Answered step by step

Verified Expert Solution

Question

1 Approved Answer

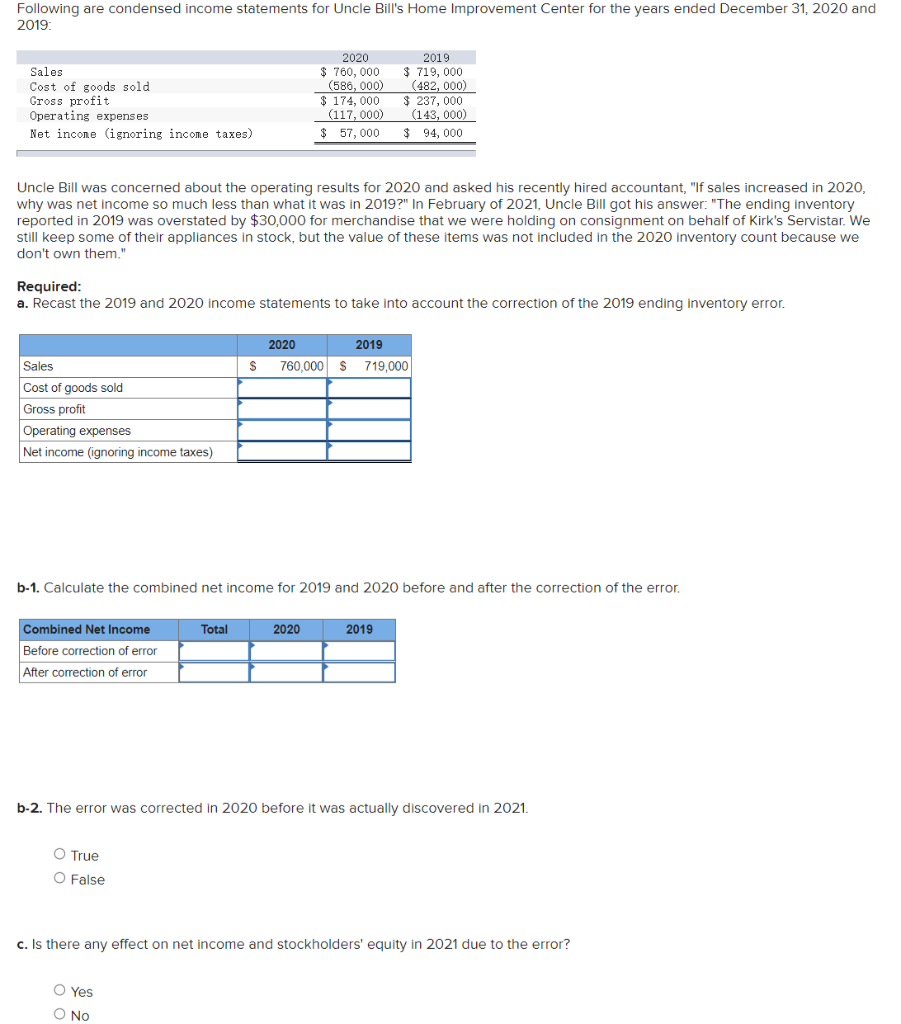

Following are condensed income statements for Uncle Bill's Home Improvement Center for the years ended December 31,2020 and 2019: Uncle Bill was concerned about the

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial accounting

Authors: Walter T. Harrison Jr., Charles T. Horngren, C. William Thom

9th edition

978-0132751216, 132751127, 132751216, 978-0132751124