Answered step by step

Verified Expert Solution

Question

1 Approved Answer

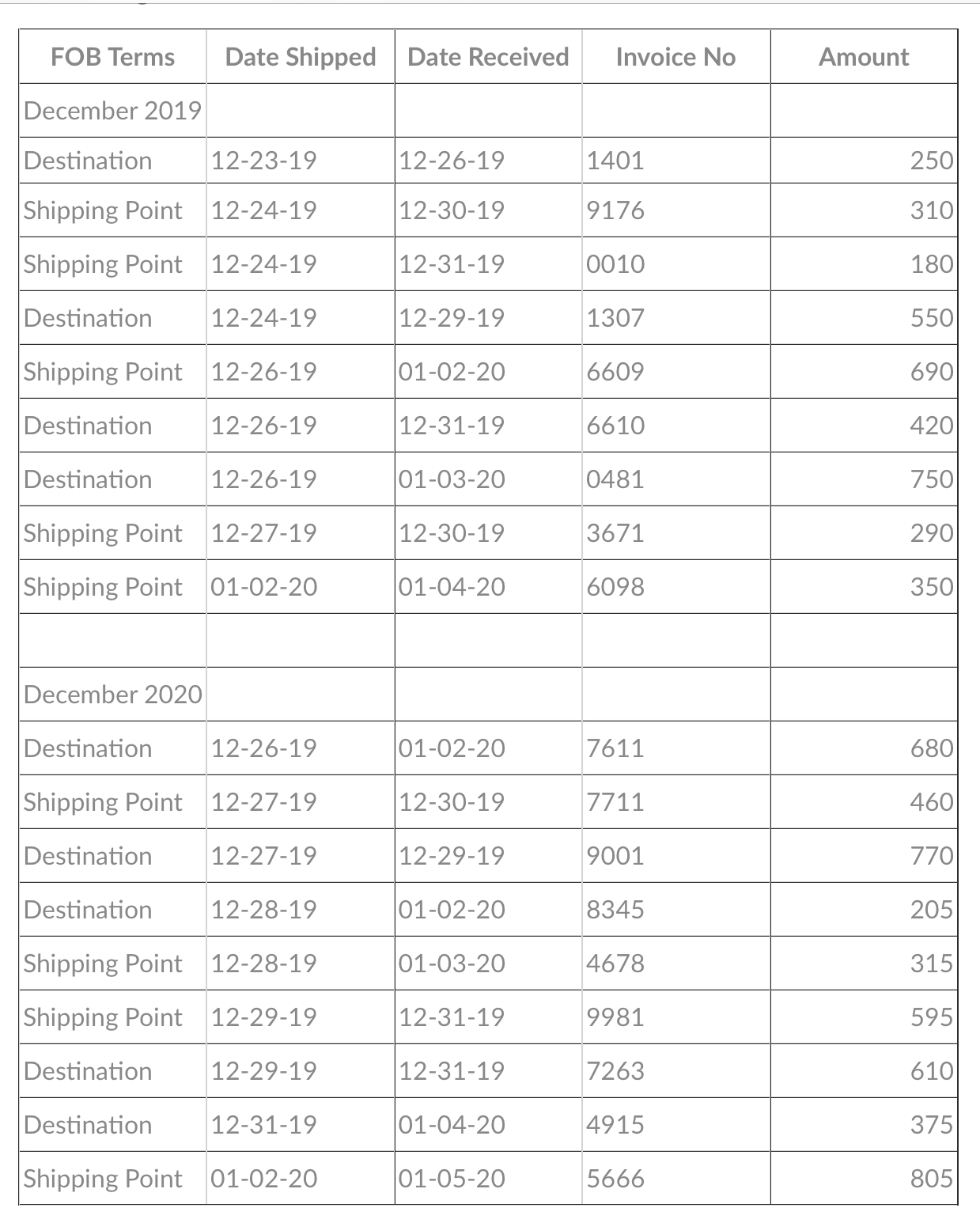

FOB Terms Date Shipped Date Received Invoice No Amount December 2019 Destination 12-23-19 12-26-19 1401 250 Shipping Point 12-24-19 12-30-19 9176 310 Shipping Point 12-24-19

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Using Microsoft Excel And Access 2013 For Accounting

Authors: Glenn Owen

4th Edition

1305161858, 9781305161856