Answered step by step

Verified Expert Solution

Question

1 Approved Answer

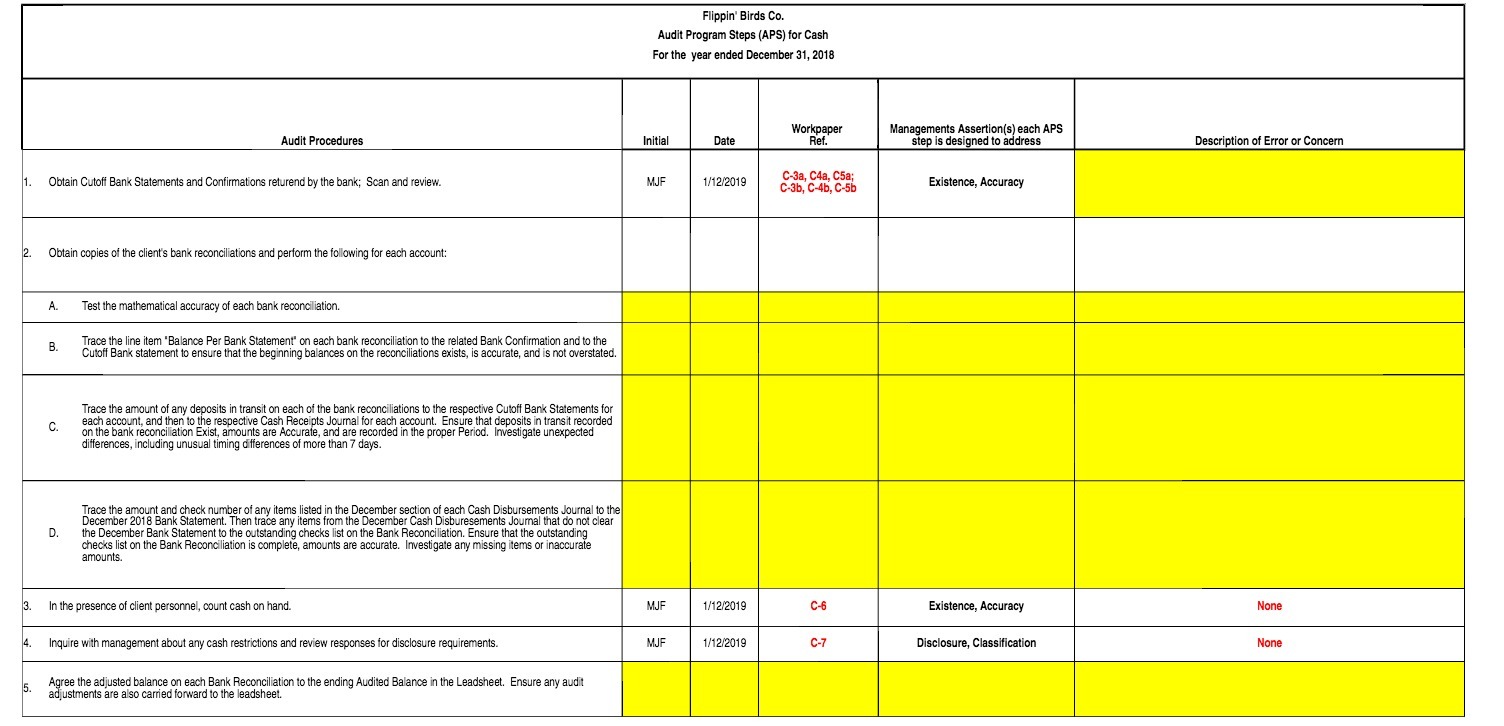

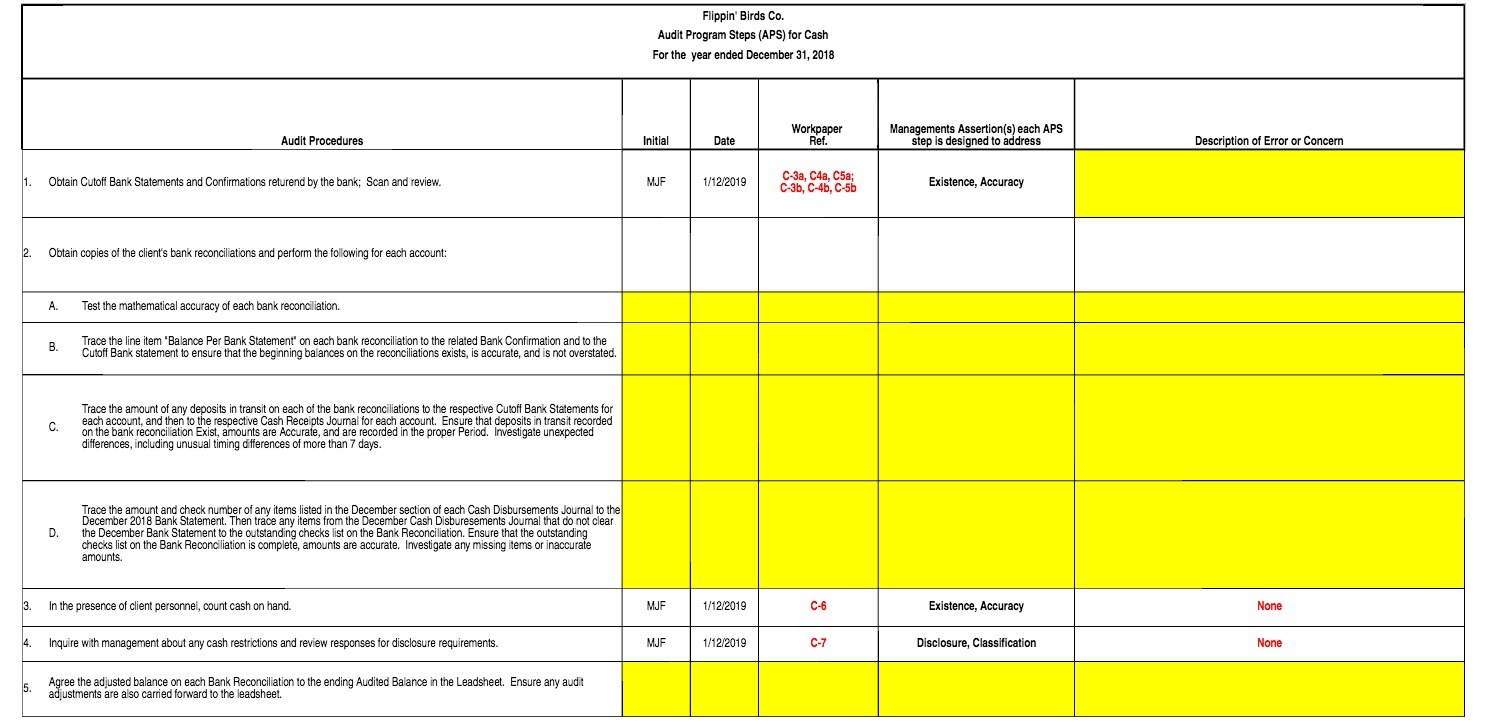

Flippin' Birds Co. Audit Program Steps (APS) for Cash For the year ended December 31, 2018 Workpaper Managements Assertion(s) each APS Audit Procedures Initial Date

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Advanced Accounting

Authors: Debra JeterJames Reeve, Jonathan Duchac, Horace Brock, Paul Chaney

4th Edition

0470506989, 978-0470506981