Answered step by step

Verified Expert Solution

Question

1 Approved Answer

For Part A- Please explain how to get the Call, Put, and Net. For Part B- Please explain how to get break-even points of the

For Part A- Please explain how to get the Call, Put, and Net.

For Part B- Please explain how to get break-even points of the long straddle.

Much appreciated!

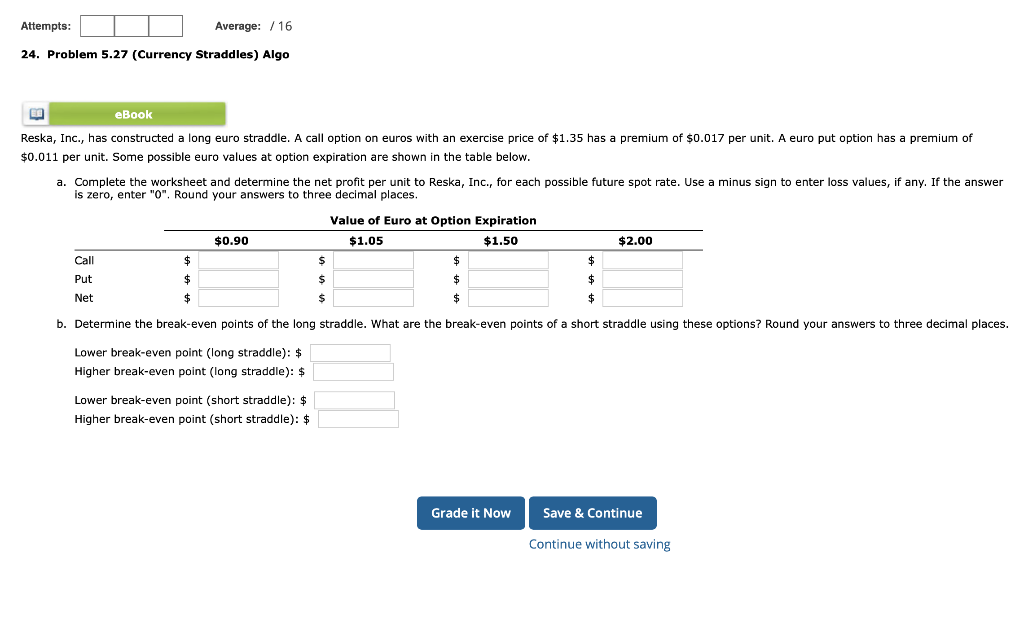

Attempts: Average: /16 24. Problem 5.27 (Currency Straddles) Algo eBook Reska, Inc., has constructed a long euro straddle. A call option on euros with an exercise price of $1.35 has premium of $0.017 per unit. A euro put option has a premium of $0.011 per unit. Some possible euro values at option expiration are shown in the table below. a. Complete the worksheet and determine the net profit per unit to Reska, Inc., for each possible future spot rate. Use a minus sign to enter loss values, if any. If the answer is zero, enter "0". Round your answers to three decimal places. Value of Euro at Option Expiration $0.90 $1.05 $1.50 $2.00 Call $ $ $ $ Put $ $ $ $ Net $ $ $ $ b. Determine the break-even points of the long straddle. What are the break-even points of a short straddle using these options? Round your answers to three decimal places. Lower break-even point (long straddle): $ Higher break-even point (long straddle): $ Lower break-even point (short straddle): $ Higher break-even point (short straddle): $ Grade it Now Save & Continue Continue without saving

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles Of Macroeconomics

Authors: Frank, Bernanke, Antonovics, Heffetz

3rd Edition

1259117162, 9781259117169