Answered step by step

Verified Expert Solution

Question

1 Approved Answer

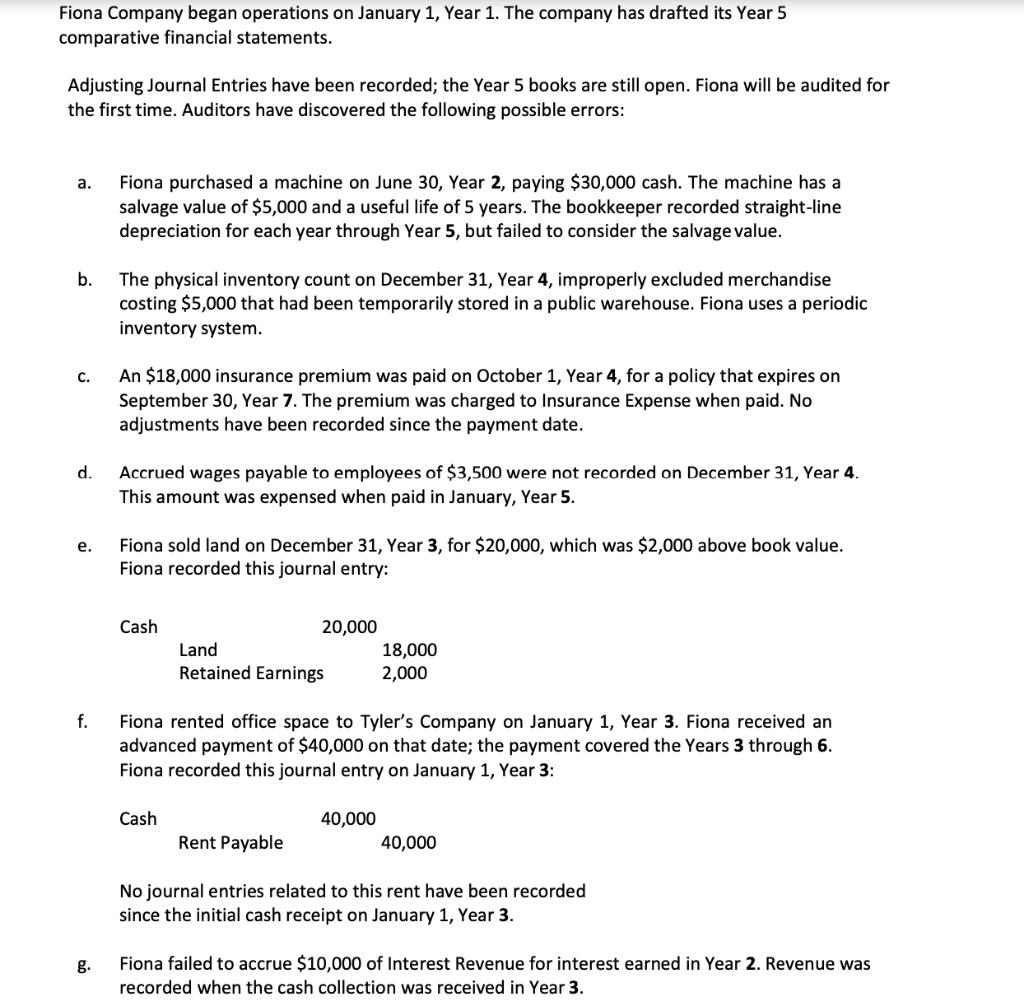

Fiona Company began operations on January 1, Year 1. The company has drafted its Year 5 comparative financial statements. Adjusting Journal Entries have been

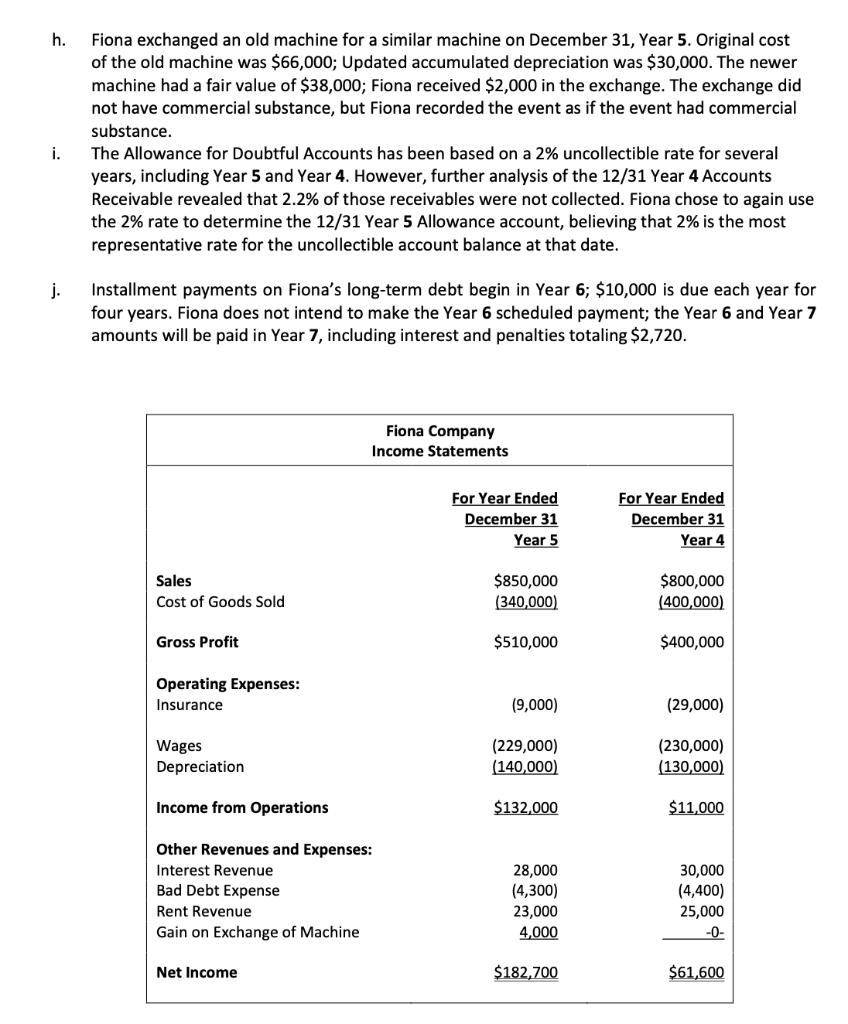

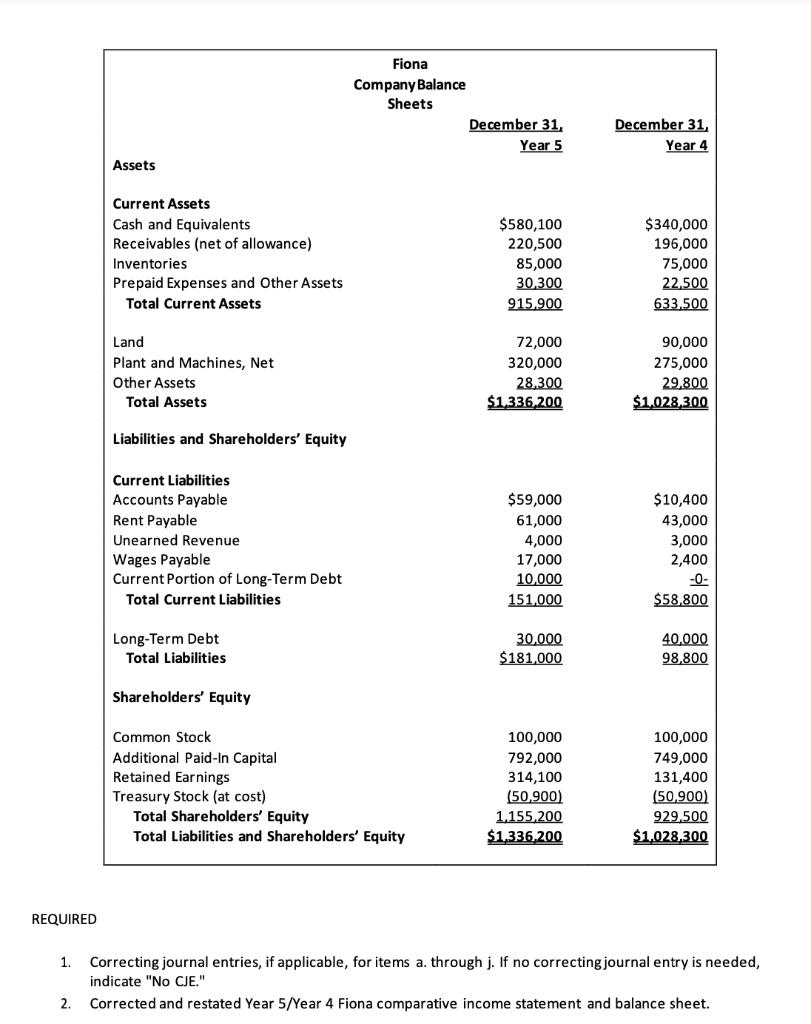

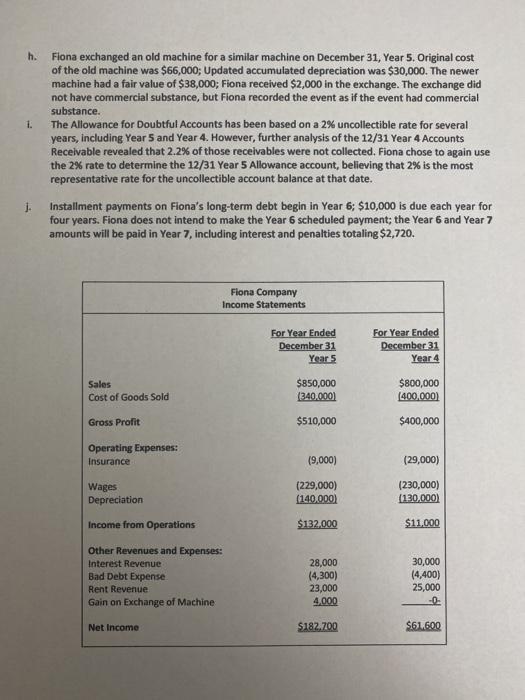

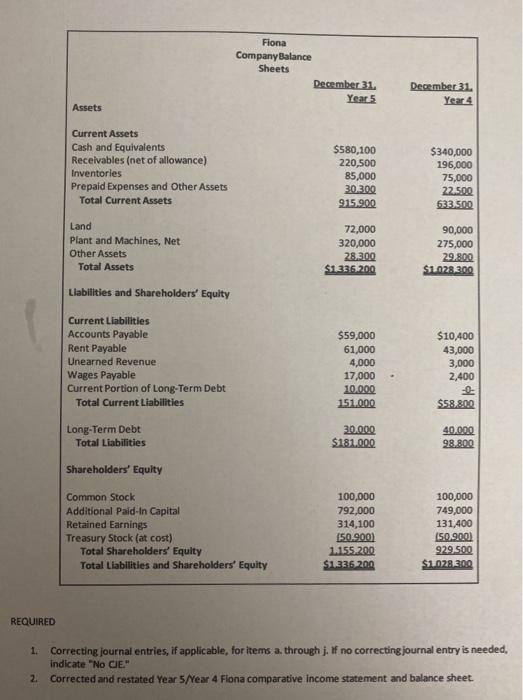

Fiona Company began operations on January 1, Year 1. The company has drafted its Year 5 comparative financial statements. Adjusting Journal Entries have been recorded; the Year 5 books are still open. Fiona will be audited for the first time. Auditors have discovered the following possible errors: a. b. C. d. e. f. g. Fiona purchased a machine on June 30, Year 2, paying $30,000 cash. The machine has a salvage value of $5,000 and a useful life of 5 years. The bookkeeper recorded straight-line depreciation for each year through Year 5, but failed to consider the salvage value. The physical inventory count on December 31, Year 4, improperly excluded merchandise costing $5,000 that had been temporarily stored in a public warehouse. Fiona uses a periodic inventory system. An $18,000 insurance premium was paid on October 1, Year 4, for a policy that expires on September 30, Year 7. The premium was charged to Insurance Expense when paid. No adjustments have been recorded since the payment date. Accrued wages payable to employees of $3,500 were not recorded on December 31, Year 4. This amount was expensed when paid in January, Year 5. Fiona sold land on December 31, Year 3, for $20,000, which was $2,000 above book value. Fiona recorded this journal entry: Cash 20,000 Cash Land Retained Earnings Fiona rented office space to Tyler's Company on January 1, Year 3. Fiona received an advanced payment of $40,000 on that date; the payment covered the Years 3 through 6. Fiona recorded this journal entry on January 1, Year 3: 18,000 2,000 40,000 Rent Payable No journal entries related to this rent have been recorded since the initial cash receipt on January 1, Year 3. 40,000 Fiona failed to accrue $10,000 of Interest Revenue for interest earned in Year 2. Revenue was recorded when the cash collection was received in Year 3. h. i. j. Fiona exchanged an old machine for a similar machine on December 31, Year 5. Original cost of the old machine was $66,000; Updated accumulated depreciation was $30,000. The newer machine had a fair value of $38,000; Fiona received $2,000 in the exchange. The exchange did not have commercial substance, but Fiona recorded the event as if the event had commercial substance. The Allowance for Doubtful Accounts has been based on a 2% uncollectible rate for several years, including Year 5 and Year 4. However, further analysis of the 12/31 Year 4 Accounts Receivable revealed that 2.2% of those receivables were not collected. Fiona chose to again use the 2% rate to determine the 12/31 Year 5 Allowance account, believing that 2% is the most representative rate for the uncollectible account balance at that date. Installment payments on Fiona's long-term debt begin in Year 6; $10,000 is due each year for four years. Fiona does not intend to make the Year 6 scheduled payment; the Year 6 and Year 7 amounts will be paid in Year 7, including interest and penalties totaling $2,720. Sales Cost of Goods Sold Gross Profit Operating Expenses: Insurance Wages Depreciation Income from Operations Other Revenues and Expenses: Interest Revenue Bad Debt Expense Rent Revenue Gain on Exchange of Machine Fiona Company Income Statements Net Income For Year Ended December 31 Year 5 $850,000 (340,000) $510,000 (9,000) (229,000) (140,000) $132,000 28,000 (4,300) 23,000 4,000 $182,700 For Year Ended December 31 Year 4 $800,000 (400,000) $400,000 (29,000) (230,000) (130,000) $11,000 30,000 (4,400) 25,000 -0- $61,600 REQUIRED Assets 2. Current Assets Cash and Equivalents Receivables (net of allowance) Inventories Prepaid Expenses and Other Assets Total Current Assets Land Plant and Machines, Net Other Assets Total Assets Liabilities and Shareholders' Equity Current Liabilities Accounts Payable Rent Payable Unearned Revenue Wages Payable Current Portion of Long-Term Debt Total Current Liabilities Long-Term Debt Total Liabilities Shareholders' Equity Common Stock Additional Paid-In Capital Retained Earnings. Treasury Stock (at cost) Fiona Company Balance Sheets Total Shareholders' Equity Total Liabilities and Shareholders' Equity December 31, Year 5 $580,100 220,500 85,000 30,300 915,900 72,000 320,000 28,300 $1,336,200 $59,000 61,000 4,000 17,000 10,000 151,000 30,000 $181,000 100,000 792,000 314,100 (50,900) 1,155,200 $1,336,200 December 31, Year 4 $340,000 196,000 75,000 22,500 633,500 90,000 275,000 29,800 $1,028,300 $10,400 43,000 3,000 2,400 -0- $58,800 40,000 98,800 100,000 749,000 131,400 (50,900) 929,500 $1,028,300 1. Correcting journal entries, if applicable, for items a. through j. If no correcting journal entry is needed, indicate "No CJE." Corrected and restated Year 5/Year 4 Fiona comparative income statement and balance sheet. Fiona Company began operations on January 1, Year 1. The company has drafted its Year 5 comparative financial statements. Adjusting Journal Entries have been recorded; the Year 5 books are still open. Fiona will be audited for the first time. Auditors have discovered the following possible errors: a. b. The physical inventory count on December 31, Year 4, improperly excluded merchandise costing $5,000 that had been temporarily stored in a public warehouse. Fiona uses a periodic inventory system. C. d. e. Fiona purchased a machine on June 30, Year 2, paying $30,000 cash. The machine has a salvage value of $5,000 and a useful life of 5 years. The bookkeeper recorded straight-line depreciation for each year through Year 5, but failed to consider the salvage value. g. An $18,000 insurance premium was paid on October 1, Year 4, for a policy that expires on September 30, Year 7. The premium was charged to Insurance Expense when paid. No adjustments have been recorded since the payment date. Accrued wages payable to employees of $3,500 were not recorded on December 31, Year 4. This amount was expensed when paid in January, Year 5. Fiona sold land on December 31, Year 3, for $20,000, which was $2,000 above book value. Fiona recorded this journal entry: Cash 20,000 Cash Land Retained Earnings f. Fiona rented office space to Tyler's Company on January 1, Year 3. Fiona received an advanced payment of $40,000 on that date; the payment covered the Years 3 through 6. Fiona recorded this journal entry on January 1, Year 3: 18,000 2,000 40,000 Rent Payable No journal entries related to this rent have been recorded since the initial cash receipt on January 1, Year 3. 40,000 Fiona failed to accrue $10,000 of Interest Revenue for interest earned in Year 2. Revenue was recorded when the cash collection was received in Year 3. h. Fiona exchanged an old machine for a similar machine on December 31, Year 5. Original cost of the old machine was $66,000; Updated accumulated depreciation was $30,000. The newer machine had a fair value of $38,000; Fiona received $2,000 in the exchange. The exchange did not have commercial substance, but Fiona recorded the event as if the event had commercial substance. 1. The Allowance for Doubtful Accounts has been based on a 2% uncollectible rate for several years, including Year 5 and Year 4. However, further analysis of the 12/31 Year 4 Accounts Receivable revealed that 2.2% of those receivables were not collected. Fiona chose to again use the 2% rate to determine the 12/31 Year 5 Allowance account, believing that 2% is the most representative rate for the uncollectible account balance at that date. j. Installment payments on Fiona's long-term debt begin in Year 6; $10,000 is due each year for four years. Fiona does not intend to make the Year 6 scheduled payment; the Year 6 and Year 7 amounts will be paid in Year 7, including interest and penalties totaling $2,720. Sales Cost of Goods Sold Gross Profit Operating Expenses: Insurance Fiona Company Income Statements Wages Depreciation Income from Operations Other Revenues and Expenses: Interest Revenue Bad Debt Expense Rent Revenue Gain on Exchange of Machine Net Income For Year Ended December 31 Year 5 $850,000 (340,000) $510,000 (9,000) (229,000) (140,000) $132,000 28,000 (4,300) 23,000 4,000 $182.700 For Year Ended December 31 Year 4 $800,000 (400,000) $400,000 (29,000) (230,000) (130,000) $11,000 30,000 (4,400) 25,000 $61.600 REQUIRED Assets Current Assets Cash and Equivalents Receivables (net of allowance) Inventories Prepaid Expenses and Other Assets Total Current Assets Land Plant and Machines, Net Other Assets Total Assets Liabilities and Shareholders' Equity Current Liabilities Accounts Payable Rent Payable Unearned Revenue Wages Payable Current Portion of Long-Term Debt Total Current Liabilities Long-Term Debt Total Liabilities Shareholders' Equity Common Stock Additional Paid-In Capital Retained Earnings Treasury Stock (at cost) Fiona Company Balance Sheets Total Shareholders' Equity Total Liabilities and Shareholders' Equity December 31. Year 5 $580,100 220,500 85,000 30.300 915.900 72,000 320,000 28.300 $1.336.200 $59,000 61,000 4,000 17,000 10.000 151.000 30.000 $181.000 100,000 792,000 314,100 (50.900) 1.155.200 $1.336.200 December 31. Year 4 $340,000 196,000 75,000 22.500 633.500 90,000 275,000 29.800 $1.028.300 $10,400 43,000 3,000 2,400 -0- $58.800 40,000 98.800 100,000 749,000 131,400 (50.900) 929.500 $1.028.300 1. Correcting journal entries, if applicable, for items a. through j. If no correcting journal entry is needed, indicate "No CIE." 2. Corrected and restated Year 5/Year 4 Fiona comparative income statement and balance sheet.

Step by Step Solution

★★★★★

3.55 Rating (155 Votes )

There are 3 Steps involved in it

Step: 1

Based on the provided information we will address each of the possible errors a through j listed in the document and provide the necessary correcting journal entries if applicable Lets go through each ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Accounting

Authors: Ray H. Garrison, Eric W. Noreen, Peter C. Brewer

13th Edition

978-0073379616, 73379611, 978-0697789938