Answered step by step

Verified Expert Solution

Question

1 Approved Answer

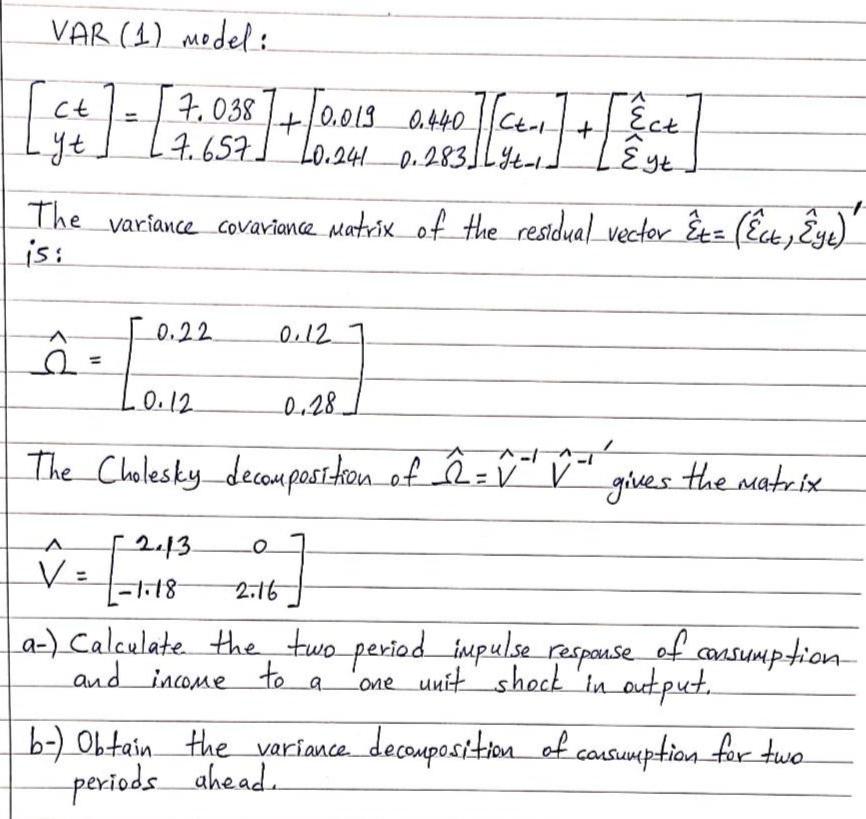

Following VAR model is estimated for consumption (c) and income (y). VAR (1) model: ct [ C+ ] = [ 7.058 ] + [0.015_0440 ]

Following VAR model is estimated for consumption (c) and income (y).

VAR (1) model: ct [ C+ ] = [ 7.058 ] + [0.015_0440 ] [C+1] + [ & ct] Ect. yt 7.657] 0.283] The variance covariance Matrix of the residual vector t= (ct, Eyt) is: a = 50.22. V = 0.12. 0.28- The Cholesky decomposition of _^2= V V gives the matrix 0.12 2.13. L-1.18- 2.16 a-) Calculate the two period impulse response of consumption one unit shock in output. and income to a decomposition of consumption for two b-) Obtain the variance periods ahead.

Step by Step Solution

★★★★★

3.47 Rating (163 Votes )

There are 3 Steps involved in it

Step: 1

a To calculate the twoperiod impulse response of consumption and income to a oneunit shock in ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Business Statistics In Practice

Authors: Bruce Bowerman, Richard O'Connell

6th Edition

0073401838, 978-0073401836