![the domain [0,T]R : tF+21x2x22F+x=0F(T,x)=ln(x2) Using the Feynman-Kac stochastic representation formula, find](https://s3.amazonaws.com/si.experts.images/answers/2024/08/66ac5cee675d3_01466ac5cee0a245.jpg)

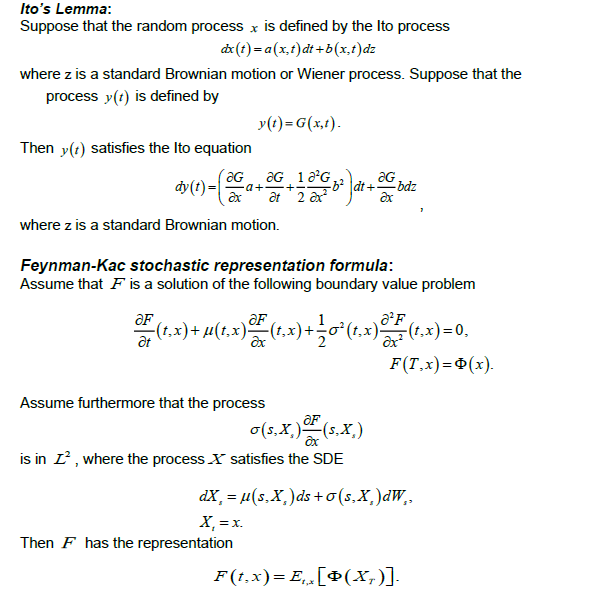

7. Consider the following boundary value problem in the domain [0,T]R : tF+21x2x22F+x=0F(T,x)=ln(x2) Using the Feynman-Kac stochastic representation formula, find the solution of this problem. Formulae: Up-step risk-neutral probability: p=udertd, where u=et+qt;d=et+qt;t=titi1andq=dividendyield. Ito's Lemma: Suppose that the random process x is defined by the lto process dx(t)=a(x,t)dt+b(x,t)dz where z is a standard Brownian motion or Wiener process. Suppose that the process y(t) is defined by y(t)=G(x,t). Then y(t) satisfies the lto equation dy(t)(xGa+tG+21x22Gb2)dt+xGbdz. where z is a standard Brownian motion. Feynman-Kac stochastic representation formula: Assume that F is a solution of the following boundary value problem tF(t,x)+(t,x)xF(t,x)+212(t,x)x22F(t,x)F(T,x)=0,=(x). Assume furthermore that the process (s,X)xF(s,X) is in L2, where the process X satisfies the SDE dXt=(s,Xs)ds+(s,Xa)dWs,Xr=x. Then F has the representation F(t,x)Et,[(Xs)]. Ito's Lemma: Suppose that the random process x is defined by the lto process dx(t)=a(x,t)dt+b(x,t)dz where z is a standard Brownian motion or Wiener process. Suppose that the process y(t) is defined by y(t)=G(x,t). Then y(t) satisfies the Ito equation dy(t)=(xGa+tG+21x22Gb2)dt+xGbdz, where z is a standard Brownian motion. Feynman-Kac stochastic representation formula: Assume that F is a solution of the following boundary value problem tF(t,x)+(t,x)xF(t,x)+212(t,x)x22F(t,x)F(T,x)=0,=(x). Assume furthermore that the process (s,Xs)xF(s,Xs) is in L2, where the process X satisfies the SDE dXs=(s,Xs)ds+(s,Xs)dWs,Xt=x. Then F has the representation F(t,x)=Et,x[(XT)]. 7. Consider the following boundary value problem in the domain [0,T]R : tF+21x2x22F+x=0F(T,x)=ln(x2) Using the Feynman-Kac stochastic representation formula, find the solution of this problem. Formulae: Up-step risk-neutral probability: p=udertd, where u=et+qt;d=et+qt;t=titi1andq=dividendyield. Ito's Lemma: Suppose that the random process x is defined by the lto process dx(t)=a(x,t)dt+b(x,t)dz where z is a standard Brownian motion or Wiener process. Suppose that the process y(t) is defined by y(t)=G(x,t). Then y(t) satisfies the lto equation dy(t)(xGa+tG+21x22Gb2)dt+xGbdz. where z is a standard Brownian motion. Feynman-Kac stochastic representation formula: Assume that F is a solution of the following boundary value problem tF(t,x)+(t,x)xF(t,x)+212(t,x)x22F(t,x)F(T,x)=0,=(x). Assume furthermore that the process (s,X)xF(s,X) is in L2, where the process X satisfies the SDE dXt=(s,Xs)ds+(s,Xa)dWs,Xr=x. Then F has the representation F(t,x)Et,[(Xs)]. Ito's Lemma: Suppose that the random process x is defined by the lto process dx(t)=a(x,t)dt+b(x,t)dz where z is a standard Brownian motion or Wiener process. Suppose that the process y(t) is defined by y(t)=G(x,t). Then y(t) satisfies the Ito equation dy(t)=(xGa+tG+21x22Gb2)dt+xGbdz, where z is a standard Brownian motion. Feynman-Kac stochastic representation formula: Assume that F is a solution of the following boundary value problem tF(t,x)+(t,x)xF(t,x)+212(t,x)x22F(t,x)F(T,x)=0,=(x). Assume furthermore that the process (s,Xs)xF(s,Xs) is in L2, where the process X satisfies the SDE dXs=(s,Xs)ds+(s,Xs)dWs,Xt=x. Then F has the representation F(t,x)=Et,x[(XT)]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts