Find the correct answer of the following problems

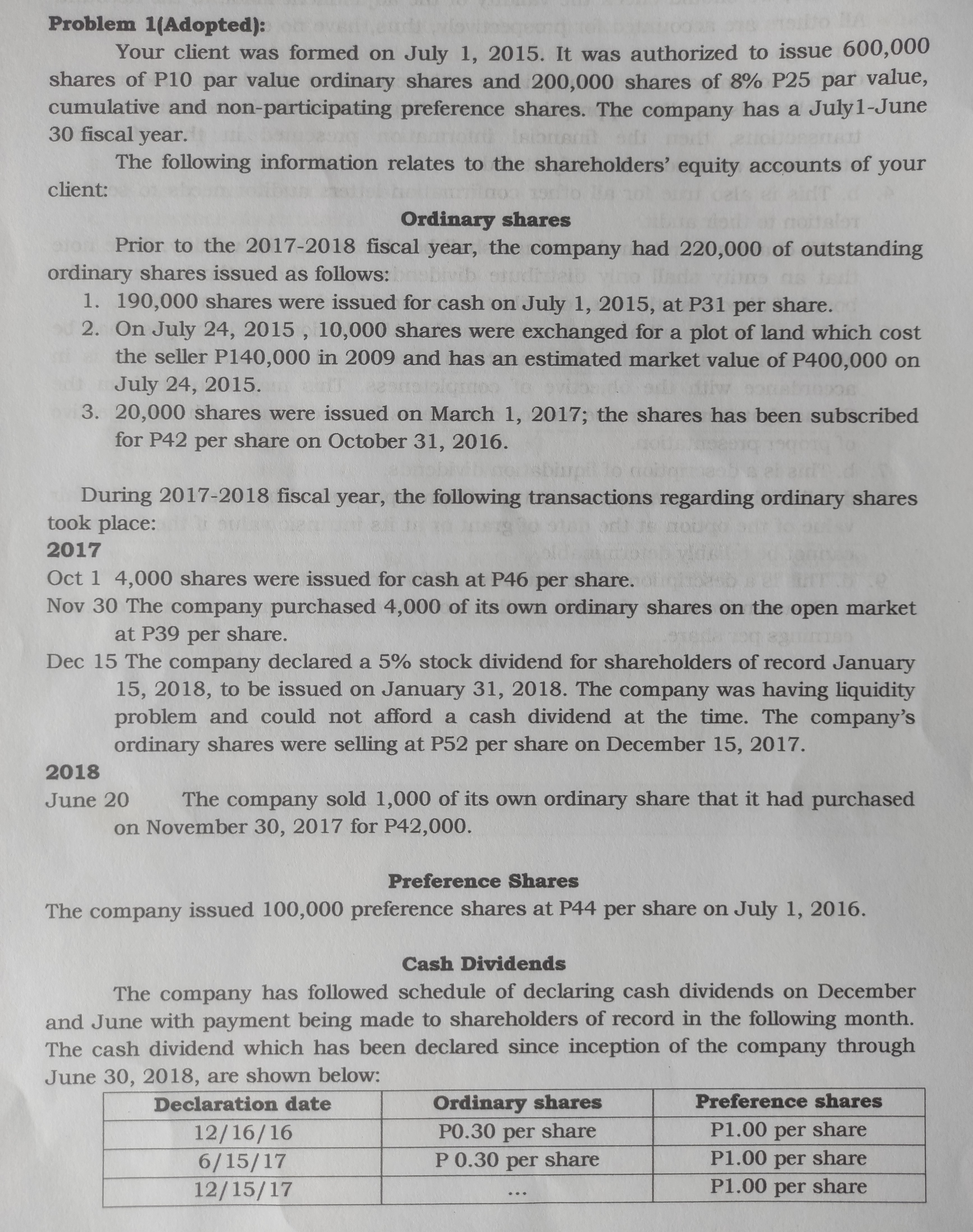

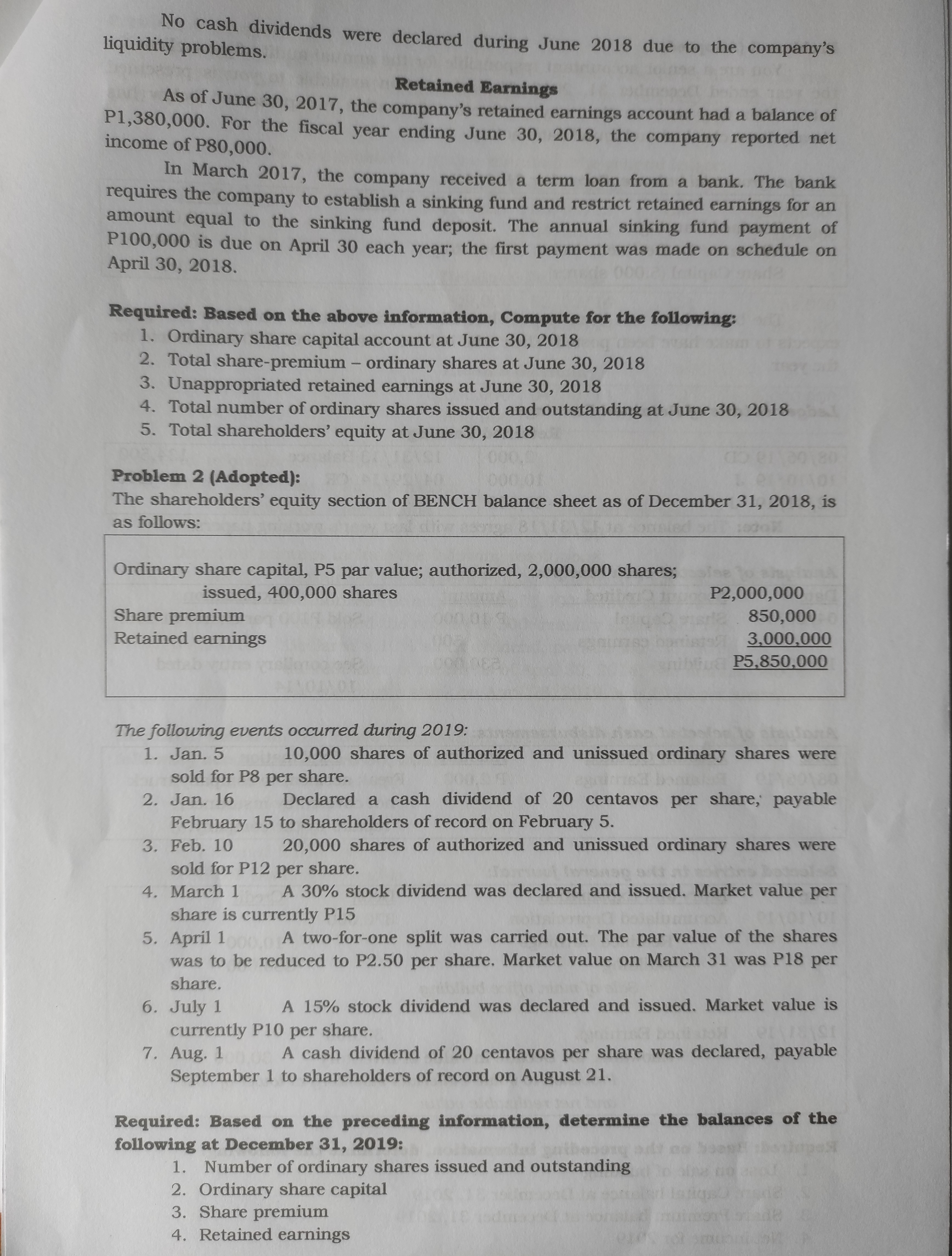

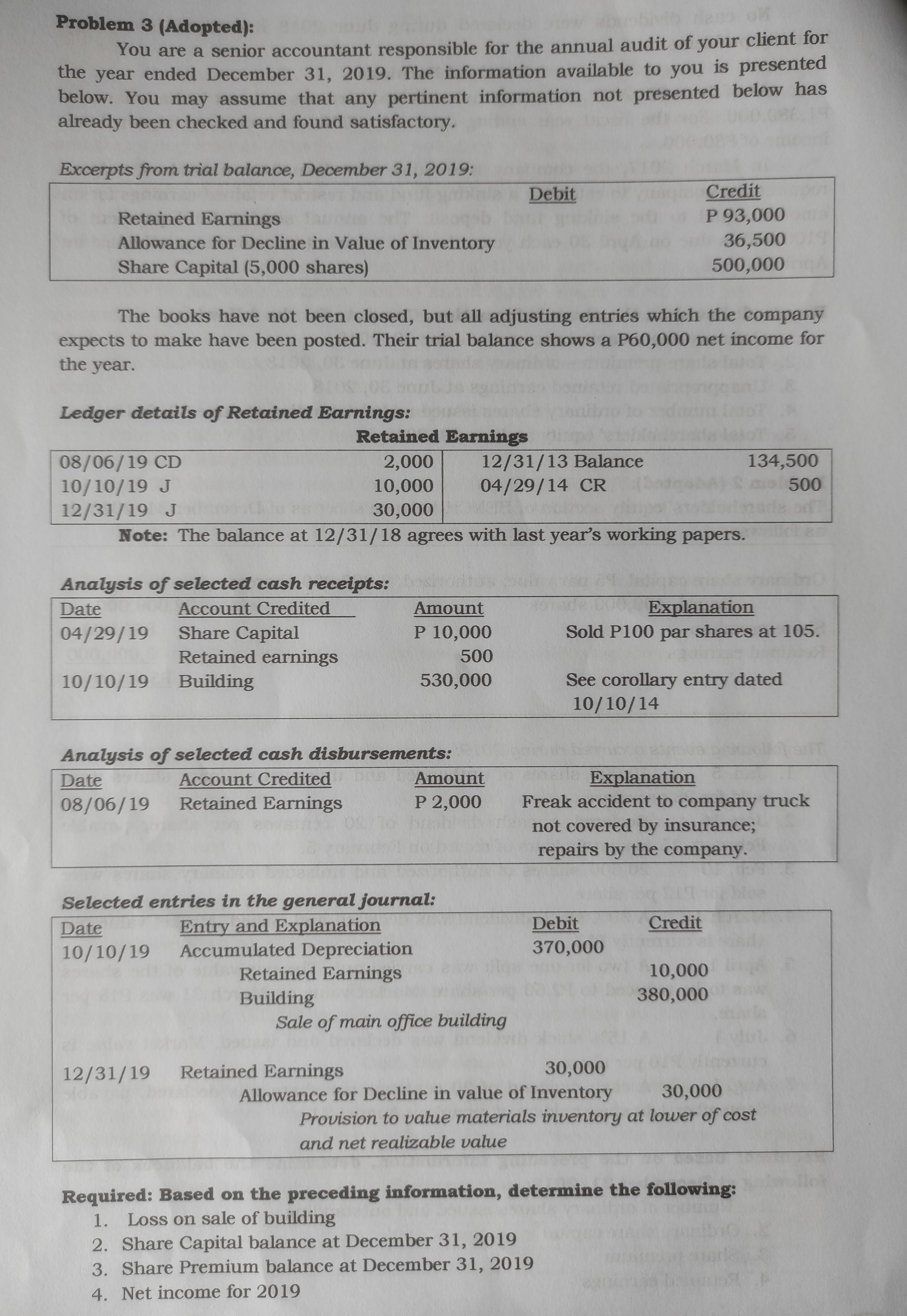

Problem 1(Adopted): Your client was formed on July 1, 2015. It was authorized to issue 600,000 shares of P10 par value ordinary shares and 200,000 shares of 8% P25 par value, cumulative and non-participating preference shares. The company has a July1-June 30 fiscal year. The following information relates to the shareholders' equity accounts of your client: Ordinary shares Prior to the 2017-2018 fiscal year, the company had 220,000 of outstanding ordinary shares issued as follows: 1. 190,000 shares were issued for cash on July 1, 2015, at P31 per share. 2. On July 24, 2015 , 10,000 shares were exchanged for a plot of land which cost the seller P140,000 in 2009 and has an estimated market value of P400,000 on July 24, 2015. 3. 20,000 shares were issued on March 1, 2017; the shares has been subscribed for P42 per share on October 31, 2016. During 2017-2018 fiscal year, the following transactions regarding ordinary shares took place: 2017 Oct 1 4,000 shares were issued for cash at P46 per share. Nov 30 The company purchased 4,000 of its own ordinary shares on the open market at P39 per share. Dec 15 The company declared a 5% stock dividend for shareholders of record January 15, 2018, to be issued on January 31, 2018. The company was having liquidity problem and could not afford a cash dividend at the time. The company's ordinary shares were selling at P52 per share on December 15, 2017. 2018 June 20 The company sold 1,000 of its own ordinary share that it had purchased on November 30, 2017 for P42,000. Preference Shares The company issued 100,000 preference shares at P44 per share on July 1, 2016. Cash Dividends The company has followed schedule of declaring cash dividends on December and June with payment being made to shareholders of record in the following month. The cash dividend which has been declared since inception of the company through June 30, 2018, are shown below: Declaration date Ordinary shares Preference shares 12/16/16 P0.30 per share P1.00 per share 6/15/17 P 0.30 per share P1.00 per share 12/15/17 P1.00 per shareliquidity problems. No cash dividends were declared during June 2018 due to the company's Retained Earnings As of June 30, 2017, the company's retained earnings account had a balance of P1,380,000. For the fiscal year ending June 30, 2018, the company reported net income of P80,000. In March 2017, the company received a term loan from a bank. The bank requires the company to establish a sinking fund and restrict retained earnings for an amount equal to the sinking fund deposit. The annual sinking fund payment of P100,000 is due on April 30 each year; the first payment was made on schedule on April 30, 2018. Required: Based on the above information, Compute for the following: 1. Ordinary share capital account at June 30, 2018 2. Total share-premium - ordinary shares at June 30, 2018 3. Unappropriated retained earnings at June 30, 2018 4. Total number of ordinary shares issued and outstanding at June 30, 2018 5. Total shareholders' equity at June 30, 2018 Problem 2 (Adopted): The shareholders' equity section of BENCH balance sheet as of December 31, 2018, is as follows: Ordinary share capital, P5 par value; authorized, 2,000,000 shares; issued, 400,000 shares P2,000,000 Share premium 850,000 Retained earnings 3,000,000 P5,850,000 The following events occurred during 2019: 1. Jan. 5 10,000 shares of authorized and unissued ordinary shares were sold for P8 per share. 2. Jan. 16 Declared a cash dividend of 20 centavos per share, payable February 15 to shareholders of record on February 5. 3. Feb. 10 20,000 shares of authorized and unissued ordinary shares were sold for P12 per share. 4. March 1 A 30% stock dividend was declared and issued. Market value per share is currently P15 5. April 1 A two-for-one split was carried out. The par value of the shares was to be reduced to P2.50 per share. Market value on March 31 was P18 per share. 6. July 1 A 15% stock dividend was declared and issued. Market value is currently P10 per share. 7. Aug. 1 A cash dividend of 20 centavos per share was declared, payable September 1 to shareholders of record on August 21. Required: Based on the preceding information, determine the balances of the following at December 31, 2019: 1. Number of ordinary shares issued and outstanding 2. Ordinary share capital 3. Share premium 4. Retained earningsProblem 3 (Adopted): You are a senior accountant responsible for the annual audit of your client for the year ended December 31, 2019. The information available to you is presented below. You may assume that any pertinent information not presented below has already been checked and found satisfactory. Excerpts from trial balance, December 31, 2019: Debit Credit Retained Earnings P 93,000 Allowance for Decline in Value of Inventory 36,500 Share Capital (5,000 shares) 500,000 The books have not been closed, but all adjusting entries which the company expects to make have been posted. Their trial balance shows a P60,000 net income for the year. Ledger details of Retained Earnings: Retained Earnings 08/06/ 19 CD 2,000 12/31/13 Balance 134,500 10/10/19 J 10,000 04/29/14 CR 500 12/31/19 J 30,000 Note: The balance at 12/31/18 agrees with last year's working papers. Analysis of selected cash receipts: Date Account Credited Amount Explanation 04/29/19 Share Capital P 10,000 Sold P100 par shares at 105. Retained earnings 500 10/10/19 Building 530,000 See corollary entry dated 10/10/14 Analysis of selected cash disbursements: Date Account Credited Amount Explanation 08/06/19 Retained Earnings P 2,000 Freak accident to company truck not covered by insurance; repairs by the company. Selected entries in the general journal: Date Entry and Explanation Debit Credit 10/10/19 Accumulated Depreciation 370,000 Retained Earnings 10,000 Building 380,000 Sale of main office building 12/31/19 Retained Earnings 30,000 Allowance for Decline in value of Inventory 30,000 Provision to value materials inventory at lower of cost and net realizable value Required: Based on the preceding information, determine the following: 1. Loss on sale of building 2. Share Capital balance at December 31, 2019 3. Share Premium balance at December 31, 2019 4. Net income for 2019Problem 4 (Adopted): You are engaged in the audit a new client, at the close of its first fiscal year, field work. April 30, 2019. The books had been closed prior to the time you began your year-end Shown below are the shareholder's equity accounts in the general ledger: Ordinary Share Capital 09/14/13 CD 110,000 05/01/13 CR 1,200,000 04/28/14 J 109,000 Retained Earnings 04/28/14 J 109,000 02/02/14 CR 52,000 04/30/14 J 800,000 Income Summary 04/30/14 5,200,000 04/30/14 J 6,000,000 04/30/ 14 800,000 Additional information is as follows: A. From the articles of incorporation: blodsauda Int Authorized share capital 30,000 shares Par value per share P100 B. Directors' minutes include the following resolutions: 04/30/13 Authorized the issue of P10,000 shares at P120 per share. 09/13/13 Authorized the acquisition of 1,000 shares at P1 10. 02/01/14 Authorized the reissue of 500 treasury shares at P105. 04 /28/ 14 Declared a 10% stock dividend, payable May 31, 2014, to shareholders of record as of April 30, 2014. The market value of the company's stock on April 28, 2019, was P130 per share. Required: Based on the above information, determine the correct balances of the following accounts on April 30, 2019. 1. Ordinary Share Capital 2. Treasury Shares 3. Share Premium 4. Retained Earnings 5. Stock Dividends Payable