Answered step by step

Verified Expert Solution

Question

1 Approved Answer

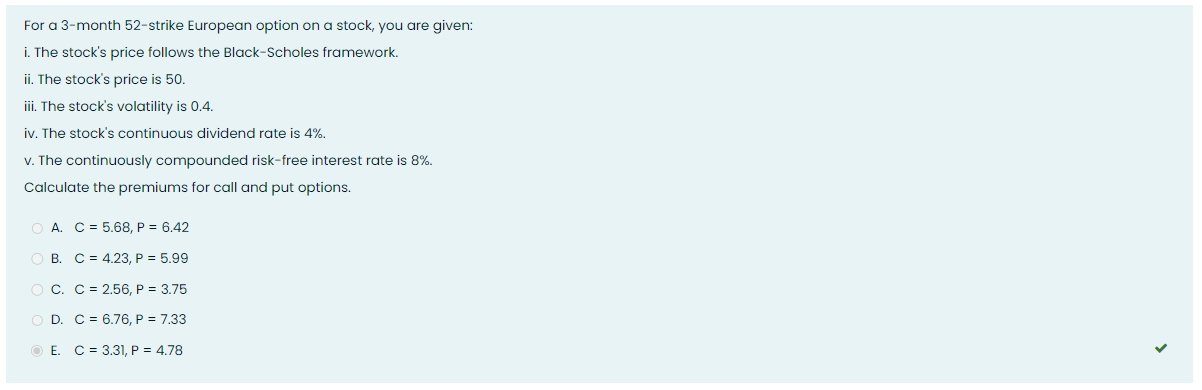

For a 3-month 52-strike European option on a stock, you are given: i. The stock's price follows the Black-Scholes framework. ii. The stock's price is

For a 3-month 52-strike European option on a stock, you are given: i. The stock's price follows the Black-Scholes framework. ii. The stock's price is 50 . iii. The stock's volatility is 0.4 . iv. The stock's continuous dividend rate is 4%. v. The continuously compounded risk-free interest rate is 8%. Calculate the premiums for call and put options. A. C=5.68,P=6.42 B. C=4.23,P=5.99 C. C=2.56,P=3.75 D. C=6.76,P=7.33 E. C=3.31,P=4.78

For a 3-month 52-strike European option on a stock, you are given: i. The stock's price follows the Black-Scholes framework. ii. The stock's price is 50 . iii. The stock's volatility is 0.4 . iv. The stock's continuous dividend rate is 4%. v. The continuously compounded risk-free interest rate is 8%. Calculate the premiums for call and put options. A. C=5.68,P=6.42 B. C=4.23,P=5.99 C. C=2.56,P=3.75 D. C=6.76,P=7.33 E. C=3.31,P=4.78 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Complete Guide To Option Selling How Selling Options Can Lead To Stellar Returns In Bull And Bear Markets

Authors: James Cordier , Michael Gross

2nd Edition

0071733485