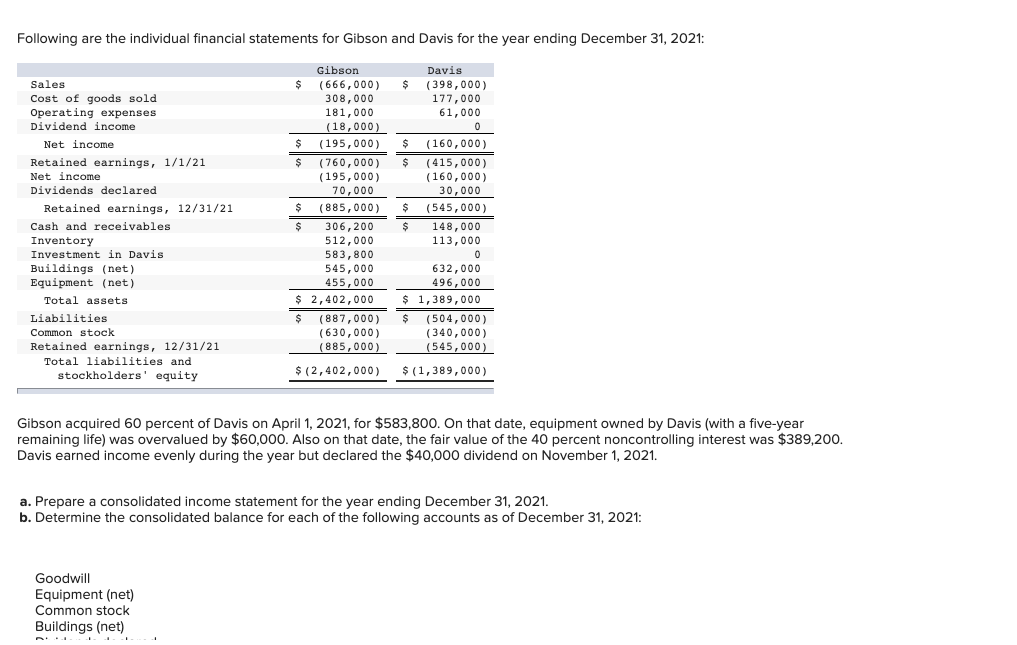

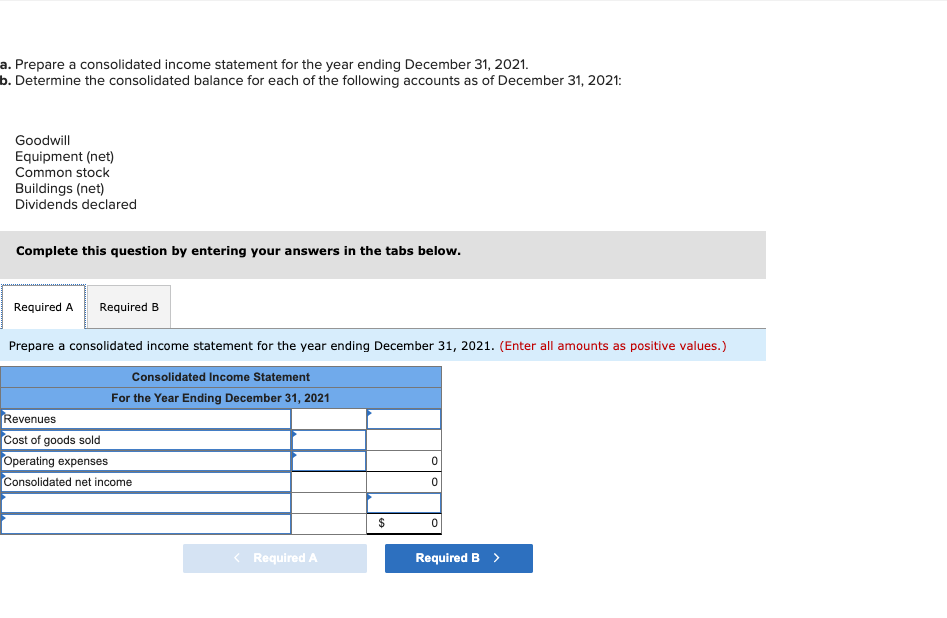

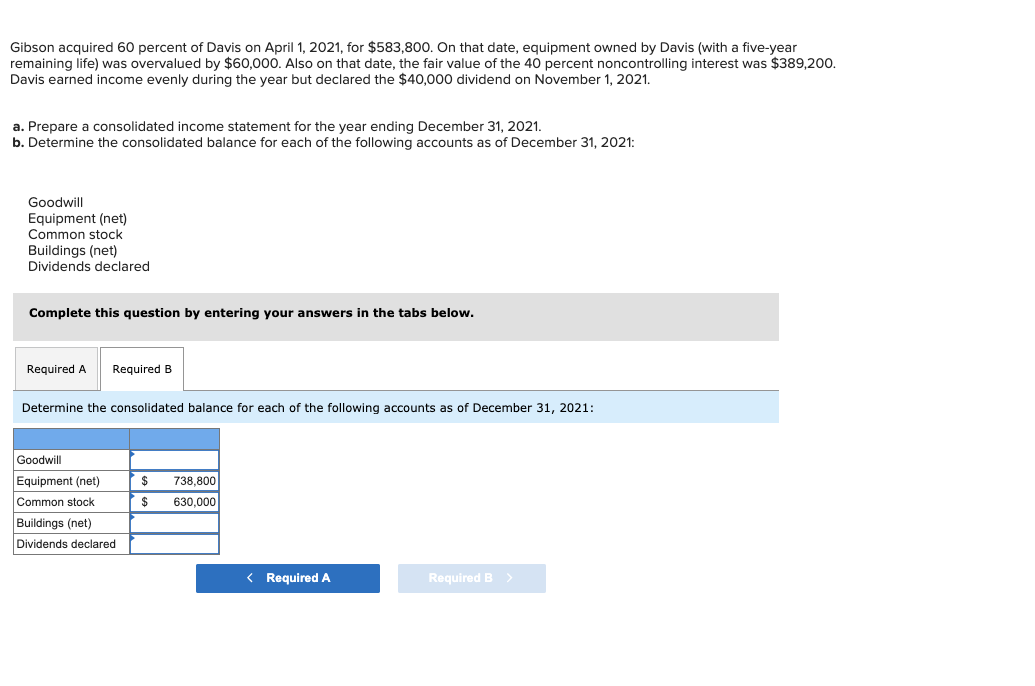

Following are the individual financial statements for Gibson and Davis for the year ending December 31, 2021: Sales Cost of goods sold Operating expenses Dividend income Net income Retained earnings, 1/1/21 Net income Dividends declared Retained earnings, 12/31/21 Cash and receivables Inventory Investment in Davis Buildings (net) Equipment (net) Total assets Liabilities Common stock Retained earnings, 12/31/21 Total liabilities and stockholders' equity Gibson $ (666,000) 308,000 181,000 (18,000) $ (195,000) $ (760,000) (195,000) 70,000 $ (885,000) $ 306,200 512,000 583,800 545,000 455,000 $ 2,402,000 $ (887,000) (630,000) (885,000) Davis $ (398,000) 177,000 61,000 0 $ (160,000) $ (415,000) (160,000) 30,000 $ (545,000) $ 148,000 113,000 0 632,000 496,000 $ 1,389,000 $ (504,000) (340,000) (545,000) $ (2,402,000) $(1,389,000) Gibson acquired 60 percent of Davis on April 1, 2021, for $583,800. On that date, equipment owned by Davis (with a five-year remaining life) was overvalued by $60,000. Also on that date, the fair value of the 40 percent noncontrolling interest was $389,200. Davis earned income evenly during the year but declared the $40,000 dividend on November 1, 2021. a. Prepare a consolidated income statement for the year ending December 31, 2021. b. Determine the consolidated balance for each of the following accounts as of December 31, 2021: Goodwill Equipment (net) Common stock Buildings (net) a. Prepare a consolidated income statement for the year ending December 31, 2021. b. Determine the consolidated balance for each of the following accounts as of December 31, 2021: Goodwill Equipment (net) Common stock Buildings (net) Dividends declared Complete this question by entering your answers in the tabs below. Required A Required B Prepare a consolidated income statement for the year ending December 31, 2021. (Enter all amounts as positive values.) Consolidated Income Statement For the Year Ending December 31, 2021 Revenues Cost of goods sold Operating expenses Consolidated net income 0 0 $ 0 Gibson acquired 60 percent of Davis on April 1, 2021, for $583,800. On that date, equipment owned by Davis (with a five-year remaining life) was overvalued by $60,000. Also on that date, the fair value of the 40 percent noncontrolling interest was $389,200. Davis earned income evenly during the year but declared the $40,000 dividend on November 1, 2021. a. Prepare a consolidated income statement for the year ending December 31, 2021. b. Determine the consolidated balance for each of the following accounts as of December 31, 2021: Goodwill Equipment (net) Common stock Buildings (net) Dividends declared Complete this question by entering your answers in the tabs below. Required A Required B Determine the consolidated balance for each of the following accounts as of December 31, 2021: $ Goodwill Equipment (net) Common stock Buildings (net) Dividends declared 738,800 630,000 $