Answered step by step

Verified Expert Solution

Question

1 Approved Answer

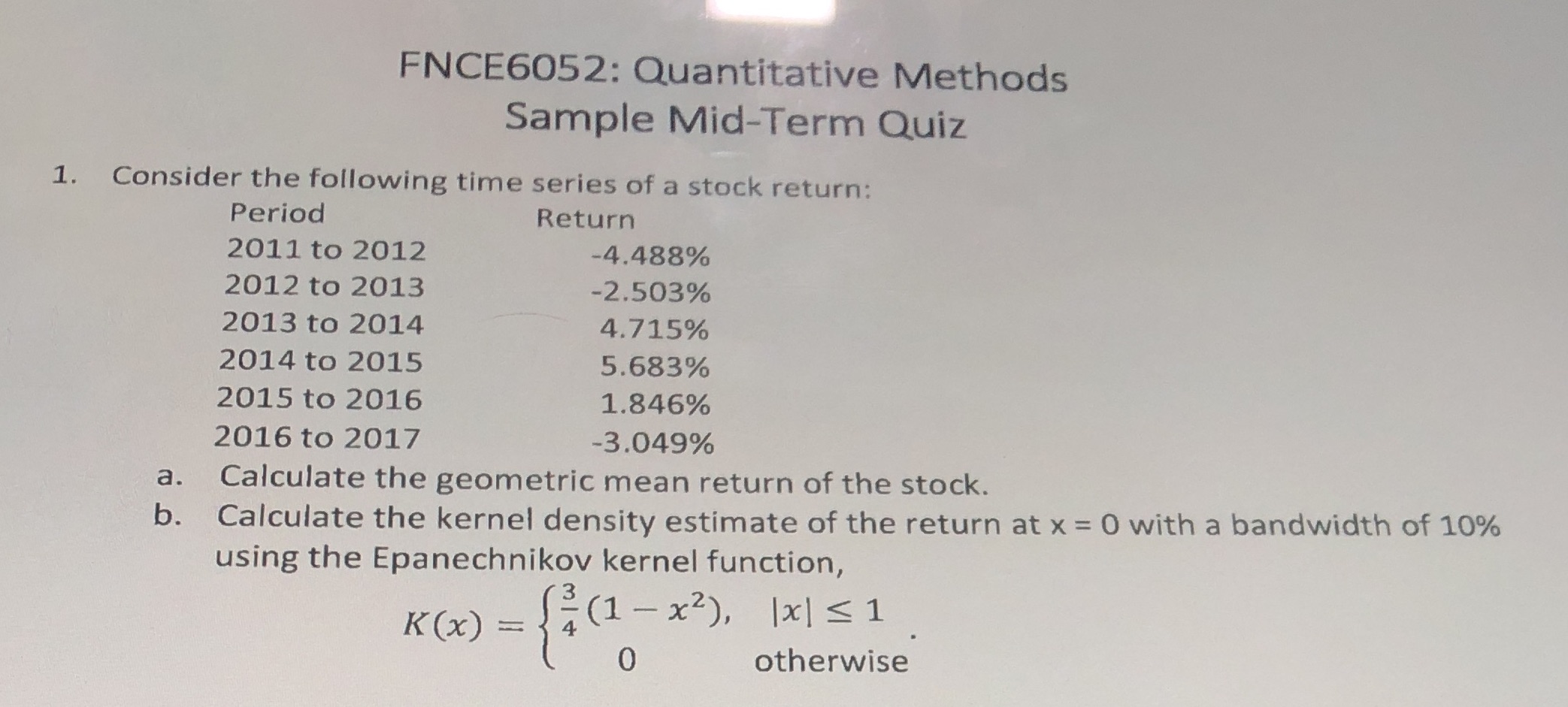

FNCE6052: Quantitative Methods Sample Mid-Term Quiz 1. Consider the following time series of a stock return: Period 2011 to 2012 2012 to 2013 2013

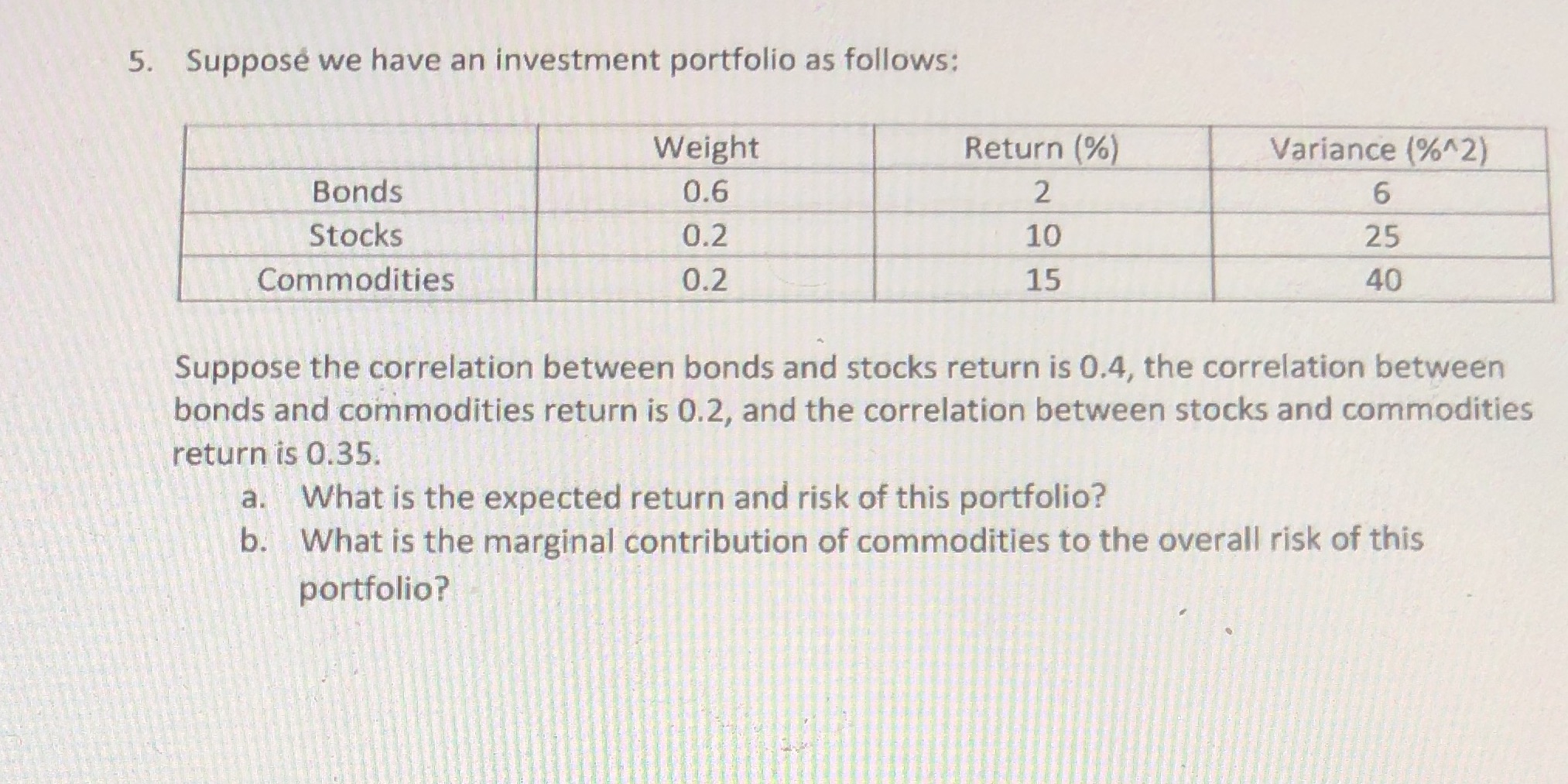

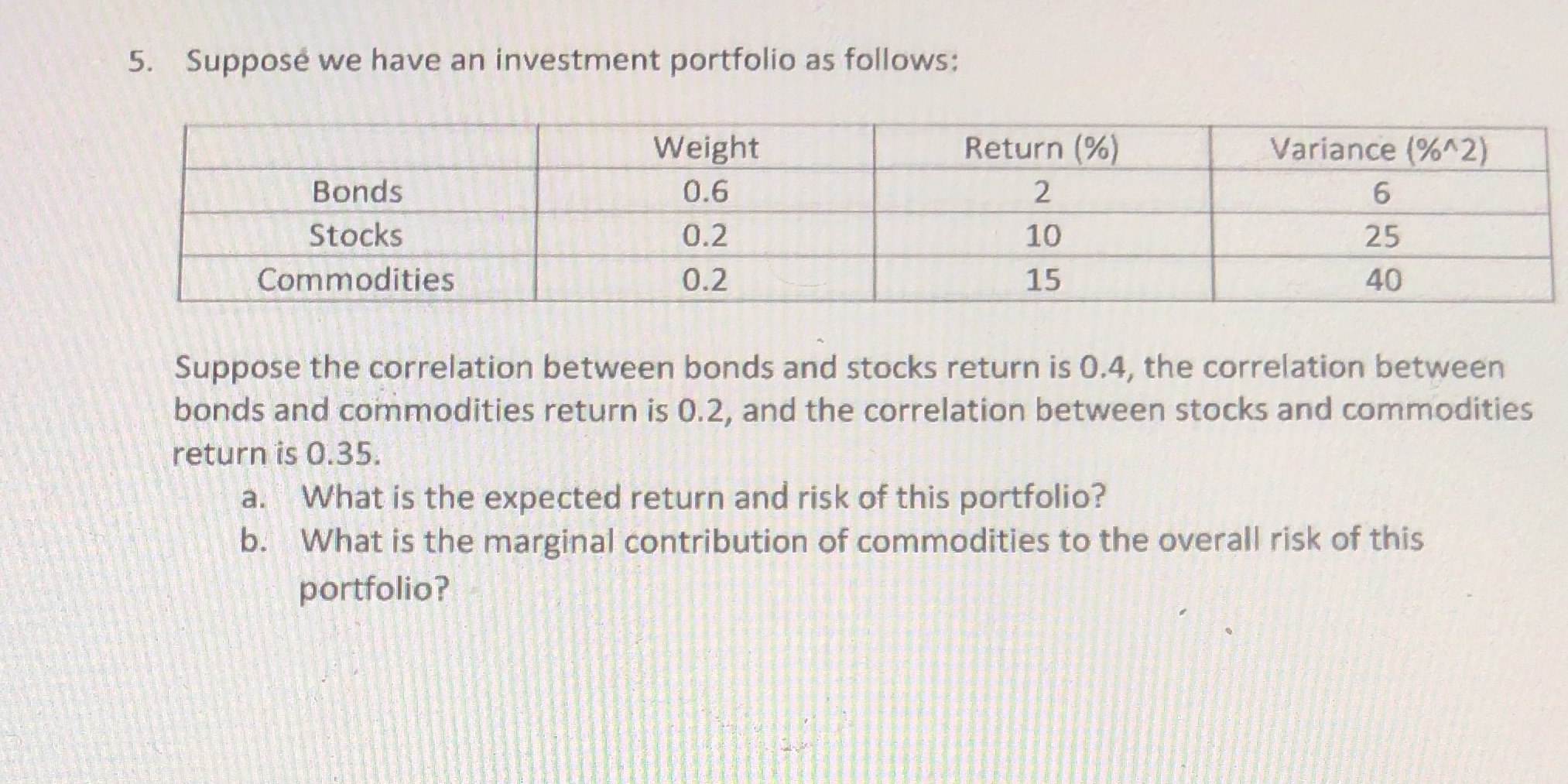

FNCE6052: Quantitative Methods Sample Mid-Term Quiz 1. Consider the following time series of a stock return: Period 2011 to 2012 2012 to 2013 2013 to 2014 2014 to 2015 2015 to 2016 2016 to 2017 a. Return -4.488% -2.503% 4.715% 5.683% 1.846% -3.049% Calculate the geometric mean return of the stock. b. Calculate the kernel density estimate of the return at x = 0 with a bandwidth of 10% using the Epanechnikov kernel function, (1-x), |x| 1 K(x) = 0 otherwise 5. Suppose we have an investment portfolio as follows: Bonds Stocks Commodities Weight 0.6 0.2 0.2 Return (%) 2 Variance (%^2) 6 10 25 15 40 Suppose the correlation between bonds and stocks return is 0.4, the correlation between bonds and commodities return is 0.2, and the correlation between stocks and commodities return is 0.35. a. What is the expected return and risk of this portfolio? b. What is the marginal contribution of commodities to the overall risk of this portfolio? 5. Suppose we have an investment portfolio as follows: Bonds Stocks Commodities Weight 0.6 0.2 0.2 Return (%) 2 Variance (%^2) 6 10 25 15 40 Suppose the correlation between bonds and stocks return is 0.4, the correlation between bonds and commodities return is 0.2, and the correlation between stocks and commodities return is 0.35. a. What is the expected return and risk of this portfolio? b. What is the marginal contribution of commodities to the overall risk of this portfolio?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Venture capital and the finance of innovation

Authors: Andrew Metrick

2nd Edition

9781118137888, 470454709, 1118137884, 978-0470454701