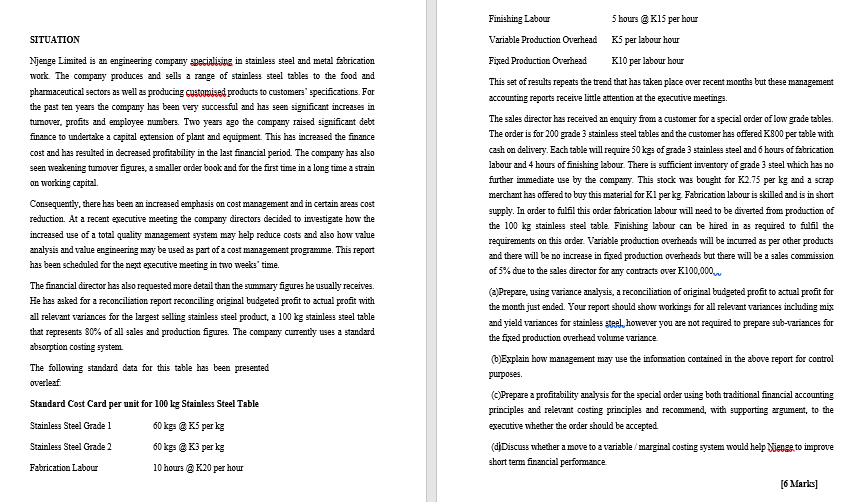

Finishing Labour Variable Production Overhead 5 hours @ K15 per hour K5 per labour hour SITUATION Fixed Production Overhead Kl0 per labour hour This set of results repeats the trend that has taken place over recent months but these management accounting reports receive little attention at the executive meetings. Njenge Limited is an engineering company specializing in stainless steel and metal fabrication work. The company produces and sells a range of stainless steel tables to the food and pharmaceutical sectors as well as producing customised products to customers' specifications. For the past ten years the company has been very successful and has seen significant increases in tumover, profits and employee numbers. Two years ago the company raised significant debt finance to undertake a capital extension of plant and equipment. This has increased the finance cost and has resulted in decreased profitability in the last financial period. The company has also seen weakening tumover figures, a smaller order book and for the first time in a long time a strain on working capital The sales director has received an enquiry from a customer for a special order of low grade tables. The order is for 200 grade 3 stainless steel tables and the customer has offered K800 per table with cash on delivery. Each table will require 50 kgs of grade 3 stainless steel and 6 hours of fabrication labour and 4 hours of finishing labour. There is sufficient inventory of grade 3 steel which has 10 further immediate use by the company. This stock was bought for K2.75 per kg and a scrap merchant has offered to buy this material for Kl per kg Fabrication labour is skilled and is in short supply. In order to fulfil this order fabrication labour will need to be diverted from production of the 100 kg stainless steel table Finishing labour can be hired in as required to fulfil the requirements on this order. Variable production overheads will be incurred as per other products and there will be no increase in fixed production overheads but there will be a sales commission of 5% due to the sales director for any contracts over K100,000 Consequently, there has been an increased emphasis on cost management and in certain areas cost reduction. At a recent executive meeting the company directors decided to investigate how the increased use of a total quality management system may belp reduce costs and also how value analysis and value engineering may be used as part of a cost management programme. This report has been scheduled for the next executive meeting in two weeks' time. The financial director has also requested more detail than the summary figures he usually receives. He has asked for a reconciliation report reconciling original budgeted profit to actual profit with all relevant variances for the largest selling stainless steel product, a 100 kg stainless steel table that represents 30% of all sales and production figures. The company currently uses a standard absorption costing system The following standard data for this table has been presented overleaf (a) Prepare, using variance analysis, a reconciliation of original budgeted profit to actual profit for the month just ended. Your report should show workings for all relevant variances including mix and yield variances for stainless steel however you are not required to prepare sub-variances for the fixed production overhead volume variance. (6) Explain how management may use the information contained in the above report for control purposes. (c)Prepare a profitability analysis for the special order using both traditional financial accounting principles and relevant costing principles and recommend, with supporting argument, to the executive whether the order should be accepted Standard Cost Card per unit for 100 leg Stainless Steel Table Stainless Steel Grade 1 60 kgs @ K5 per kg Stainless Steel Grade 2 60 kgs @k3 per kg Fabrication Labour 10 how: @K20 per hour (d) Discuss whether a move to a variable / marginal costing system would help Nieuze to improve short term financial performance [6 Marks] Finishing Labour Variable Production Overhead 5 hours @ K15 per hour K5 per labour hour SITUATION Fixed Production Overhead Kl0 per labour hour This set of results repeats the trend that has taken place over recent months but these management accounting reports receive little attention at the executive meetings. Njenge Limited is an engineering company specializing in stainless steel and metal fabrication work. The company produces and sells a range of stainless steel tables to the food and pharmaceutical sectors as well as producing customised products to customers' specifications. For the past ten years the company has been very successful and has seen significant increases in tumover, profits and employee numbers. Two years ago the company raised significant debt finance to undertake a capital extension of plant and equipment. This has increased the finance cost and has resulted in decreased profitability in the last financial period. The company has also seen weakening tumover figures, a smaller order book and for the first time in a long time a strain on working capital The sales director has received an enquiry from a customer for a special order of low grade tables. The order is for 200 grade 3 stainless steel tables and the customer has offered K800 per table with cash on delivery. Each table will require 50 kgs of grade 3 stainless steel and 6 hours of fabrication labour and 4 hours of finishing labour. There is sufficient inventory of grade 3 steel which has 10 further immediate use by the company. This stock was bought for K2.75 per kg and a scrap merchant has offered to buy this material for Kl per kg Fabrication labour is skilled and is in short supply. In order to fulfil this order fabrication labour will need to be diverted from production of the 100 kg stainless steel table Finishing labour can be hired in as required to fulfil the requirements on this order. Variable production overheads will be incurred as per other products and there will be no increase in fixed production overheads but there will be a sales commission of 5% due to the sales director for any contracts over K100,000 Consequently, there has been an increased emphasis on cost management and in certain areas cost reduction. At a recent executive meeting the company directors decided to investigate how the increased use of a total quality management system may belp reduce costs and also how value analysis and value engineering may be used as part of a cost management programme. This report has been scheduled for the next executive meeting in two weeks' time. The financial director has also requested more detail than the summary figures he usually receives. He has asked for a reconciliation report reconciling original budgeted profit to actual profit with all relevant variances for the largest selling stainless steel product, a 100 kg stainless steel table that represents 30% of all sales and production figures. The company currently uses a standard absorption costing system The following standard data for this table has been presented overleaf (a) Prepare, using variance analysis, a reconciliation of original budgeted profit to actual profit for the month just ended. Your report should show workings for all relevant variances including mix and yield variances for stainless steel however you are not required to prepare sub-variances for the fixed production overhead volume variance. (6) Explain how management may use the information contained in the above report for control purposes. (c)Prepare a profitability analysis for the special order using both traditional financial accounting principles and relevant costing principles and recommend, with supporting argument, to the executive whether the order should be accepted Standard Cost Card per unit for 100 leg Stainless Steel Table Stainless Steel Grade 1 60 kgs @ K5 per kg Stainless Steel Grade 2 60 kgs @k3 per kg Fabrication Labour 10 how: @K20 per hour (d) Discuss whether a move to a variable / marginal costing system would help Nieuze to improve short term financial performance [6 Marks]