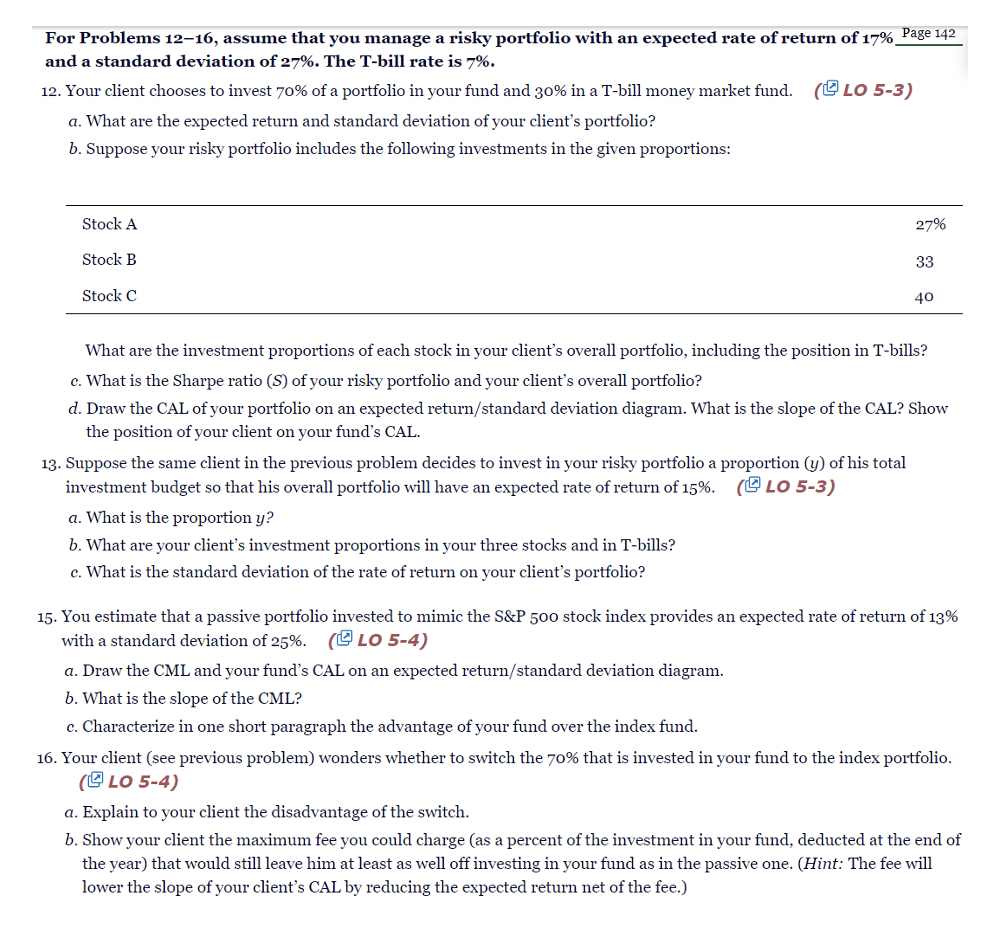

For Problems 1216, assume that you manage a risky portfolio with an expected rate of return of 17% Page 142 and a standard deviation of 27%. The T-bill rate is 7%. 12. Your client chooses to invest 70% of a portfolio in your fund and 30% in a T-bill money market fund. ( LO 53 ) a. What are the expected return and standard deviation of your client's portfolio? b. Suppose your risky portfolio includes the following investments in the given proportions: What are the investment proportions of each stock in your client's overall portfolio, including the position in T-bills? c. What is the Sharpe ratio (S) of your risky portfolio and your client's overall portfolio? d. Draw the CAL of your portfolio on an expected return/standard deviation diagram. What is the slope of the CAL? Show the position of your client on your fund's CAL. 13. Suppose the same client in the previous problem decides to invest in your risky portfolio a proportion (y) of his total investment budget so that his overall portfolio will have an expected rate of return of 15%. () O53) a. What is the proportion y ? b. What are your client's investment proportions in your three stocks and in T-bills? c. What is the standard deviation of the rate of return on your client's portfolio? 15. You estimate that a passive portfolio invested to mimic the S\&P 500 stock index provides an expected rate of return of 13% with a standard deviation of 25%. ( O54) a. Draw the CML and your fund's CAL on an expected return/standard deviation diagram. b. What is the slope of the CML? c. Characterize in one short paragraph the advantage of your fund over the index fund. 16. Your client (see previous problem) wonders whether to switch the 70% that is invested in your fund to the index portfolio. ( LO 5-4) a. Explain to your client the disadvantage of the switch. b. Show your client the maximum fee you could charge (as a percent of the investment in your fund, deducted at the end of the year) that would still leave him at least as well off investing in your fund as in the passive one. (Hint: The fee will lower the slope of your client's CAL by reducing the expected return net of the fee.) For Problems 1216, assume that you manage a risky portfolio with an expected rate of return of 17% Page 142 and a standard deviation of 27%. The T-bill rate is 7%. 12. Your client chooses to invest 70% of a portfolio in your fund and 30% in a T-bill money market fund. ( LO 53 ) a. What are the expected return and standard deviation of your client's portfolio? b. Suppose your risky portfolio includes the following investments in the given proportions: What are the investment proportions of each stock in your client's overall portfolio, including the position in T-bills? c. What is the Sharpe ratio (S) of your risky portfolio and your client's overall portfolio? d. Draw the CAL of your portfolio on an expected return/standard deviation diagram. What is the slope of the CAL? Show the position of your client on your fund's CAL. 13. Suppose the same client in the previous problem decides to invest in your risky portfolio a proportion (y) of his total investment budget so that his overall portfolio will have an expected rate of return of 15%. () O53) a. What is the proportion y ? b. What are your client's investment proportions in your three stocks and in T-bills? c. What is the standard deviation of the rate of return on your client's portfolio? 15. You estimate that a passive portfolio invested to mimic the S\&P 500 stock index provides an expected rate of return of 13% with a standard deviation of 25%. ( O54) a. Draw the CML and your fund's CAL on an expected return/standard deviation diagram. b. What is the slope of the CML? c. Characterize in one short paragraph the advantage of your fund over the index fund. 16. Your client (see previous problem) wonders whether to switch the 70% that is invested in your fund to the index portfolio. ( LO 5-4) a. Explain to your client the disadvantage of the switch. b. Show your client the maximum fee you could charge (as a percent of the investment in your fund, deducted at the end of the year) that would still leave him at least as well off investing in your fund as in the passive one. (Hint: The fee will lower the slope of your client's CAL by reducing the expected return net of the fee.)