Question

FIRST I WILL PROVIDE MY QUESTION WITH ITS DATA, THEN I WILL PROVIDE AN EXAMPLE OF HOW ITS SUPPOSE TO BE DONE UNDERNEATH TO ASSIST

FIRST I WILL PROVIDE MY QUESTION WITH ITS DATA, THEN I WILL PROVIDE AN EXAMPLE OF HOW ITS SUPPOSE TO BE DONE UNDERNEATH TO ASSIST YOU

My question:

Euro/Japanese Yen.

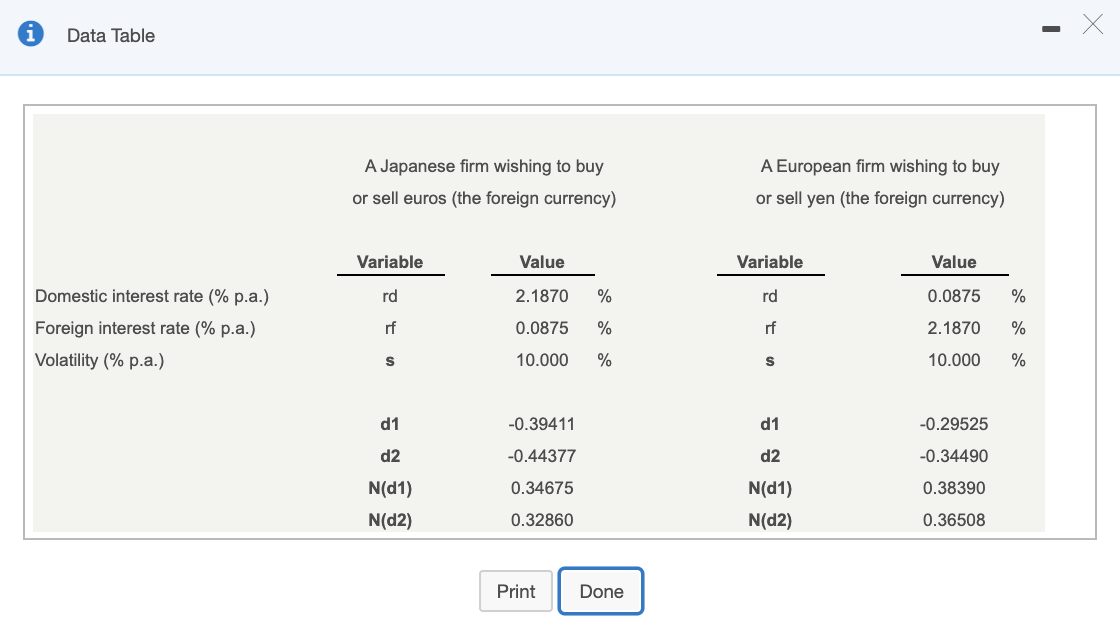

A French firm is expecting to receive 10.4 million in 90 days as a result of an export sale to a Japanese semiconductor firm. What will it cost, in total, to purchase an option to sell the yen at 0.0072/? (See table for initial values.)

The cost, in total, to purchase an option to sell the yen at 0.0072/JPY is ____________/. (Round to the nearest cent.) --> please make answer clear

The cost, in total, to purchase an option to sell the yen at 0.0072/JPY is ____________/. (Round to the nearest cent.) --> please make answer clear

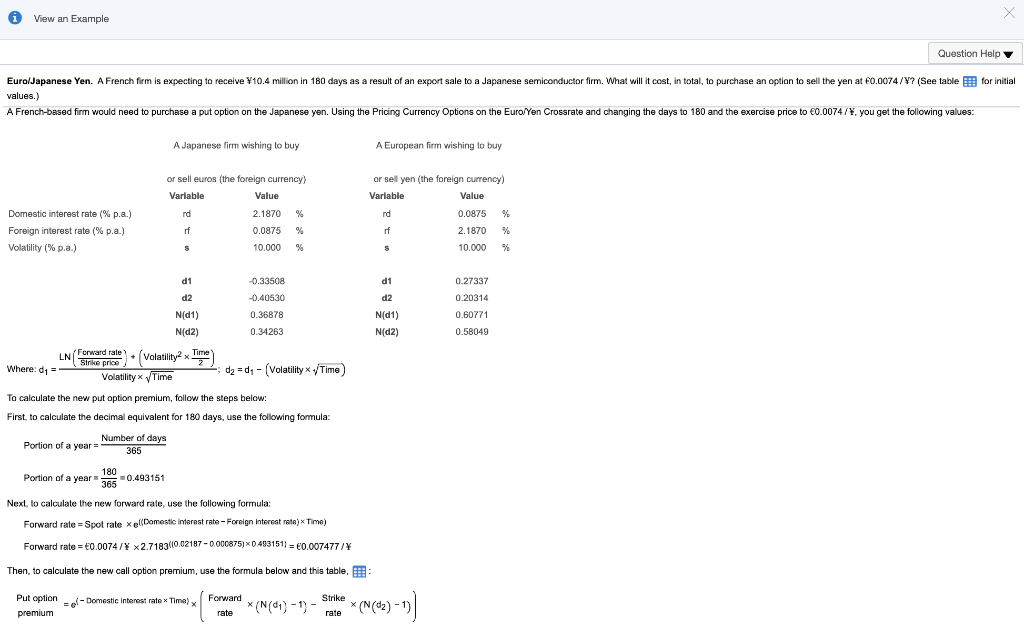

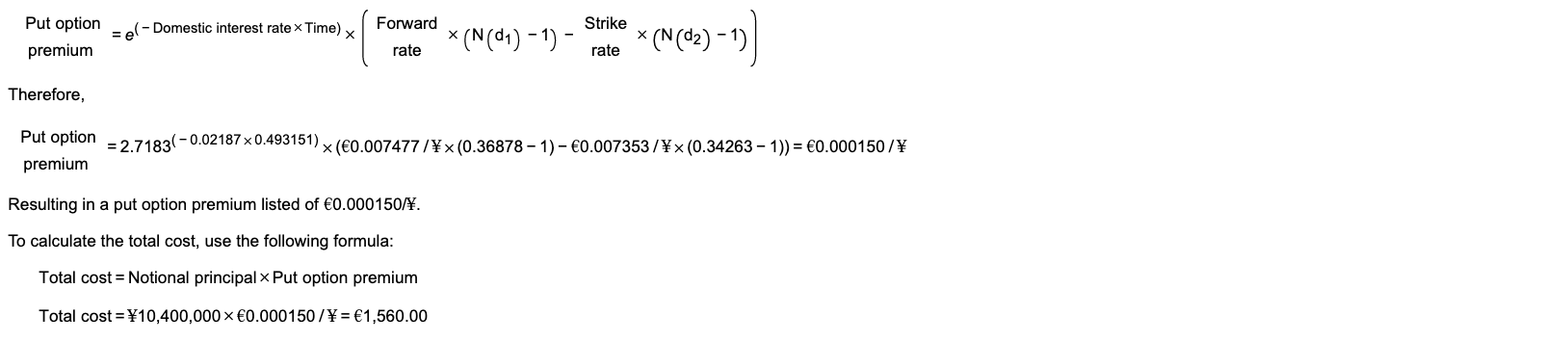

An Example:

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managing Currency Options In Financial Institutions

Authors: Yat-Fai Lam, Kin-Keung Lai

1st Edition

1138778052, 978-1138778054