Answered step by step

Verified Expert Solution

Question

1 Approved Answer

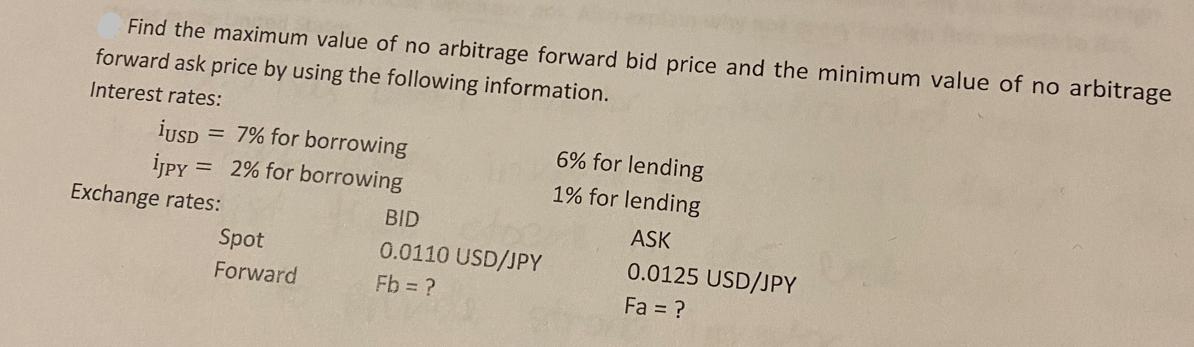

Find the maximum value of no arbitrage forward bid price and the minimum value of no arbitrage forward ask price by using the following

Find the maximum value of no arbitrage forward bid price and the minimum value of no arbitrage forward ask price by using the following information. Interest rates: iUSD = 7% for borrowing iJPY = 2% for borrowing Exchange rates: Spot Forward BID 0.0110 USD/JPY Fb = ? 6% for lending 1% for lending ASK 0.0125 USD/JPY Fa = ?

Step by Step Solution

★★★★★

3.49 Rating (166 Votes )

There are 3 Steps involved in it

Step: 1

9Maximum Fb Spot1Interest Rate100001...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduction to graph theory

Authors: Douglas B. West

2nd edition

131437372, 978-0131437371