Answered step by step

Verified Expert Solution

Question

1 Approved Answer

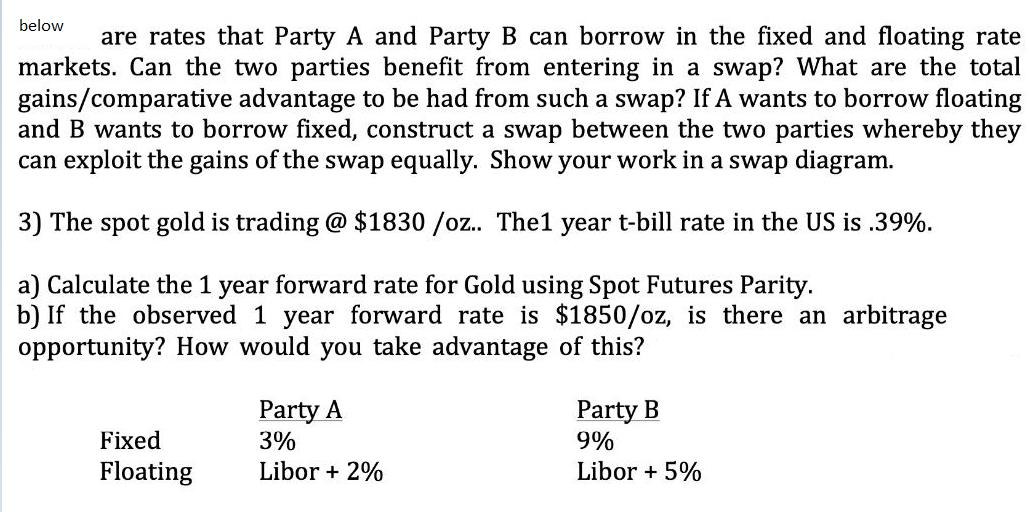

below are rates that Party A and Party B can borrow in the fixed and floating rate markets. Can the two parties benefit from

below are rates that Party A and Party B can borrow in the fixed and floating rate markets. Can the two parties benefit from entering in a swap? What are the total gains/comparative advantage to be had from such a swap? If A wants to borrow floating and B wants to borrow fixed, construct a swap between the two parties whereby they can exploit the gains of the swap equally. Show your work in a swap diagram. 3) The spot gold is trading @ $1830 /oz.. The1 year t-bill rate in the US is .39%. a) Calculate the 1 year forward rate for Gold using Spot Futures Parity. b) If the observed 1 year forward rate is $1850/oz, is there an arbitrage opportunity? How would you take advantage of this? Fixed Floating Party A 3% Libor + 2% Party B 9% Libor + 5%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

ANSWER AND EXPLANATION Refer to image Yes both party can b...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Institutions Management A Risk Management Approach

Authors: Marcia Cornett, Patricia McGraw, Anthony Saunders

8th edition

978-0078034800, 78034809, 978-0071051590